Seagate or NetApp: Which Data Storage Company Makes a Wiser Investment Choice?

STX vs. NTAP: A Comprehensive Look at Data Storage Leaders

Seagate Technology Holdings plc (STX) and NetApp, Inc. (NTAP) are both integral players in the enterprise storage sector. Seagate primarily focuses on hardware solutions, especially hard disk drives, while NetApp is known for its expertise in data management and hybrid cloud storage platforms.

Market Outlook for Data Storage

According to Fortune Business Insights, the global data storage industry is expected to grow from $298.5 billion in 2026 to $984.6 billion by 2034, reflecting a compound annual growth rate (CAGR) of 16%. Mordor Intelligence projects the hard disk drive (HDD) market to increase from $51.8 billion in 2026 to $69.7 billion by 2031 at a 6% CAGR. Additionally, the enterprise flash storage market is forecasted to rise from $29.04 billion in 2025 to $49.87 billion by 2030, with an 11.42% CAGR.

Investment Considerations

Both STX and NTAP are positioned to benefit from the expansion of AI-powered data centers, as the need for scalable storage infrastructure grows with increasing data volumes. Investors looking for broad exposure to the storage landscape may consider holding both companies. However, choosing between them depends on individual preferences for value versus growth, investment timelines, and perspectives on the future of data infrastructure.

Seagate Technology (STX): Strengths and Challenges

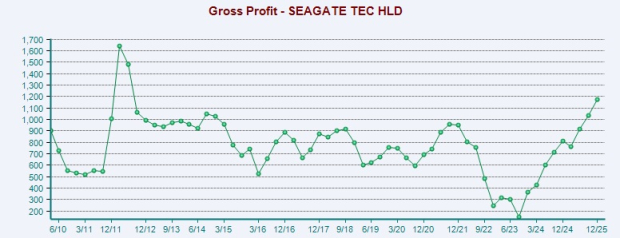

Seagate specializes in hardware storage solutions, including HDDs and large-scale capacity products for data centers and hyperscalers. The company has experienced significant growth, fueled by rising demand from AI, cloud computing, and big data applications. Seagate’s revenue can be volatile due to the cyclical nature of hardware demand, which is closely linked to enterprise spending and large-scale customer orders. In the fiscal second quarter, Seagate reported $2.83 billion in revenue, a 22% year-over-year increase, driven by robust nearline cloud demand and positive trends at the enterprise edge.

Seagate’s non-GAAP gross margin surpassed 42%, supported by strategic pricing and the growing adoption of high-capacity drives as HAMR (Heat-Assisted Magnetic Recording) shipments increased. HAMR technology is a cornerstone for scaling mass storage capacity. The company is advancing its Mozaic second-generation 4-terabyte-per-disk products and aims to reach 10 terabytes per disk in the coming years. Nearline capacity is fully booked through 2026, with strong demand visibility into 2027 and ongoing discussions for 2028.

Seagate plans to meet increasing storage needs by enhancing areal density rather than ramping up production volume. The company is seeing strong demand for video, cloud, and AI-driven applications, which are generating massive data storage requirements. By focusing on higher-capacity products and leveraging HAMR technology, Seagate aims to improve customer efficiency and reduce total cost of ownership.

Strong cash flow enables Seagate to invest in innovation, pursue acquisitions, and support growth initiatives, while also funding regular dividends and share buybacks. In the December quarter, Seagate returned $154 million to shareholders through dividends and retired $500 million in exchangeable senior notes, reducing dilution risk and maintaining financial flexibility. The company anticipates further free cash flow growth in the March quarter, supported by robust demand, operational efficiency, and disciplined capital allocation.

Seagate intends to keep capital spending within 4–6% of revenue for fiscal 2026, maintaining financial discipline as it continues to transition to HAMR technology. These strategic shifts and a strong product pipeline position Seagate for improved profitability and cash generation in the coming years.

However, Seagate faces challenges such as currency fluctuations, intense competition, and ongoing macroeconomic and supply chain uncertainties. Its high debt level—$1.05 billion in cash and equivalents versus $4.5 billion in long-term debt as of January 2, 2026—adds financial risk and may limit flexibility for future shareholder returns and acquisitions.

NetApp (NTAP): Strengths and Challenges

NetApp delivers enterprise storage solutions alongside data management software and hardware. The company’s growth is driven by its all-flash storage offerings, cloud solutions, and AI-focused products. NetApp continues to innovate, enhancing cybersecurity and expanding its cloud capabilities, which positions it for ongoing growth despite economic headwinds. Revenue streams are bolstered by intelligent data management, all-flash arrays, and hybrid cloud software as enterprises modernize their IT infrastructure.

NetApp’s modern all-flash portfolio, including the C-series and ASA block-optimized systems, is gaining traction, with the A-series also seeing increased adoption. These platforms accelerate workloads from core enterprise applications to generative AI, and management expects them to capture additional market share. By the end of the fiscal second quarter, all-flash systems accounted for 46% of the installed base under active support contracts. All-Flash Array revenue rose 9% year over year to $1 billion, with total billings up 4% to $1.65 billion.

Cybersecurity is a top priority for NetApp. The company has enhanced its ransomware resilience with AI-driven breach detection, isolated recovery, and proactive threat identification—features especially valuable in regulated industries. The release of StorageGRID 12.0 supports unstructured data growth and AI initiatives, while strengthening object storage scalability and security. NetApp is also expanding its cloud-native ecosystem with tools like Trident 25.10 and enhanced migration capabilities, ensuring relevance in containerized and hybrid environments.

NetApp’s Keystone storage-as-a-service (STaaS) solution is seeing widespread adoption, now supporting AI workloads through a consumption-based model. Keystone revenues surged 76% year over year in the fiscal second quarter, contributing to a 13.8% increase in Professional Services revenue. Unbilled remaining performance obligations (RPO) reached $456 million, up 39% year over year, indicating a strong pipeline for Keystone.

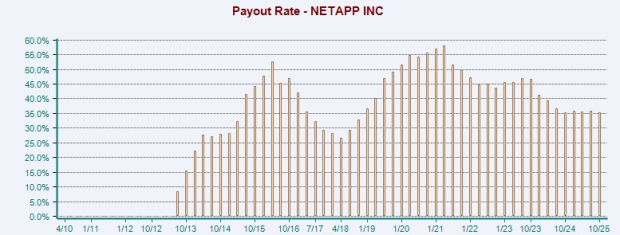

NetApp continues to return value to shareholders through buybacks and dividends, supported by healthy free cash flow. In the fiscal second quarter, the company returned $353 million to shareholders via dividends and repurchases. Over fiscal 2025, NetApp distributed $1.57 billion through these channels. The company’s cash generation is expected to sustain its current dividend payout in the near term.

Despite these strengths, NetApp remains cautious with spending due to macroeconomic uncertainty, with softness in the U.S. public sector and EMEA regions keeping revenue flat in the fiscal second quarter. Full-year fiscal 2026 revenue is projected between $6.625 billion and $6.875 billion. Delays in storage refresh cycles could impact revenue if conditions worsen. NetApp’s active acquisition strategy expands growth opportunities but also increases integration risks and has pushed goodwill and intangibles to 28.6% of total assets.

Performance and Valuation Comparison

In the past year, STX shares have soared by 294.9%, while NTAP has declined by 19.8%.

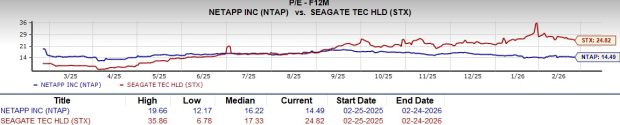

Looking at valuation, NTAP trades at 14.49 times forward earnings, compared to STX’s 24.82.

Zacks Consensus Estimates

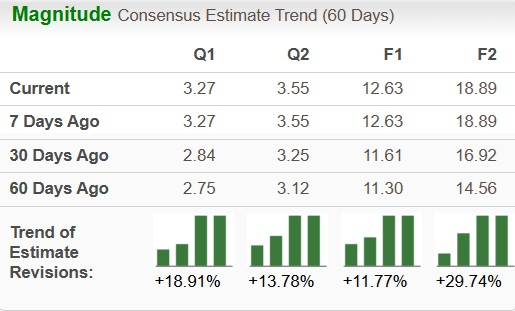

The Zacks Consensus Estimate for STX’s fiscal 2026 earnings has increased by 11.8% over the past two months, now standing at $12.63.

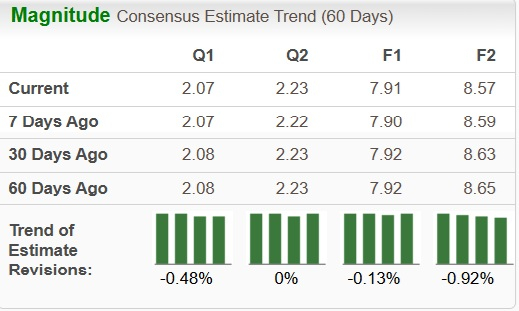

Meanwhile, the estimate for NTAP’s fiscal 2026 earnings has edged down slightly to $7.91 in the same period.

Which Stock Is the Better Choice?

Seagate is capitalizing on robust demand for AI and cloud-driven HDDs, record shipment growth, and expanding margins, with HAMR technology offering long-term potential. However, it remains sensitive to hyperscaler spending cycles, carries higher debt, and faces earnings volatility if storage demand softens. NetApp, on the other hand, benefits from the adoption of hybrid cloud and all-flash solutions, strong cloud-integrated data management, and increasing recurring software and services revenue, which provide earnings stability. Still, its growth lags more aggressive competitors, and it faces stiff competition in the cloud space and occasional sentiment swings related to guidance.

Currently, STX holds a Zacks Rank #1 (Strong Buy), while NTAP is rated Zacks Rank #3 (Hold), making STX the more favorable pick based on Zacks’ rankings.

Spotlight: Zacks’ Top Semiconductor Pick

A lesser-known company is making waves in the semiconductor industry, producing products that giants like NVIDIA do not. Positioned to benefit from the next wave of market growth, this company is just starting to gain attention—an ideal time for investors.

With impressive earnings growth and a rapidly expanding customer base, it is set to meet the surging demand for Artificial Intelligence, Machine Learning, and the Internet of Things. The global semiconductor market is expected to grow from $452 billion in 2021 to $971 billion by 2028.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Quiet Timeline, Big Setup? 5 Crypto Trades to Watch as Market Cap Signals Rally

China’s surge in oil purchases could be losing momentum

AI disruption looms over markets with US jobs data on tap

Cache Wallet Partners With InitVerse to Advance Its Web3 Multi-Chain Wallet Development Supported By Decentralized Computing