Root (NASDAQ:ROOT) Delivers Strong Q4 CY2025 Numbers, Stock Jumps 12.2%

Digital auto insurance company Root (NASDAQ:ROOT) reported Q4 CY2025 results

Is now the time to buy Root?

Root (ROOT) Q4 CY2025 Highlights:

- Net Premiums Earned: $367.3 million vs analyst estimates of $355.2 million (22.6% year-on-year growth, 3.4% beat)

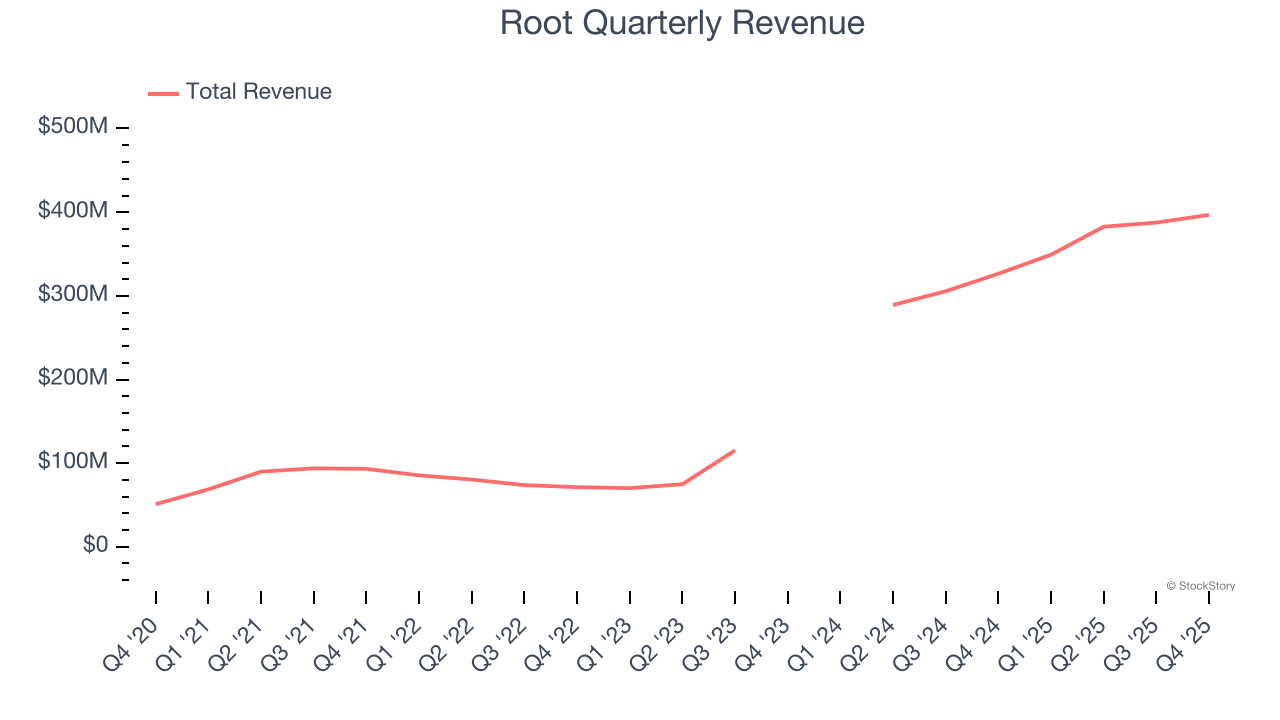

- Revenue: $397 million vs analyst estimates of $384.4 million (21.5% year-on-year growth, 3.3% beat)

- Combined Ratio: 99.7% vs analyst estimates of 105% (575 basis point beat)

- EPS (GAAP): $0.31 vs analyst estimates of -$0.48 (significant beat)

- Market Capitalization: $896.6 million

Company Overview

Pioneering a data-driven approach that rewards good driving habits, Root (NASDAQ:ROOT) is a technology-driven auto insurance company that uses mobile apps to acquire customers and data science to price policies based on individual driving behavior.

Revenue Growth

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services. Luckily, Root’s revenue grew at an incredible 34.3% compounded annual growth rate over the last five years. Its growth beat the average insurance company and shows its offerings resonate with customers.

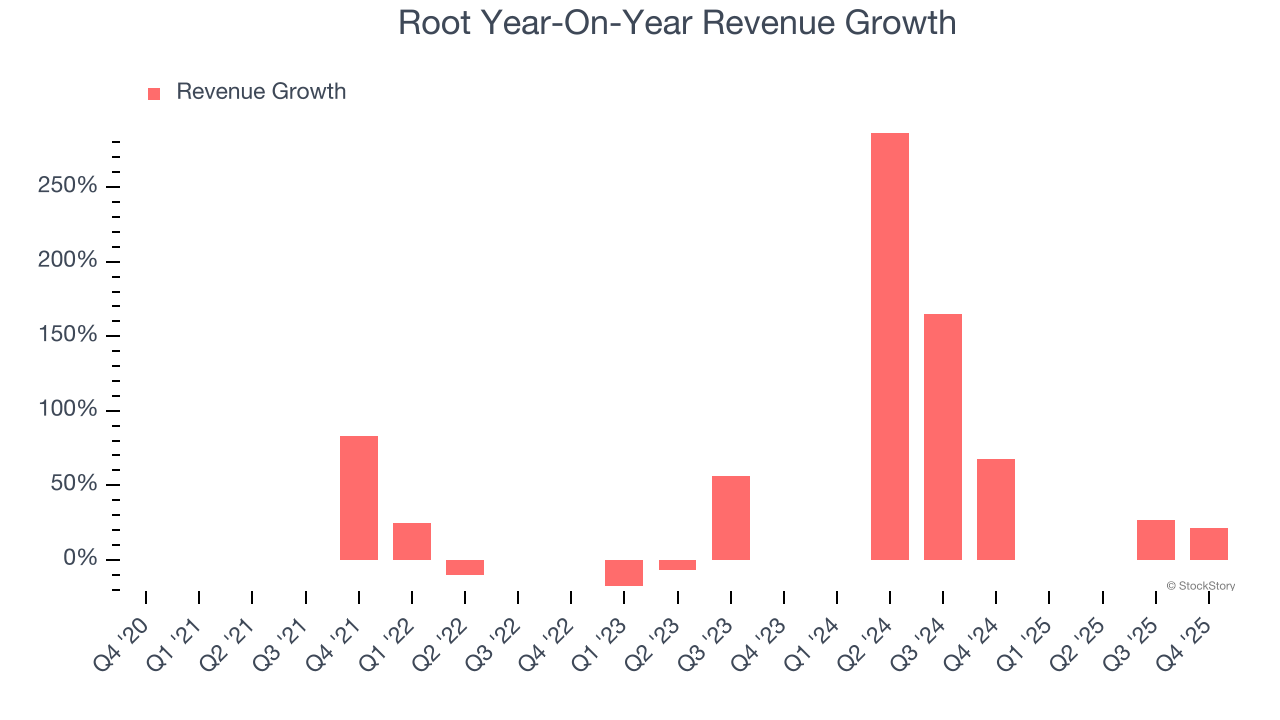

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Root’s annualized revenue growth of 82.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Root reported robust year-on-year revenue growth of 21.5%, and its $397 million of revenue topped Wall Street estimates by 3.3%.

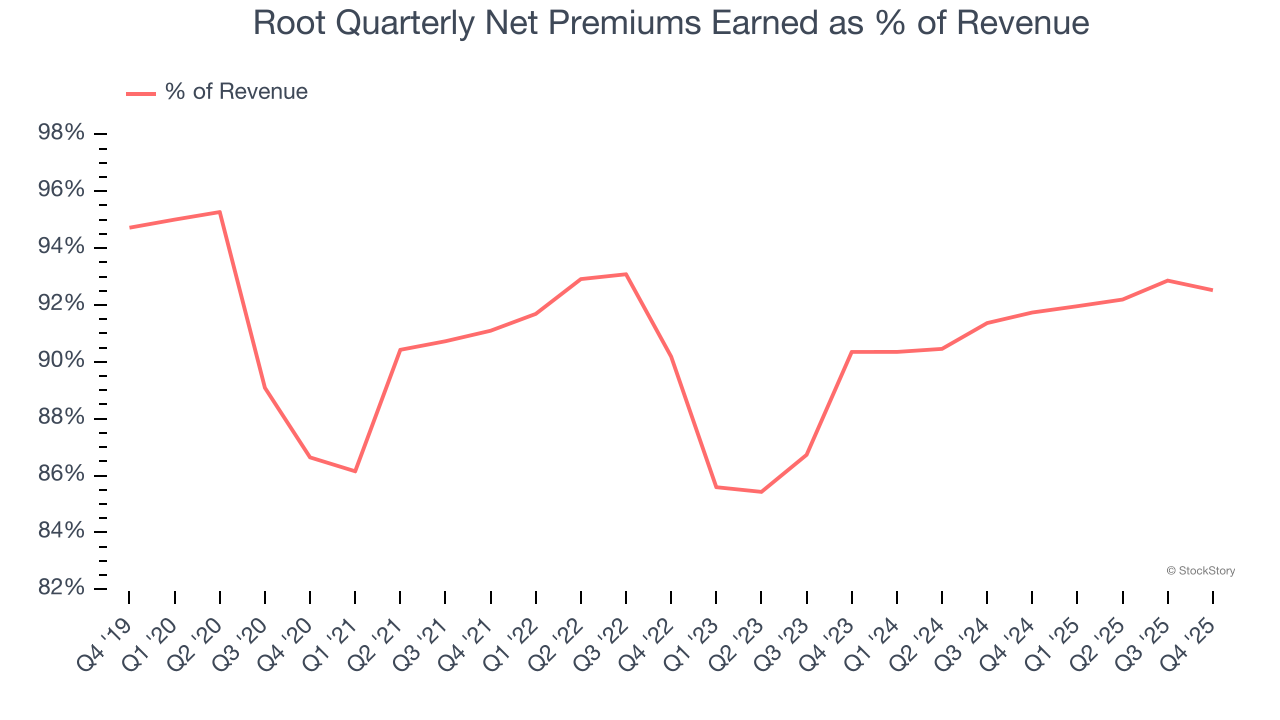

Net premiums earned made up 91.2% of the company’s total revenue during the last five years, meaning Root lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Our experience and research show the market cares primarily about an insurer’s net premiums earned growth as investment and fee income are considered more susceptible to market volatility and economic cycles.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking.

Net Premiums Earned

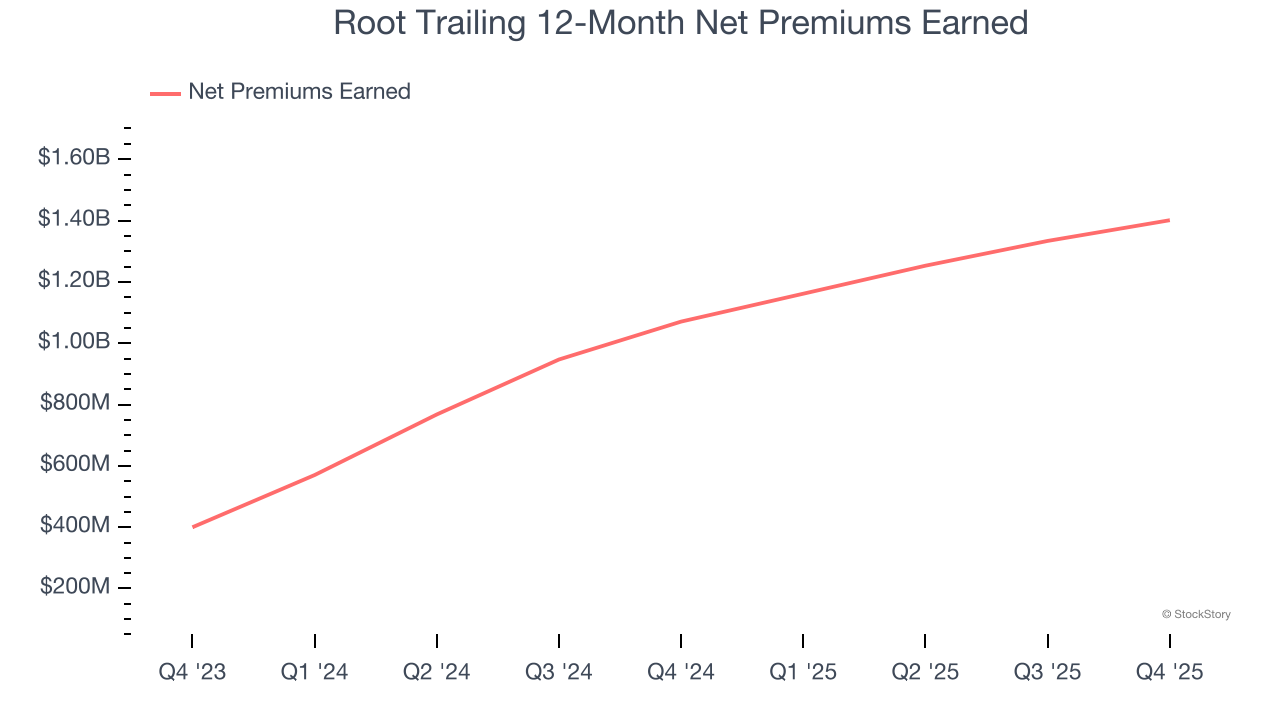

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore gross premiums less what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Root’s net premiums earned has grown at a 34.2% annualized rate over the last five years, much better than the broader insurance industry and in line with its total revenue.

When analyzing Root’s net premiums earned over the last two years, we can see that growth accelerated to 87.2% annually. Since two-year net premiums earned grew faster than total revenue over this period, it's implied that other line items such as investment income grew at a slower rate. While these additional streams certainly contribute to the bottom line, their impact can vary. Some firms have shown greater success and long-term consistency in investing their float compared to peers. However, sharp fluctuations in the fixed income and equity markets can significantly affect short-term performance.

Root produced $367.3 million of net premiums earned in Q4, up a hearty 22.6% year on year and topping Wall Street Consensus estimates by 3.4%.

Key Takeaways from Root’s Q4 Results

It was good to see Root beat analysts’ EPS expectations this quarter. We were also excited its net premiums earned outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 12.2% to $68.50 immediately after reporting.

Root had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

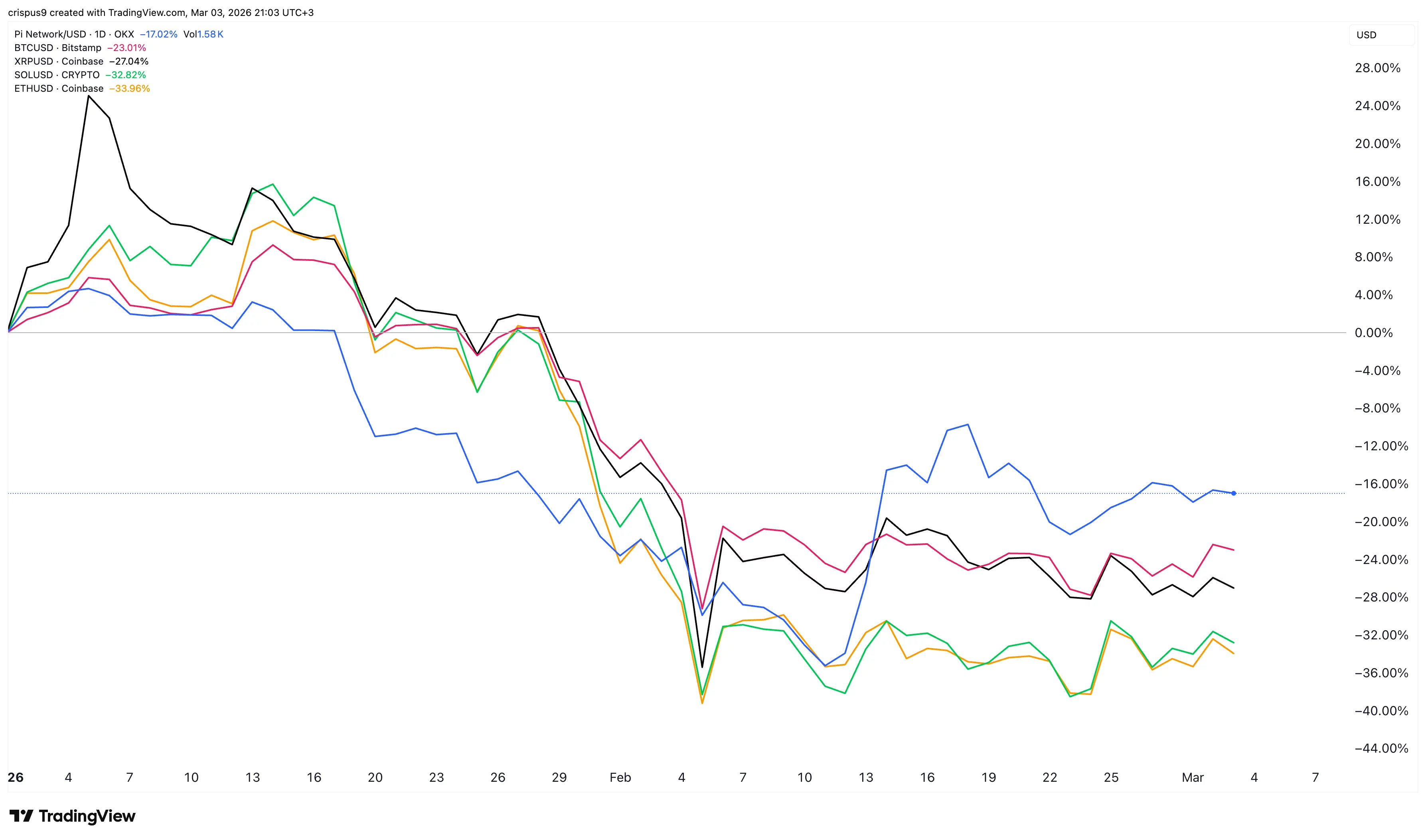

Here’s why Pi Network is suddenly beating Bitcoin, XRP, and Solana

Unemployment has returned forcefully. The extent of its impact remains uncertain.

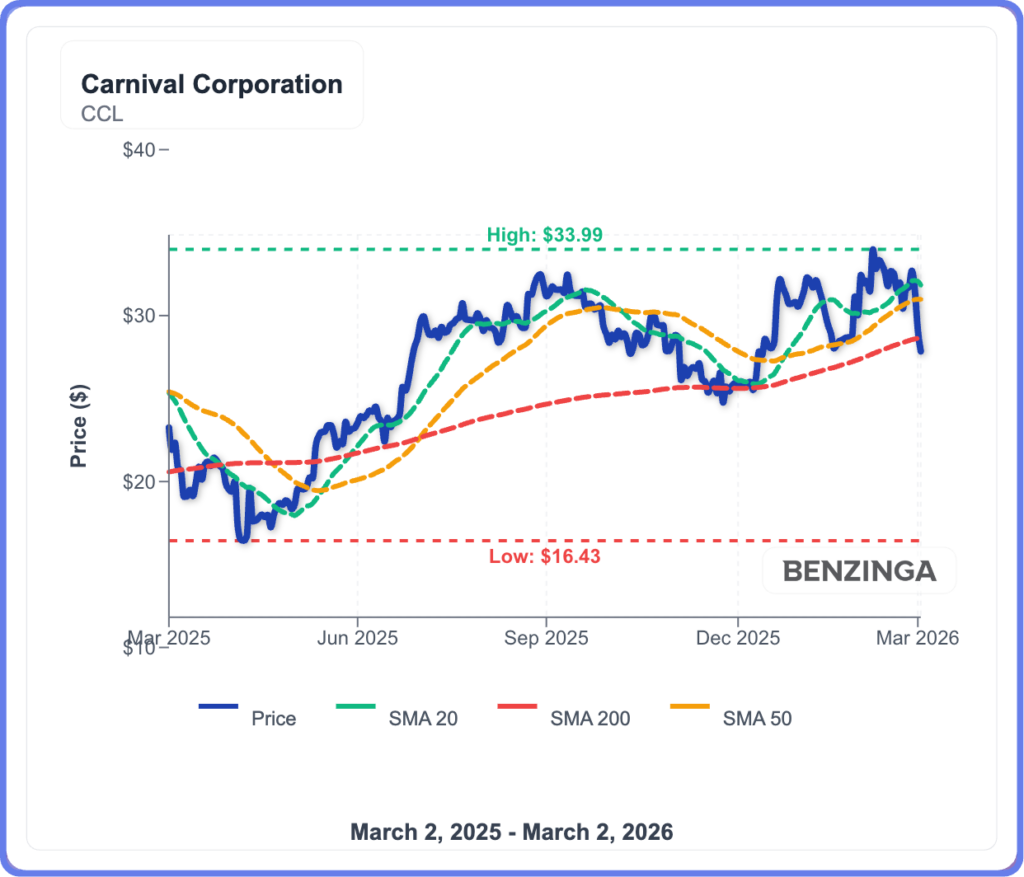

Carnival Stock Extends Sell-Off As Norwegian Outlook Pressures Sector

Suzano vs. Klabin: A Value Investor’s Perspective on Leading Pulp & Paper Companies