3 Reasons Why BY Is a Risky Choice and One Alternative Stock Worth Considering

Byline Bancorp: Recent Performance and Investment Outlook

Byline Bancorp is currently priced at $31.86 per share, having climbed 10.9% in the past six months—outpacing the S&P 500’s 6.2% gain during the same period.

Should you consider adding Byline Bancorp to your portfolio, or is caution warranted?

Reasons for a Cautious Approach to Byline Bancorp

We remain reserved about Byline Bancorp’s prospects. Here are three factors that temper our enthusiasm, along with an alternative stock we prefer.

1. Slowing sop Revenue Expansion

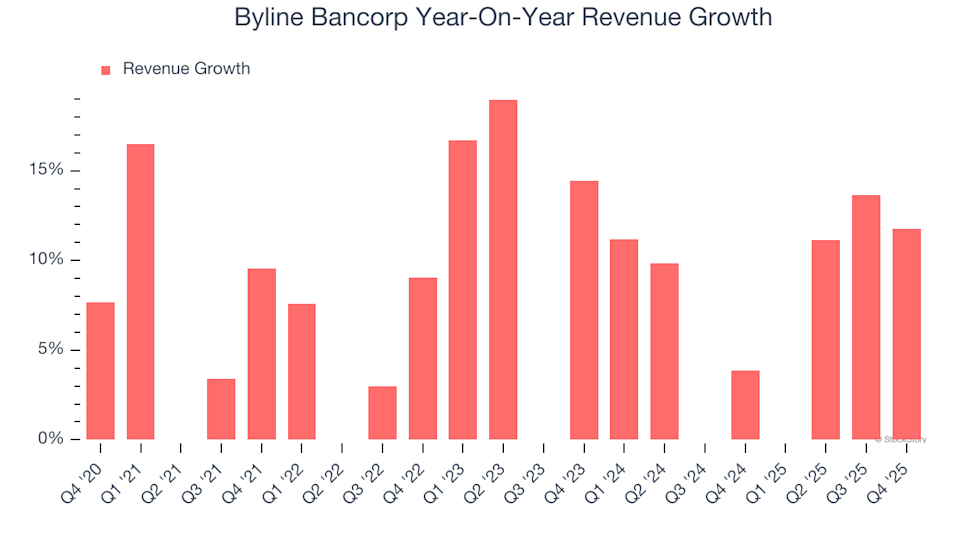

While long-term growth is crucial, focusing solely on historical performance can overlook recent shifts in interest rates and market dynamics. Byline Bancorp’s annualized revenue growth over the past two years was 7.4%, falling short of its five-year average. This slowdown in revenue may indicate shifting customer preferences, especially in a sector where switching costs are low.

Byline Bancorp Year-On-Year Revenue Growth

Note: Certain quarters are excluded as they were impacted by significant investment gains or losses, which do not reflect the company’s ongoing business fundamentals.

2. Modest Outlook for Net Interest Income

Analyst forecasts for net interest income provide insight into a company’s future potential. While projections can miss the mark, accelerating growth tends to lift valuations, whereas deceleration can weigh on stock prices.

Wall Street expects Byline Bancorp’s net interest income to increase by just 4.4% over the next year—a slowdown from the 8% annualized growth seen in the previous two years. This suggests a less robust outlook moving forward.

3. Earnings Per Share Growth Disappoints

While long-term earnings trends are important, short-term EPS changes can reveal emerging patterns. Byline Bancorp’s EPS grew at a compounded annual rate of only 2.4% over the past two years, lagging behind its revenue growth. This indicates that profitability per share has diminished as the company has expanded.

Byline Bancorp Trailing 12-Month EPS (Non-GAAP)

Our Verdict

Byline Bancorp is not a poor business, but it doesn’t meet our investment criteria. The stock trades at 1× forward price-to-book, or $31.86 per share, which is a fair valuation. However, we don’t see significant upside at this time and believe there are more attractive opportunities elsewhere. For example, consider a rapidly expanding restaurant chain known for its A+ ranch dressing.

Top Stocks for Any Market Environment

This year’s market rally has been driven by just four stocks, accounting for half of the S&P 500’s gains—a level of concentration that makes many investors uneasy. While the crowd chases the same popular names, savvy investors are seeking quality in overlooked areas, often at much lower prices. Explore our handpicked selections in the Top 5 Growth Stocks for this month. These high-quality stocks have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known companies like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Tecnoglass, which achieved a 1,754% five-year return. Discover your next winning investment with StockStory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Vanguard Global Capital Cycles Fund Investor (VGPMX) Currently a Top Choice Among Mutual Funds?

Roblox's Momentum Fades As EU Digital Services Act Probe Triggers Stock Slide

Copper: Chinese demand lifts prices – ING

Today's Bullish Patterns & Technical Sentiment | Published on 02/25: ARM, ADEA, HRL and More