Magnite (NASDAQ:MGNI) Falls Short of Q4 CY2025 Revenue Projections

Magnite (MGNI) Q4 2025 Earnings Overview

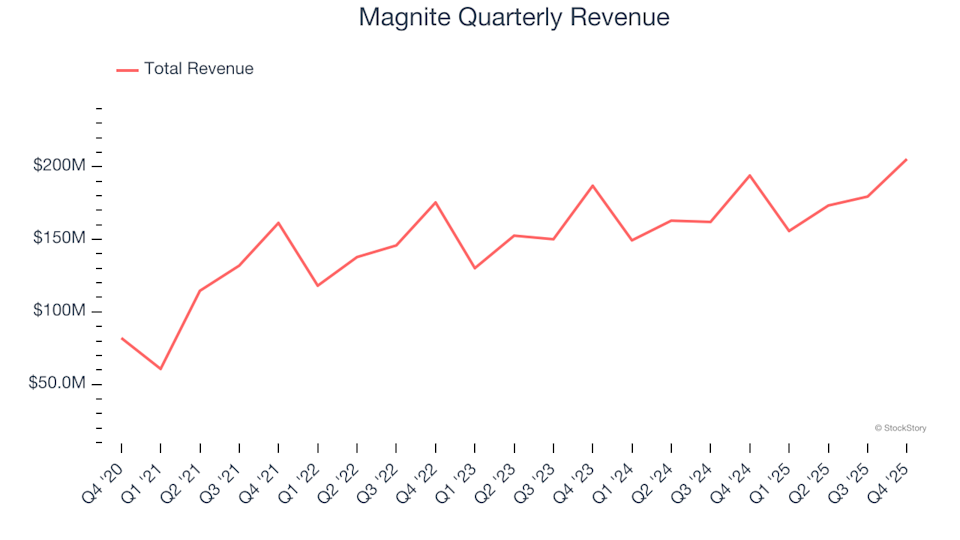

Magnite, a digital advertising platform listed on NASDAQ as MGNI, reported fourth-quarter sales of $205.4 million for calendar year 2025, marking a 5.9% increase compared to the previous year. However, this figure fell short of Wall Street’s revenue expectations. The company’s adjusted earnings per share came in at $0.34, which was 3.9% below analyst forecasts.

Quarterly Highlights

- Revenue: $205.4 million, compared to analyst projections of $211.2 million (5.9% year-over-year growth, 2.8% below estimates)

- Adjusted EPS: $0.34, versus expectations of $0.35 (3.9% below estimates)

- Adjusted EBITDA: $52.93 million, missing analyst estimates of $80.88 million (25.8% margin, 34.6% below expectations)

- Operating Margin: 25.3%, up from 20.7% in the same period last year

- Free Cash Flow Margin: 50.2%, down from 57.2% a year ago

- Market Cap: $1.68 billion

Michael G. Barrett, Magnite’s CEO, commented, “We’re thrilled to see a notable shift in the growth trajectory of the programmatic CTV market, highlighted by our 32% top-line growth excluding political spending in Q4 and continued momentum into Q1. Spending is moving toward CTV from other digital advertising segments, including DV+. Magnite’s technology, partnerships, and team position us as a leading force in CTV, which now accounts for over half of our business in Q1.”

About Magnite

Magnite was formed in 2020 through the merger of Rubicon Project and Telaria. Today, it operates the largest independent sell-side advertising platform, streamlining the buying and selling of digital ad inventory across multiple channels and formats.

Revenue Performance

Examining a company’s sales over time helps gauge its overall strength. While any business can have a strong quarter, sustained growth over years is a sign of resilience.

Magnite generated $714 million in revenue over the past year, making it a relatively small player in the business services sector. While this size can limit advantages enjoyed by larger competitors, it also allows for faster expansion.

Over the past five years, Magnite achieved an impressive annualized revenue growth rate of 26.4%, indicating robust demand compared to many peers in the industry.

Although we focus on long-term growth, recent industry changes can impact performance. Magnite’s annualized revenue growth over the last two years was 7.3%, lower than its five-year average, but still reflects healthy demand.

Recent Revenue Trends

This quarter, Magnite’s revenue increased by 5.9% year-over-year to $205.4 million, missing analyst expectations.

Looking forward, analysts anticipate revenue growth of 14.3% over the next year, suggesting that new products and services may drive stronger results.

Operating Margin Analysis

While Magnite was operationally profitable this quarter, it has faced challenges over the longer term. The company’s high costs have resulted in an average operating margin of -6.6% over the past five years. Unprofitable business services firms require careful scrutiny, as they may be vulnerable during downturns.

On a positive note, Magnite’s operating margin improved by 31 percentage points over the last five years, thanks to sales growth providing leverage. However, sustained profitability will require further progress.

In Q4, Magnite posted an operating margin of 25.3%, up 4.6 percentage points from the previous year, reflecting greater efficiency.

Earnings Per Share (EPS)

Revenue growth shows demand, but changes in EPS reveal how profitable that growth is. Sometimes, companies boost sales through heavy spending, which can impact profitability.

Magnite’s EPS has grown at a remarkable 57.1% compound annual rate over the past five years, outpacing its revenue growth. This indicates improved profitability per share as the company expanded.

Looking deeper, Magnite’s operating margin expansion was a major driver behind its higher earnings, aside from revenue growth. While interest and taxes also affect EPS, they don’t provide as much insight into core performance.

Shorter-term EPS analysis helps spot recent changes. Magnite’s two-year annual EPS growth rate was 26.2%, below its five-year trend, but still strong. We hope to see this accelerate in the future.

For Q4, Magnite reported adjusted EPS of $0.34, matching last year’s figure but missing analyst estimates. Wall Street expects Magnite’s full-year EPS to reach $0.86 in the next 12 months, representing a 28.3% increase.

Summary of Q4 Results

Overall, Magnite’s latest quarter was underwhelming, with both revenue and EPS falling short of expectations. Following the report, shares dropped 2.1% to $11.72. While one quarter doesn’t determine a company’s long-term prospects, it’s important to consider valuation, business fundamentals, and recent earnings before making investment decisions.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Concentra's Q4 Beat: Was the Good News Already Priced In?

Sinclair’s Prices Climb While Technical Indicators Signal Caution

AXT’s Strong Technicals Clash With Weak Fundamentals

Bitcoin Drops to $65K Again as ETH, XRP and Solana Followed