3 Reasons Why TMHC Carries Risks and One Alternative Stock Worth Considering

Taylor Morrison Home: Recent Performance and Outlook

Over the past half-year, Taylor Morrison Home’s stock price has remained relatively unchanged, slipping just 1.6% to settle at $66.89. In comparison, the S&P 500 advanced by 6.2% during the same period, highlighting the company’s underperformance against the broader market.

Is it a smart move to invest in Taylor Morrison Home right now, or should you proceed with caution?

Why We’re Not Enthusiastic About Taylor Morrison Home

At this time, we’re choosing to stay on the sidelines. Here are three reasons we’re steering clear of TMHC, along with a stock we find more appealing.

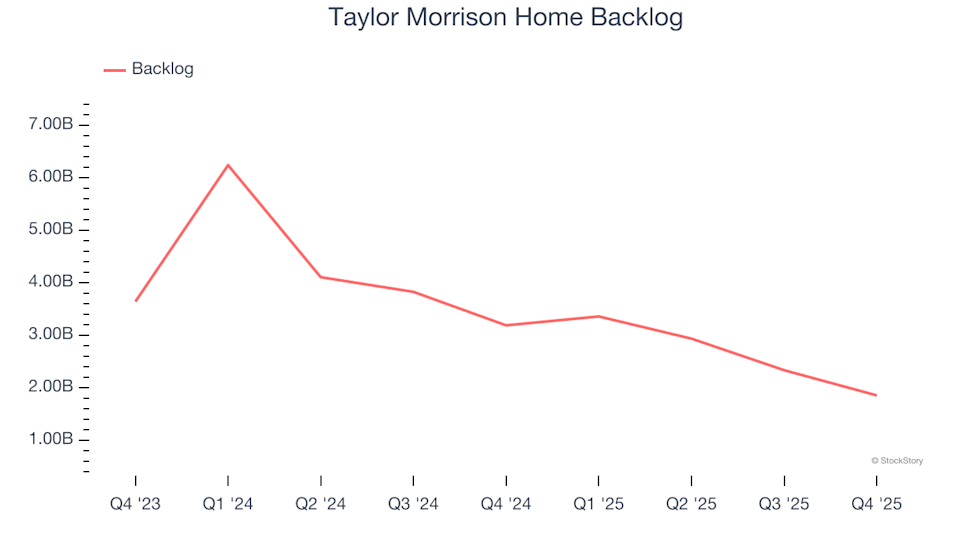

1. Shrinking Backlog Signals Fewer Orders

For homebuilders, backlog—the total value of unfulfilled orders—offers a glimpse into future revenue potential. Taylor Morrison Home’s latest reported backlog stands at $1.86 billion, but this figure has dropped by an average of 33.6% year-over-year for the past two years. Such a decline suggests the company is struggling to secure new business, possibly due to intensifying competition or a saturated market.

2. Revenue Forecasts Point to Slower Growth

Analyst projections for future revenue provide valuable clues about a company’s prospects. While forecasts aren’t always precise, accelerating sales growth tends to lift valuations, whereas decelerating growth can weigh on share prices. For Taylor Morrison Home, analysts anticipate a 17.2% revenue decline over the next year—a sharp reversal from the 5.8% annual growth rate seen over the previous five years. This outlook suggests the company may face weaker demand ahead.

3. EPS Growth Lags Behind Expectations

Although long-term earnings trends are important, we also examine recent earnings per share (EPS) growth to spot any shifts in performance. Over the past two years, Taylor Morrison Home’s EPS has grown at a modest 3.8% annually, mirroring its revenue trend. This indicates the company has maintained its profitability per share, but hasn’t delivered standout growth.

Our Verdict

While Taylor Morrison Home is not a poor business, it doesn’t make our list of top picks. The stock currently trades at 13 times forward earnings, or $66.89 per share—a reasonable valuation, but we see more compelling opportunities elsewhere. If you’re seeking growth, consider exploring our recommended software and edge computing stocks.

Better Alternatives to Taylor Morrison Home

Relying on just a handful of stocks can leave your portfolio vulnerable. Now is the time to secure high-quality investments before the market broadens and attractive prices disappear.

Discover Top Growth Stocks

Don’t wait for market turbulence to act. Explore our Top 5 Growth Stocks for this month. These carefully selected high-quality stocks have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known leaders like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Tecnoglass, which achieved a 1,754% five-year return. Find your next winning stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Decreasing Convenience Yield and the Impact of Quantitative Tightening

Pundit: $50–$100 XRP Is Inevitable By Christmas If Trump Makes This Move

Evaluating the Strategic and Financial Consequences of the US-Israel Attack on Iran

Instacart: A Conviction Buy for Quality Growth Portfolios?