3 Key Reasons to Steer Clear of MRNA and One Alternative Stock Worth Considering

Moderna’s Recent Surge: What’s Next for Investors?

Moderna has experienced an impressive rally over the past six months, with its stock price nearly doubling to $50.65. This remarkable climb was fueled in part by strong quarterly performance, prompting many investors to reconsider their positions.

Should you consider adding Moderna to your portfolio at this stage, or is caution warranted?

Why We’re Not Bullish on Moderna

Despite its recent momentum, we remain hesitant about Moderna’s prospects. Below are three key reasons why we believe MRNA may underperform, along with an alternative stock we prefer.

1. Declining Revenue

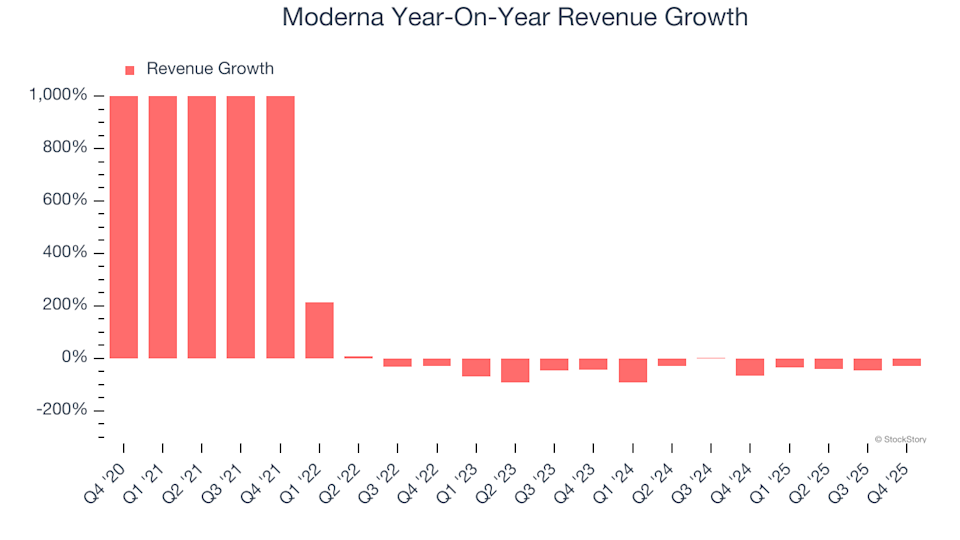

While we typically focus on long-term growth, especially in the healthcare sector, it’s important not to overlook recent shifts. Moderna’s revenue trajectory has reversed sharply, with annualized declines of 46.7% over the past two years—marking a significant departure from its previous five-year trend.

Moderna Year-On-Year Revenue Growth

2. Falling Earnings Per Share

We closely monitor changes in earnings per share (EPS) to assess whether a company’s growth is translating into profitability. Over the last five years, Moderna’s EPS has dropped at an average rate of 30.2% per year, deepening its losses. Persistent declines in EPS often signal shifting industry dynamics and can leave companies vulnerable to sharp declines in share price, especially when their margin of safety is thin.

Moderna Trailing 12-Month EPS (Non-GAAP)

3. Worsening Free Cash Flow Margin

Although free cash flow isn’t always highlighted in financial reports, it’s a crucial indicator because it reflects all operating and capital expenditures—making it difficult to manipulate. Over the past five years, Moderna’s free cash flow margin has dropped significantly. While there may have been a recent uptick, investors are likely hoping for a return to historical levels. For the trailing 12 months, Moderna’s free cash flow margin stood at a negative 106%, suggesting the company may be in the midst of a heavy investment cycle.

Moderna Trailing 12-Month Free Cash Flow Margin

Our Verdict

We appreciate companies that contribute to better health outcomes, but in Moderna’s case, we’re staying on the sidelines. After its recent surge, the stock is trading at $50.65 per share, with a forward price-to-sales ratio of 9.8. The market generally values companies like Moderna based on their expected profits over the next year, but current forecasts anticipate ongoing losses. Given the limited upside and considerable risks, we believe there are more attractive opportunities elsewhere.

Stocks We Prefer Over Moderna

This year’s market gains have been concentrated in just a handful of stocks—four companies account for half of the S&P 500’s total increase. Such concentration can make investors uneasy. While many chase the same popular names, savvy investors are seeking out high-quality businesses that are flying under the radar and trading at more reasonable valuations. Discover our top picks in this month’s Top 5 Growth Stocks—a curated selection of high-quality companies that have delivered a 244% return over the past five years (as of June 30, 2025).

Our list features well-known leaders like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Tecnoglass, which achieved a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump’s latest global tariffs ‘opened a new Pandora's box with no good exits’ – Mind Money’s Khandoshko

Government Bonds Are Becoming Less Attractive, Warns New York Fed

AMDY Achieves 75.8% Yield: How the Market Has Already Factored It In

AWS's $50 billion gamble: Charting the trajectory of AI infrastructure