5 Insightful Analyst Inquiries from Motorola Solutions’ Fourth Quarter Earnings Conference

Motorola Solutions Delivers Strong Q4 Performance

Motorola Solutions impressed investors with its fourth-quarter results, achieving significant revenue growth and outperforming market forecasts. The company’s leadership credited this success to heightened demand across both its Products & SI and Software & Services divisions. In particular, orders surged for mission-critical communications, video security, and cloud-based Command Center solutions. CEO Gregory Q. Brown highlighted that the year closed with an unprecedented $15.7 billion backlog, fueled by record-setting orders in both business segments. The company’s momentum was further bolstered by the seamless integration of recent acquisitions and the debut of innovative AI-driven products like the SVX body-worn assistant.

Should You Consider Investing in MSI?

Curious if now is a good time to invest in Motorola Solutions?

Key Q4 2025 Highlights for Motorola Solutions (MSI)

- Revenue: $3.38 billion, surpassing analyst projections of $3.34 billion (12.3% year-over-year increase, 1.1% above expectations)

- Adjusted EPS: $4.59, exceeding the consensus estimate of $4.35 (5.4% higher)

- Adjusted EBITDA: $1.16 billion, topping the $1.13 billion estimate (34.3% margin, 2.6% beat)

- Operating Margin: 27.9%, consistent with the prior year’s quarter

- Market Cap: $75.83 billion

While executive commentary is always insightful, the real value often comes from analyst Q&A sessions, which can reveal issues management might otherwise avoid or complex topics that require deeper explanation. Here are some of the most notable questions from the latest earnings call:

Top 5 Analyst Questions from the Q4 Earnings Call

- Timothy Patrick Long (Barclays): Asked about Silvus’ growth prospects amid rising demand for unmanned systems. CEO Brown noted that international markets, especially Ukraine and NATO countries, are driving up expectations for Silvus, leading to increased revenue guidance.

- Andrew Carl Spinola (UBS): Inquired about margin trends given higher tariffs and memory costs. CFO Jason J. Winkler responded that margins are expected to improve through a better product mix, greater software adoption, and disciplined cost control, targeting a 100 basis point increase.

- Adam Tindle (Raymond James): Questioned whether backlog and order momentum can be sustained as supply chain disruptions ease. Brown explained that the company is shifting to a faster “quick-turn” model and anticipates ongoing double-digit product order growth throughout the year.

- Meta A. Marshall (Morgan Stanley): Asked about the effect of rising memory prices and which business areas are strongest. Management clarified that memory costs are a minor factor and that growth is widespread across LMR, cloud video, and Command Center software.

- Keith Michael Housum (Northcoast Research): Explored the early performance and competitive edge of the AI Assist Suites. CTO Mahesh Saptharishi highlighted broad adoption in 911 workflows and stressed the integration and cost benefits compared to rival products.

What to Watch in the Coming Quarters

Looking forward, key areas to monitor include: (1) the uptake and monetization of new AI Assist Suites and the SVX device, (2) continued progress in international and defense markets, especially with the integration of Silvus, and (3) the company’s ability to maintain strong margins despite tariffs and rising component costs. Expanding recurring revenue and successfully rolling out cloud-based solutions will also be important indicators of future growth.

Motorola Solutions shares are currently trading at $457.82, up from $421.13 before the earnings announcement. Wondering if there’s an investment opportunity?

Top Picks for Quality-Focused Investors

The market has seen substantial gains this year, but much of that growth is concentrated in just a handful of stocks. With so many investors crowding into the same names, savvy investors are seeking out high-quality opportunities that others may overlook—often at more attractive prices.

This list features well-known leaders like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known companies such as Comfort Systems, which achieved a 782% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Tokenized RWAs: $2.5B Flow in a Slump

Bitcoin Price News: DeepSnitch AI Could Mirror BTC’s Early Run as Investors Place $2M Bet Ahead of March 31 Launch

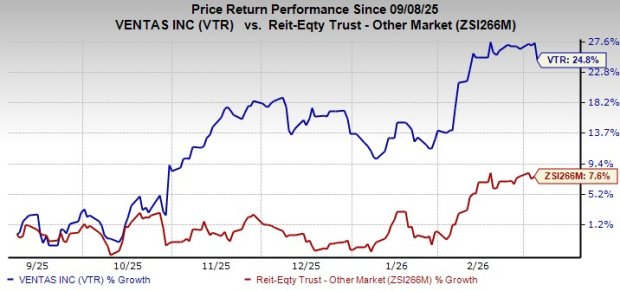

Ventas Stock Rallies 24.8% in Six Months: Will the Momentum Last?

Reasons Why You Should Retain Rollins Stock in Your Portfolio Now