Ryder (NYSE:R) Falls Short of Q4 CY2025 Revenue Projections

Ryder’s Q4 2025 Earnings: A Closer Look

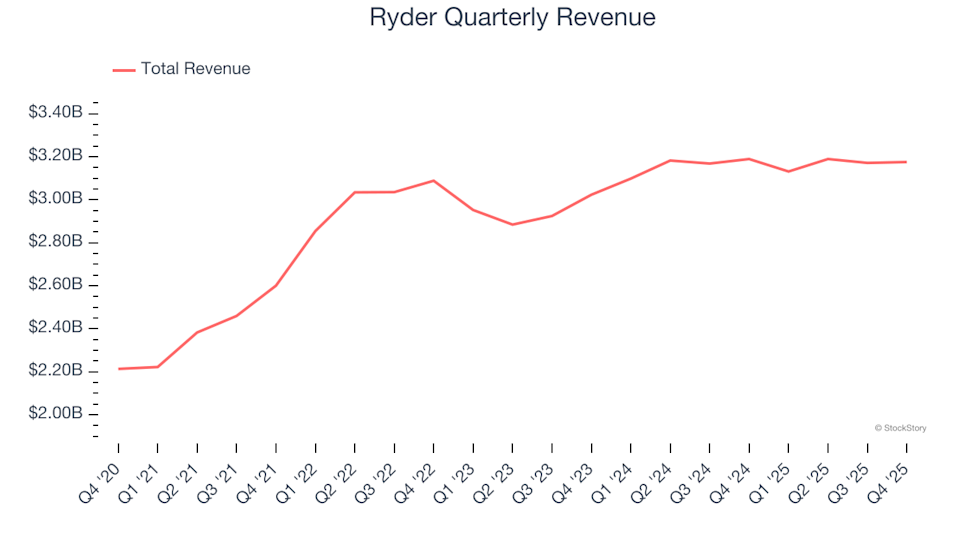

Ryder (NYSE:R), a leading provider of commercial rental vehicles and delivery services, reported fourth-quarter 2025 results that fell short of Wall Street’s revenue forecasts. The company posted $3.18 billion in sales, matching last year’s figure, and delivered non-GAAP earnings of $3.59 per share—right in line with analyst expectations.

Q4 2025 Financial Highlights

- Total Revenue: $3.18 billion, slightly below the $3.20 billion consensus (a 0.7% miss and flat year-over-year)

- Adjusted Earnings Per Share (EPS): $3.59, closely matching the $3.57 analyst estimate

- Adjusted EBITDA: $726 million, compared to the $731 million forecast (22.9% margin, 0.7% below expectations)

- 2026 Adjusted EPS Guidance: Midpoint at $13.95, which is 4.6% under analyst projections

- Operating Margin: 8.8%, consistent with the same period last year

- Free Cash Flow: $450 million, a significant improvement from negative $203 million a year ago

- Market Cap: $8.57 billion

About Ryder

Ryder pioneered the concept of truck leasing and today offers a range of rental vehicles for businesses, as well as direct delivery services to homes and companies.

Revenue Performance

Long-term sales growth is a key indicator of a company’s strength. Ryder has achieved an 8.5% compound annual growth rate in revenue over the past five years, outpacing the average for industrial companies and demonstrating strong customer demand for its services.

While five-year growth is impressive, recent trends show a slowdown. Ryder’s annualized revenue growth over the last two years was 3.7%, trailing its longer-term average and suggesting demand has softened.

Breaking down the business, Fleet Management Solutions and Supply Chain Solutions account for 46.2% and 43.5% of revenue, respectively. Over the past two years, Fleet Management Solutions (leasing and rentals) remained steady, while Supply Chain Solutions (distribution design and management) grew at an average of 5.9% year-over-year.

This quarter, Ryder’s revenue dipped 0.4% year-over-year to $3.18 billion, missing analyst expectations.

Looking forward, analysts anticipate Ryder’s revenue will increase by 3.1% over the next year, mirroring its recent growth rate. This outlook suggests that new offerings are not expected to drive significant top-line acceleration in the near term.

Profitability and Margins

Over the past five years, Ryder has maintained an average operating margin of 8.2%, outperforming the broader industrial sector. The company’s margin has improved by 1.8 percentage points during this period, benefiting from operating leverage as sales expanded—a notable achievement given that many competitors in ground transportation have seen margins decline.

In the latest quarter, Ryder’s operating margin held steady at 8.8%, matching the prior year and indicating a stable cost structure.

Earnings Per Share Trends

While revenue growth tells part of the story, changes in earnings per share (EPS) reveal how profitable that growth is. Ryder has turned its annual EPS from negative to positive over the last five years, marking a significant turnaround for the company.

However, over the past two years, EPS has remained flat despite revenue growth, indicating that profitability per share has not kept pace with sales expansion.

For Q4, adjusted EPS came in at $3.59, up from $3.45 a year earlier and closely aligned with analyst forecasts. Wall Street expects Ryder’s EPS to reach $12.94 over the next year, representing a projected 12.9% increase.

Summary and Outlook

This quarter’s results offered few bright spots. Both full-year and next-quarter EPS guidance fell short of expectations, and the stock price dropped 3.6% to $204.50 following the announcement. While Ryder’s recent performance was underwhelming, investors may want to consider the company’s longer-term fundamentals and valuation before making a decision.

Discover the Next Big Opportunity

Many industry giants—such as Microsoft, Alphabet, Coca-Cola, and Monster Beverage—started as lesser-known growth stories fueled by major trends. We’ve identified a promising AI semiconductor company that’s still flying under Wall Street’s radar.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Top Blue Chip Stock to Consider Purchasing Following This Year’s Market Decline

Lula’s Narrowing Lead Mirrors Historical Reversals as Bolsonaro Rivals Surge in Key Independent Vote

Ripple’s $50B Valuation Sparks Questions Despite Expanding Crypto Empire