Salesforce’s Earnings Are the Software Market’s AI Moment of Truth

Salesforce reports after the close on Wednesday, February 25, 2026, and it’s shaping up as another referendum on whether “AI eats software” is a real earnings problem or just a narrative with good PR. Workday’s post-print slide (and subsequent recovery) has helped the group’s tone a bit: the initial guidance-driven hit mattered, but the dip-buying matters more because it suggests the software tape may be moving from panic to price discovery. SalesforceCRM+2.42% is a bigger test because it sits right at the intersection of the fear (seat deflation, DIY agents, budget reallocation) and the counterargument (embedded workflows, data gravity, and an app-layer distribution machine that can package AI and charge for it).

What analysts are looking for starts with the basics: Wall Street consensus sits around adjusted EPS of about $3.05 on revenue around $11.18–$11.19 billion for the quarter. More important is whether the “AI helps the platform” story shows up in forward indicators rather than just in buzzwords. In the last reported quarter (fiscal Q3), Salesforce posted revenue of $10.26 billion (+9% y/y) and reported current remaining performance obligation (cRPO) of $29.4 billion (+11% y/y). Management also pointed to Agentforce and Data 360 reaching nearly $1.4 billion in ARR (+114% y/y), with Agentforce ARR disclosed at $540 million (+330% y/y). Those are the “proof points” bulls will anchor to; the bears will ask whether those figures are still small relative to the installed base and whether they’re meaningfully bending the revenue curve.

The cleanest way to watch for erosion is to treat this as a bookings/backlog print masquerading as an AI debate. First, focus on cRPO growth and total RPO trajectory. cRPO is the near-term backlog proxy and tends to be a better “temperature check” than revenue in a quarter where execution timing can move deals around. Salesforce itself emphasized cRPO strength in Q3 as evidence of pipeline health. If cRPO growth decelerates materially versus the prior quarter’s ~11% level, that will feed the “AI is slowing seat-based expansion” narrative fast. Second, scrutinize any commentary on deal cycles, downsell/rightsizing, and renewals. AI-driven “seat deflation” is ultimately a renewal math issue: fewer seats, lower per-seat, or more discounting to keep logos. That won’t always show up immediately in headline revenue, but it will show up in booking quality, renewal discussions, and forward-looking commentary.

Agentforce is the headline product, but the market is going to grade it like a CFO: attach rate, time to production, and monetization, not demo velocity. Recent channel commentary cited by analysts suggests pilots and trials are increasingly converting into paying contracts and add-ons, which is exactly what Salesforce needs to prove this is a real product cycle rather than a “free trial forever” feature. Watch for updates that separate “customers experimenting” from “customers in production,” and any disclosure that ties Agentforce to broader platform expansion (multi-cloud wins, Data Cloud pull-through, higher net new ACV/AOV). If management can credibly argue that Agentforce improves core cloud retention/expansion (Sales, Service, Platform, Integration/Analytics, Slack), it becomes a defense against the disruption narrative: even if AI changes workflows, Salesforce is the system of record that gets to monetize the change.

On guidance: Salesforce previously raised its fiscal 2026 revenue outlook to about $41.45–$41.55 billion and lifted adjusted EPS guidance into the ~$11.75–$11.77 range range around the fiscal Q3 report, so investors will be looking for any reaffirmation or tightening, plus how much of the story is “AI-driven upside” versus normal execution. For the quarter specifically, some previews note Salesforce’s own ranges that bracket consensus (revenue roughly in the low-$11B range and EPS around the low-$3 range), which puts extra weight on commentary and forward indicators because the bar for “in-line” is already well set. If the company guides conservatively on cRPO growth or implies macro softness in key verticals, the market will assume the AI “help” isn’t offsetting budget scrutiny yet.

So what should you watch for if you’re trying to judge whether the business is wearing down underneath the AI noise?

Core demand health: any signs of slower new logo adds, more downsell at renewal, longer deal cycles, or heavier discounting. These are the first real-world fingerprints of “AI disruption” because they reflect buyer behavior, not product announcements.

Bookings/backlog quality: cRPO and any billings/booking commentary. When investors are nervous, backlog is the lie detector.

Mix shift and margin: Salesforce has shown strong non-GAAP margin performance recently; if AI attach requires materially higher costs (model usage, infrastructure, services) without monetization, margins will tell you before revenue does.

Agentforce reality checks: ARR growth is great, but what matters now is conversion to production, expansion within the installed base, and whether it’s incremental (new dollars) versus substitutive (discounted bundles).

Analyst framing is split in a familiar way: the bullish camp argues fears of rapid SaaS displacement are overstated and that Salesforce is strategically positioned in the AI ecosystem (apps + data + workflow), while the more cautious camp acknowledges better feedback but wants proof the revenue/backlog curve is bending meaningfully higher. That makes this print less about “did they beat EPS by a nickel” and more about whether management can show that AI is a growth accelerant rather than a seat-count reducer.

Finally, on the stock: the $175 area you cited matters as a potential bottom, but a true V-shaped recovery is always the market’s way of saying “we panicked efficiently.” If the report is clean and the forward indicators hold (especially cRPO), a move back toward $200 is plausible; if cRPO or demand commentary cracks, the tape will assume the software group’s “AI anxiety” still has more chapters. Either way, Salesforce is likely to set the tone for enterprise software in the near term—because if the category leader can’t narrate AI as additive, everyone else will be doing it with a tremor.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Daily Mirror-owner faces largest loss in ten years as Google traffic declines

Target’s newly appointed CEO reveals his strategy for revitalizing the company

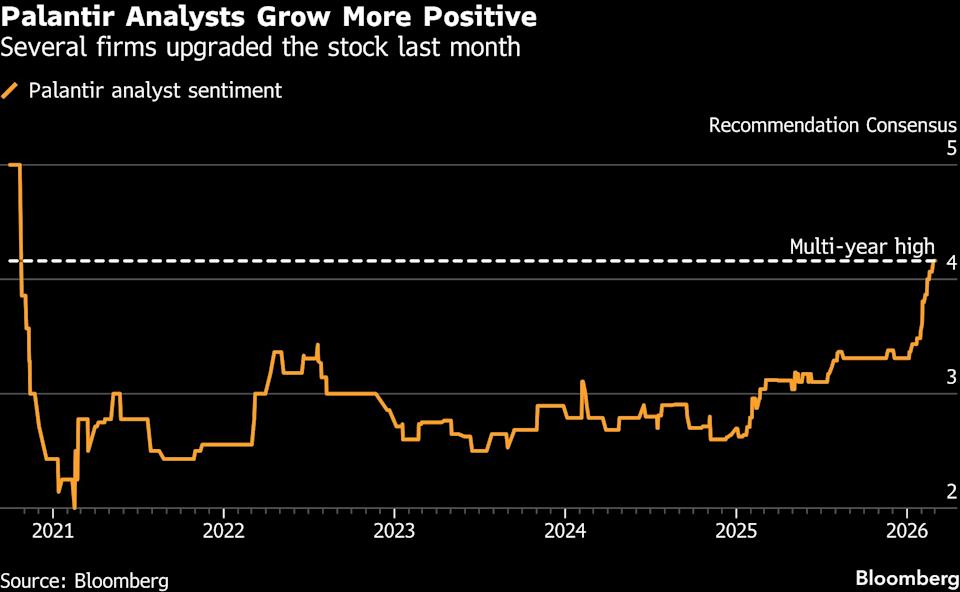

Palantir Returns to Wall Street’s Recommended Stocks Following a 38% Drop

Options Income Daily: MU, SOFI, CRWV and More