Can Lam Research Maintain Its Over $5 Billion Revenue Run Thanks to Foundry Demand?

Lam Research: Sustained Revenue Growth Driven by Foundry Demand

Lam Research Corporation (LRCX) has consistently generated over $5 billion in revenue for three straight quarters, highlighting the ongoing strength in the wafer fabrication equipment sector. In the second quarter of fiscal 2026, the company reported a 22% increase in revenue, reaching $5.34 billion. This impressive growth was largely fueled by the Systems division, which benefited from heightened demand in the foundry market, particularly for artificial intelligence (AI) applications.

During this period, Systems revenue climbed 28% year-over-year to $3.36 billion. The foundry segment contributed 59% of Systems sales, a significant rise from 35% in the same quarter last year. Lam Research’s foundry operations are thriving as investments in advanced semiconductor manufacturing accelerate, especially for AI and high-performance computing. The company’s expertise in etch and deposition equipment, essential for producing smaller and more complex transistors, has solidified its role as a preferred supplier for leading foundries.

Innovative solutions like the Aether dry resist EUV patterning technology and the Akara conductor etch system are gaining momentum among top-tier chipmakers. These advancements enhance pattern accuracy and process efficiency, supporting the industry’s shift toward next-generation nodes such as gate-all-around transistors.

Lam Research’s ongoing commitment to technological innovation, combined with rising demand for AI and advanced computing chips, is expected to further strengthen its foundry business. This momentum should continue to drive both Systems and overall company revenues in the near future.

Analyst forecasts for the third quarter of fiscal 2026 reinforce expectations for continued growth in the Systems segment. The Zacks Consensus Estimate projects Systems revenue at $3.7 billion, representing a 22% year-over-year increase. Total revenue is anticipated to reach $5.74 billion, up 21.7% from the previous year.

Competition in the Foundry Equipment Sector

Lam Research faces significant competition from Applied Materials, Inc. (AMAT) and KLA Corporation (KLAC) within the semiconductor equipment industry.

Applied Materials is a direct rival in the deposition and etch equipment space, serving major chipmakers such as TSMC and Samsung. The company’s broad product lineup and strong customer relationships make it a formidable presence in the market.

KLA Corporation, on the other hand, specializes in process control and inspection tools, which are vital for ensuring quality and yield in advanced semiconductor manufacturing. While KLA does not compete directly with Lam Research in etch or deposition, its solutions are crucial for the overall chip production process.

Lam Research: Stock Performance, Valuation, and Outlook

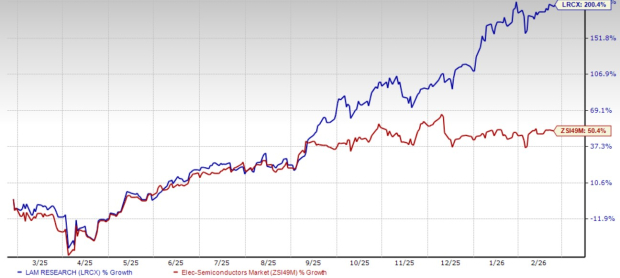

Over the past year, Lam Research shares have soared by 200.4%, far outpacing the Electronics – Semiconductors industry’s 50.4% gain.

One-Year Share Price Performance

Source: Zacks Investment Research

In terms of valuation, Lam Research is currently trading at a forward price-to-earnings (P/E) ratio of 39.75, which is notably higher than the industry average of 32.07.

Forward 12-Month P/E Ratio

Source: Zacks Investment Research

The Zacks Consensus Estimate anticipates Lam Research’s earnings to grow by approximately 27.1% in fiscal 2026 and 25.6% in fiscal 2027. Notably, estimates for fiscal 2026 have been revised upward over the past month, and projections for fiscal 2027 have increased in the past week.

Source: Zacks Investment Research

Currently, Lam Research holds a Zacks Rank #2 (Buy). For a full list of Zacks #1 Rank (Strong Buy) stocks, click here.

Zacks’ Top Semiconductor Pick

Zacks highlights a lesser-known company in the semiconductor space that is poised for significant growth, serving market needs that industry giants like NVIDIA do not address. As this company gains more attention, it stands to benefit from the expanding demand for Artificial Intelligence, Machine Learning, and the Internet of Things. The global semiconductor market is forecasted to nearly double from $452 billion in 2021 to $971 billion by 2028.

With robust earnings and a growing customer base, this company is well-positioned to capitalize on the next wave of industry expansion.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Up 37% Over the Last 6 Months, Does This Popular Networking Stock Still Have Room to Grow?

Ripple CEO Stuns XRP Army With Bombshell Statement for Banks

dogwifhat at $0.20: Reversal or further drop, what’s next for WIF?

"A sharp divide": Wall Street assesses the gains and losses as AI-fueled tech stocks tumble