3 Key Reasons to Steer Clear of AVAV and One Alternative Stock Worth Buying

AeroVironment’s Recent Performance Compared to the Market

Over the past half year, AeroVironment’s share price has largely mirrored the S&P 500’s upward movement. The company’s stock has advanced by 8.6%, reaching $261.95 per share, while the broader index has increased by 6.2% during the same period.

Should you consider adding AeroVironment to your investment portfolio now, or is caution warranted?

Why We’re Not Enthusiastic About AeroVironment

At this time, we’re choosing to stay on the sidelines. Below are three key reasons why AeroVironment doesn’t stand out to us, along with a stock we prefer instead.

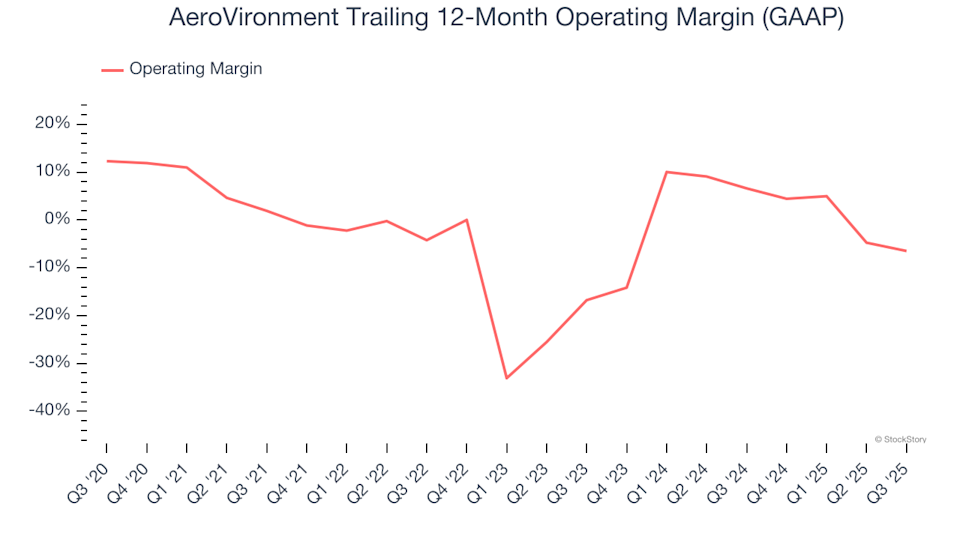

1. Declining Operating Margin

Operating margin is a crucial indicator of a company’s profitability, representing earnings before taxes and interest—factors less tied to core business operations.

Looking at AeroVironment’s financials, its operating margin has dropped by 8.4 percentage points over the past five years. This decline is concerning, especially since revenue growth should have helped the company better manage fixed costs and improve profitability. Instead, rising expenses have outpaced revenue gains, and the company hasn’t been able to pass these costs onto customers. For the last twelve months, AeroVironment’s operating margin stood at negative 6.5%.

2. Earnings Per Share Have Fallen Over Two Years

While long-term earnings trends are important, tracking short-term changes in earnings per share (EPS) can reveal new developments within a business.

Unfortunately, AeroVironment’s EPS has decreased by an average of 9.9% each year over the past two years, despite a 44.8% increase in revenue. This suggests that the company’s profitability on a per-share basis has weakened as it has grown.

3. Free Cash Flow Margin Is Worsening

Free cash flow is a valuable metric because it reflects all operating and capital expenditures, making it difficult to manipulate. In the end, cash flow is what matters most.

Over the last five years, AeroVironment’s free cash flow margin has fallen by 19 percentage points. Any negative trend here is troubling, especially since the company is already burning cash. If this pattern persists, it could indicate that AeroVironment is becoming more reliant on capital. For the trailing twelve months, its free cash flow margin was negative 17.6%.

Our Verdict

While AeroVironment isn’t a poor business, it doesn’t make our list of top picks. Currently, the stock trades at a forward price-to-earnings ratio of 57.6 (or $261.95 per share), reflecting high expectations. We believe there are other companies with stronger fundamentals at this time. Consider exploring one of our leading digital advertising stocks instead.

Alternative Stocks Worth Considering

Relying on just four stocks for your portfolio’s success can be risky. Now is the time to secure high-quality investments before the market broadens and current prices are no longer available.

Don’t wait for the next market downturn. Take a look at our Top 5 Growth Stocks for this month. This handpicked selection of high-quality stocks has delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known names like Nvidia, which soared 1,326% between June 2020 and June 2025, as well as lesser-known companies such as Exlservice, which achieved a 354% five-year return. Discover your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Agilent's Stock Climbs 0.74% as Trading Volume Crumbles 20.6% to Rank 442nd in Volume

IDEXX's Slight Earnings Miss Leads to 0.18% Decline, with $320M Trading Volume Placing 450th on March 3

BK Drops Even After Surpassing Earnings Estimates as $330M Trading Volume Places It at 441st in Market Turnover

Domino's Pizza Stock Rises 1.75% as $330M Volume Ranks 434th