Peloton (NASDAQ:PTON) Announces Q4 CY2025 Earnings With Revenue Falling Short of Analyst Expectations, Shares Decline

Peloton Q4 CY2025 Earnings Overview

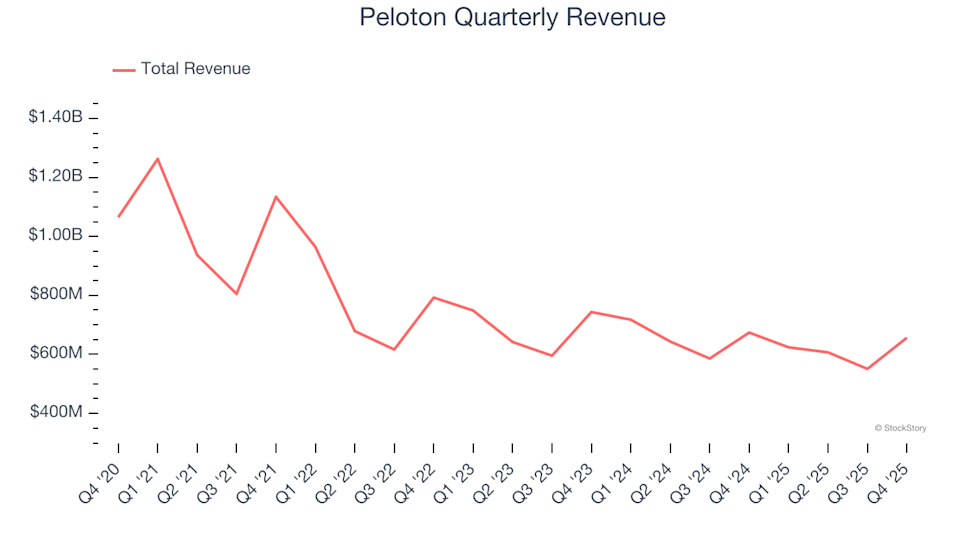

Peloton (NASDAQ:PTON), a leading provider of fitness equipment, reported fourth-quarter revenue of $656.5 million, representing a 2.6% decrease compared to the same period last year and falling short of market expectations. The company’s revenue outlook for the upcoming quarter is $615 million, which is 3.5% below what analysts had anticipated. Additionally, Peloton posted a GAAP loss of $0.09 per share, missing consensus estimates by 53.8%.

Is Peloton a good investment at this point?

Highlights from Peloton’s Q4 CY2025 Results

- Revenue: $656.5 million, missing analyst expectations of $677.2 million (2.6% year-over-year decline, 3.1% below estimates)

- GAAP EPS: -$0.09, compared to the expected -$0.06 (53.8% below consensus)

- Adjusted EBITDA: $81.4 million, exceeding analyst forecasts of $72.61 million (12.4% margin, 12.1% above estimates)

- Full-Year Revenue Guidance: Reduced to $2.42 billion (midpoint), down from $2.45 billion, a 1.2% decrease

- Full-Year EBITDA Guidance: $475 million (midpoint), surpassing analyst projections of $462 million

- Operating Margin: -2.2%, an improvement from -6.8% a year ago

- Free Cash Flow Margin: 10.8%, compared to 15.7% in the previous year’s quarter

- Connected Fitness Subscribers: 2.88 million, unchanged from the prior year

- Market Cap: $2.47 billion

CEO Peter Stern commented, “This quarter marked Peloton’s most innovative period since inception. Our disciplined approach led to a 39% increase in Adjusted EBITDA year-over-year and a 52% reduction in Net Debt, demonstrating our ability to innovate while improving profitability.”

About Peloton

Peloton (NASDAQ:PTON) began as a Kickstarter project and has grown into a prominent fitness technology company, recognized for its home exercise machines and interactive online workout experiences.

Revenue Performance

Long-term revenue trends are a key indicator of a company’s strength. While short-term gains are possible for any business, sustained growth over several years is a hallmark of quality. Over the past five years, Peloton’s sales have declined at an average annual rate of 3.8%, signaling ongoing challenges in maintaining demand and suggesting the business faces significant headwinds.

Although we prioritize long-term growth, it’s important to note that in the consumer discretionary sector, companies can sometimes benefit from new trends or products. However, Peloton’s recent results show continued weakness, with revenue falling at a 5.5% annual rate over the last two years.

Examining the number of connected fitness subscribers provides additional insight. Peloton reported 2.88 million connected fitness subscribers in the latest quarter, with the subscriber base shrinking by an average of 3.1% per year over the past two years. Since this decline is less severe than the drop in revenue, it indicates that the company’s ability to generate revenue per subscriber has weakened.

Profitability and Margins

Operating margin is a crucial metric for assessing profitability, as it reflects earnings before taxes and interest. Over the past year, Peloton’s operating margin has improved but still averaged -4.3% over the last two years, largely due to high expenses and an inefficient cost structure.

For the most recent quarter, Peloton’s operating margin stood at -2.2%. The company’s ongoing inability to achieve profitability remains a concern.

Earnings Per Share (EPS) Trends

While revenue growth is important, changes in earnings per share (EPS) reveal how profitable that growth is. Peloton’s EPS has declined at an average rate of 18.2% per year over the last five years, outpacing its revenue decline. This suggests that fixed costs have made it difficult for the company to adapt to falling demand.

In the fourth quarter, Peloton reported an EPS of -$0.09, an improvement from -$0.24 a year earlier, but still below analyst expectations. Looking ahead, analysts are optimistic, projecting that Peloton’s full-year EPS will shift from -$0.14 to a positive $0.28 over the next 12 months.

Summary and Investment Considerations

Peloton’s upbeat EBITDA guidance for the next quarter exceeded analyst expectations, and its EBITDA performance was stronger than anticipated. However, the company’s EPS missed forecasts, and its full-year revenue guidance was also disappointing. Following the earnings release, Peloton’s stock price dropped 5.3% to $5.60.

Despite a challenging quarter, investors may wonder if this presents a buying opportunity. We believe that a single quarter’s results are just one aspect of evaluating a company’s long-term quality. Assessing both business fundamentals and valuation is essential before making investment decisions.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

American Express Shares Drop Amid Mixed Earnings and 94th-Ranked Trading Volume

BlackRock Shares Climb Despite Sharp Volume Drop to 82nd in Market Activity Amid Private Credit Liquidity Crisis

Lockheed Martin's $150M Alabama Expansion Stumbles as Stock Dips 1.95% and Volume Slides to 91st

Bitway (BTW) fluctuates 70.6% in 24 hours: Driven by WEEX airdrop and Binance wallet integration