Markel Group (NYSE:MKL) Q4 2025: Robust Revenue Performance

Markel Group Surpasses Q4 2025 Revenue Expectations

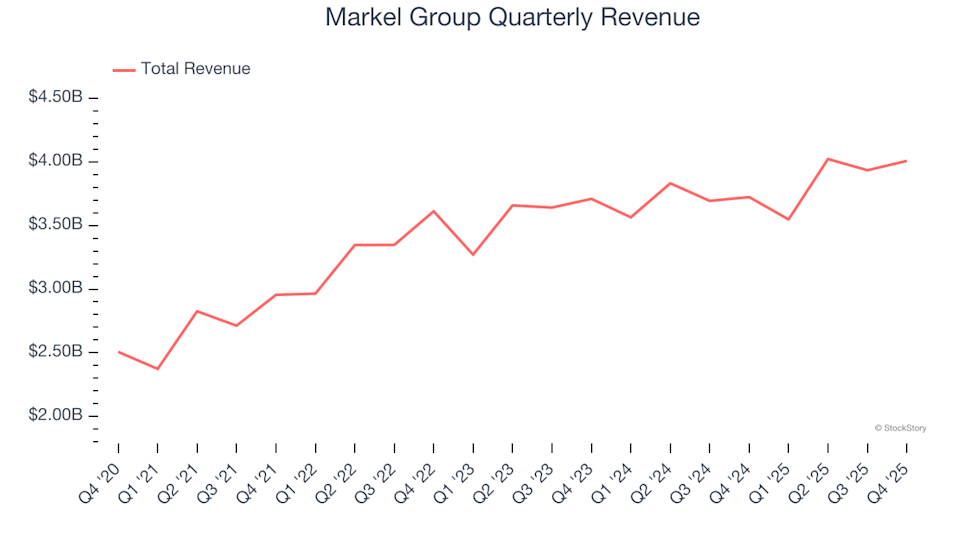

Markel Group (NYSE: MKL), a leader in specialty insurance, delivered fourth-quarter 2025 results that exceeded market forecasts. The company reported a 7.6% increase in revenue year-over-year, reaching $4.01 billion. Its GAAP earnings per share came in at $48.75, surpassing analyst projections by 21.1%.

Curious if Markel Group is a smart investment right now?

Highlights from Markel Group’s Q4 2025 Performance

- Net Premiums Earned: $2.28 billion, outpacing analyst expectations of $2.17 billion (7.6% annual growth, 5.1% above consensus)

- Total Revenue: $4.01 billion, beating projections of $3.87 billion (7.6% annual growth, 3.7% above consensus)

- Combined Ratio: 92.7%, outperforming the expected 95.3% (a 260 basis point improvement)

- GAAP EPS: $48.75, exceeding the anticipated $40.24 (21.1% above expectations)

- Market Value: $25.71 billion

“Markel Group made significant strides in 2025. Operating income reached $3.2 billion, and adjusted operating income surpassed $2.3 billion, with all business segments contributing meaningfully,” stated CEO Tom Gayner.

About Markel Group

Often likened to a “mini Berkshire Hathaway” due to its diversified business model, Markel Group operates across insurance, investments, and wholly-owned businesses. The company specializes in underwriting complex risks, managing investment portfolios, and overseeing a broad array of operating subsidiaries.

Examining Revenue Growth

Insurance companies typically generate income through three primary channels: underwriting (premiums earned), investment income from managing the float, and fees from services such as policy administration or annuities. Markel Group has achieved an impressive 11.2% compound annual revenue growth over the past five years, outpacing the industry average and reflecting strong customer demand.

While long-term growth is crucial, recent shifts in interest rates and market conditions can impact financial results. Over the past two years, Markel Group’s annualized revenue growth slowed to 4.2%, falling below its five-year trend and indicating a deceleration in demand.

Note: Certain quarters are excluded from the analysis due to exceptional investment gains or losses that do not reflect the company’s ongoing business fundamentals.

For Q4, Markel Group posted a 7.6% year-over-year increase in revenue, with its $4.01 billion result exceeding Wall Street’s forecast by 3.7%.

Revenue Mix and Net Premiums Earned

Over the last five years, net premiums earned have accounted for 57.5% of Markel Group’s total revenue, highlighting a balanced contribution from both insurance and non-insurance activities.

Among the various revenue streams, net premiums earned are viewed as the most direct indicator of an insurer’s core business, offering a more stable measure compared to the volatility of investment returns and fee income.

Understanding Net Premiums Earned

When insurance companies issue policies, they often use reinsurance to protect themselves from large or unexpected losses. Net premiums earned represent the portion of gross premiums retained after transferring some risk to reinsurers.

Markel Group’s net premiums earned have grown at a 9.2% annual rate over the past five years, slightly outpacing the broader insurance sector but trailing the company’s overall revenue growth.

Looking at the last two years, net premiums earned increased at a slower 2.5% annual rate, suggesting that other income sources, such as investment returns, have grown more rapidly. While these additional streams can boost profits, their impact may fluctuate with market conditions, and not all companies achieve consistent investment success.

In the fourth quarter, Markel Group reported $2.28 billion in net premiums earned, a 7.6% increase from the previous year and 5.1% above analyst expectations.

Summary of Q4 Results

Markel Group’s strong quarterly performance included beating EPS and net premiums earned forecasts. Despite these positive results, the company’s stock price remained steady at $2,061 following the announcement.

While the latest earnings were robust, investors should consider broader factors such as valuation and business fundamentals before making investment decisions.

Industry Trends

As software continues to transform industries worldwide, demand for developer tools is on the rise—whether for monitoring cloud infrastructure, integrating multimedia, or enabling seamless content delivery.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Newmont’s Alpha Strategy: Ensuring Long-Term Cash Generation Through the Cerro Negro Investment

Consensys-backed SharpLink reports $734 million loss as ETH holdings climb

Coeur Mining Surges 340% Over the Last Year: What Factors Are Fueling Its Share Price?

Coeur Mining Shares Surge 340% Over the Last Year: What Factors Are Fueling This Growth?