AVO Stock Trades Near 52-Week High: Buy the Strength or Wait?

Mission Produce, Inc. AVO has shown a consistent upward trend in recent months. By balancing growth in emerging markets with stable demand from more mature regions, the company has positioned itself to capture new opportunities without sacrificing consistency. This broad-based exposure not only strengthens top-line visibility but also enhances resilience in an industry often shaped by volatility and regional supply shifts.

AVO, a leading avocado grower and distributor, hit a 52-week high of $15.02 on Thursday. It is currently trading just 3.4% below that peak and sits 51.9% above its 52-week low of $9.56.

Is AVO’s Overall Share Performance Just as Impressive?

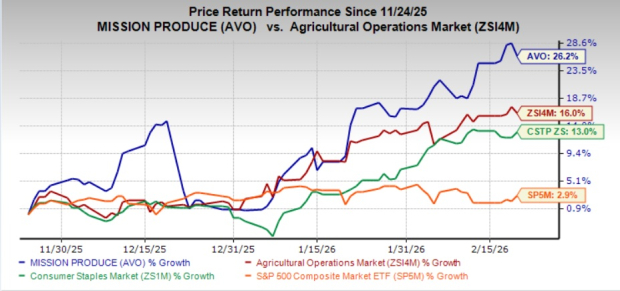

In the past three months, the company’s shares have rallied 26.2%, outperforming the broader Agricultural - Operations industry’s 16% gain, the Consumer Staples sector’s 13% rise and the S&P 500’s modest growth of 2.9%.

AVO’s Three-Month Stock Price Performance

Image Source: Zacks Investment Research

AVO’s performance is also notably stronger than that of its competitors, Corteva Inc. CTVA, Adecoagro AGRO and Dole Plc DOLE, which posted growth of 16.2%, 17.2% and 14.2%, respectively, in the past three months.

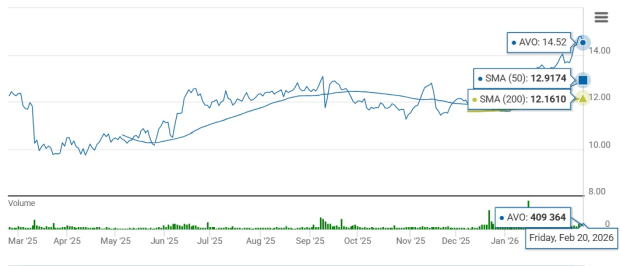

The stock trades above its 50-day and 200-day simple moving averages (SMA), indicating a bullish sentiment. SMA is an essential tool in technical analysis that helps investors evaluate price trends by smoothing out short-term fluctuations. This approach provides a clearer perspective on a stock's long-term direction.

AVO Stock Trades Above 50 & 200-Day Moving Averages

Image Source: Zacks Investment Research

What’s Fueling AVO’s Recent Outperformance?

Mission Produce’s recent stock momentum reflects growing investor confidence in the company’s vertically integrated business model, which provides greater control over sourcing, quality and distribution across global markets. This integrated platform allows AVO to respond quickly to shifts in supply and demand, optimize fruit placement across regions and maintain consistent service levels for key customers. Such operational flexibility has strengthened customer relationships and positioned Mission Produce as a reliable partner amid ongoing volatility in agricultural markets.

The company’s expanding global footprint is another key tailwind. Mission Produce has been gaining traction beyond its core North American market, supported by strong execution in Europe and other international regions. Improved access to diversified growing regions, particularly in South America, has enhanced supply consistency and reduced dependence on any single geography. This broader reach not only supports volume growth but also enables the company to capture opportunities in higher-growth international markets.

Mission Produce is seeing solid growth across its avocado, mango and blueberry businesses, supported by expanding production, stronger consumer demand and improved market penetration. Avocados remain the core growth engine, benefiting from rising household consumption and increased international reach, particularly in Europe and Asia, where consistent supply has enabled deeper retail partnerships.

The mango business continues to gain traction as the company focuses on expanding sourcing capabilities, improving availability and driving consumer awareness, which has helped build market share and strengthen its position in the category. Meanwhile, the blueberry segment is scaling steadily as newer acreage comes into production, supporting higher volumes and reinforcing Mission Produce’s presence in the fast-growing healthy snacking space, positioning the company well for sustained long-term growth across all three categories.

Mission Produce’s Estimate Revision Trend

The Zacks Consensus Estimate for AVO’s fiscal 2026 and 2027 earnings remained unchanged in the last 30 days. For fiscal 2026, the Zacks Consensus Estimate for AVO’s sales and EPS implies year-over-year declines of 10.2% and 10.1%, respectively. For fiscal 2027, the Zacks Consensus Estimate for AVO’s sales and EPS implies year-over-year growth of 1.7% and 4.2%, respectively.

Image Source: Zacks Investment Research

Decoding Challenges Faced by AVO

AVO operates in an inherently volatile pricing environment, where fluctuations in avocado supply and market pricing can pressure near-term financial performance. Periods of elevated industry supply, particularly from key sourcing regions, tend to compress selling prices and can obscure underlying volume growth. While the company manages its business around volume and per-unit margins, sharp pricing swings still create variability in reported revenue and margin percentages, making quarterly performance less predictable and increasing sensitivity to market conditions beyond management’s control.

The company also faces operational challenges linked to agricultural productivity and cost pressures across its farming operations. Newer acreage, particularly in blueberries, tends to carry higher unit costs in the early stages, while weather variability can affect yields and profitability. At the same time, ongoing investments to support global expansion added pressure on execution, and any inability to translate volume growth into sustainable margin improvement could weigh on profitability and investor sentiment.

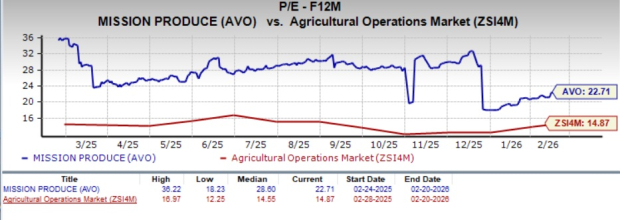

AVO’s Premium Valuation

Mission Produce is currently trading at a forward 12-month P/E multiple of 22.71X, above the industry average of 14.87X. This elevated valuation underscores the market’s confidence in the company’s long-term growth story, differentiated operating model and ability to navigate the inherent volatility of the produce sector. Investors appear willing to pay a premium for Mission Produce’s scale, vertical integration and expanding global footprint, which collectively set it apart from traditional agricultural peers.

At its current valuation, Mission Produce trades at a notable premium to several close competitors, including Adecoagro, Corteva and Dole, all of which are delivering steady growth but command meaningfully lower earnings multiples. Adecoagro, Corteva and Dole have forward 12-month P/E ratios of 7.6X, 20.09X and 10.96X — all significantly lower than that of AVO.

Image Source: Zacks Investment Research

Is it Prudent to Buy AVO Stock Now?

Mission Produce’s recent share price strength reflects improving investor confidence in its vertically integrated business model and expanding global footprint, which have enhanced operational flexibility and market reach. The company’s ability to manage supply, optimize distribution and grow volumes across avocados, mangoes and blueberries underscores its long-term growth potential.

However, Mission Produce continues to face challenges from volatile commodity pricing, agricultural productivity pressures and higher costs in newer operations. Coupled with a premium valuation compared with peers, these factors suggest that near-term performance may remain uneven. For those already invested, holding onto the stock could be a prudent choice, considering its strong long-term potential.

Mission Produce currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Innodata Inc. (INOD) Expands Role as AI Data Engineering Partner

Critical Bitcoin weekly trend breaks for first time in 2+ years: Is BTC done?

PayPal Stock Up Monday Despite CEO Shake-Up, Takeover Interest, Lowered Outlook

Here's the Reason Arcellx Stock Has Surged Nearly 80% Today