Is it Justified to Bet on Undervalued SLB Stock Right Away?

SLB SLB is currently considered cheap on a relative basis, with the stock trading at a trailing 12-month enterprise value to earnings before interest, taxes, depreciation and amortization (EV/EBITDA) of 10.28X, representing a discount compared with the broader industry average of 10.48X and to Baker Hughes BKR, another oilfield service major, which trades at 14.23X. Halliburton Company HAL, belonging to the same space, is, however, valued at a lower 8.25X.

Is it time to bet on undervalued SLB right away? Before delving into it, investors should analyze the company’s overall business fundamentals first.

SLB Sees Robust Offshore Oil & Gas Activities

SLB is expecting robust opportunities in offshore oil and gas projects, particularly in its subsea business, which provides equipment installed on the ocean floor to help extract energy. The company won about $4 billion in new subsea contracts last year and anticipates total awards to be more than $9 billion over the next two years.

The oilfield services giant expressed strong confidence that industry activity is picking up. During its fourth-quarter 2025 earnings call, SLB mentioned anticipating more than 500 subsea trees, key equipment used in offshore oil and gas production, to be ordered in 2026 and 2027. That suggests a 20% improvement from the 2025 reported level, signaling growing demand and a strengthening offshore market. As a leading oilfield services provider, SLB expects to capitalize on this trend.

SLB’s Diversification Beyond Traditional Oilfield Services

To lower its dependence on commodity price volatility, SLB has been focusing on the Data Center Solutions business, which the company believes to be the fastest-growing business in the coming days. The oilfield service giant is witnessing mounting opportunities from this business.

SLB also has a strong commitment to returning capital to shareholders. In 2026, the company decided to return more than $4 billion to shareholders through the employment of both stock repurchases and dividend payments.

What to Do With the Stock?

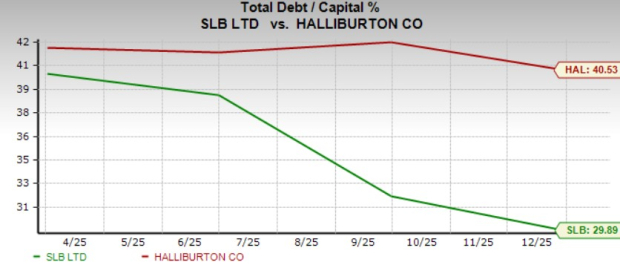

SLB has significantly lower exposure to debt capital than HAL, another industry giant. BKR, however, has lower debt exposure than SLB.

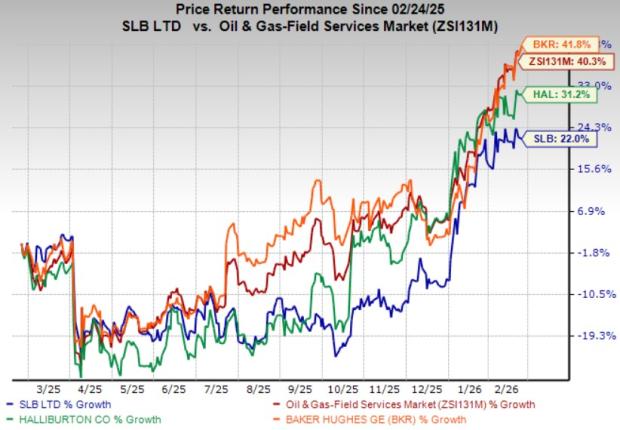

Despite the positive developments, SLB has underperformed the broader industry over the past year. Over the period, the SLB stock has gained 22%, underperforming the industry’s 40.3% jump. BKR and HAL jumped 41.8% and 31.2%, respectively, over the same time frame.

Moreover, SLB is expecting a temporary slowdown in business at the beginning of 2026. Thus, it is not ideal for investors to bet on the stock right away, although it is undervalued. However, those who have already invested may continue to retain the Zacks Rank #3 (Hold) stock in their portfolios.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Greif, Inc. Declares Quarterly Dividend

BC-Gold-Silver

Quantum Outlook for March 2026: 3 Stocks With Over 100% Price Target