Fidelis Insurance (NYSE:FIHL) Posts Q4 CY2025 Revenue That Falls Short of Analyst Projections

Fidelis Insurance Q4 CY2025 Earnings Overview

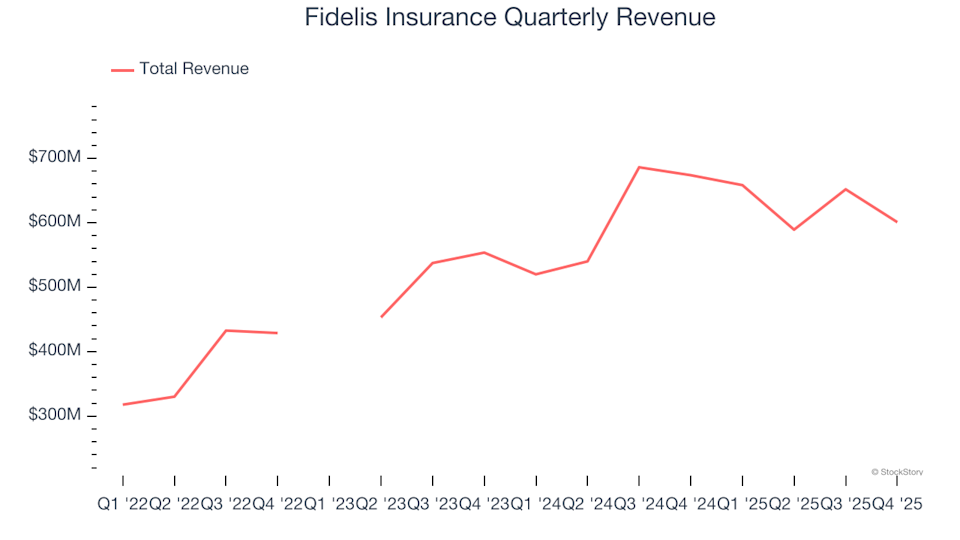

Fidelis Insurance (NYSE: FIHL), a provider of specialty insurance, reported fourth-quarter 2025 results that did not meet Wall Street's revenue projections. The company posted $600.9 million in sales, reflecting a 10.8% decrease compared to the same period last year. However, its adjusted earnings per share came in at $1.09, slightly surpassing analyst expectations by 1.3%.

Quarterly Performance Highlights

- Net Premiums Earned: $552.9 million, falling short of the $621.3 million forecast (down 12.9% year-over-year, 11% below estimates)

- Total Revenue: $600.9 million, missing the $706.8 million estimate (down 10.8% year-over-year, 15% below expectations)

- Combined Ratio: 80.6%, outperforming the analyst estimate of 84.5% by 390 basis points

- Adjusted EPS: $1.09, slightly above the $1.08 consensus (1.3% beat)

- Book Value per Share: $24.61, matching the $24.51 estimate (up 12.3% year-over-year)

- Market Capitalization: $2.07 billion

Dan Burrows, CEO of Fidelis Insurance Group, remarked, "Our strong fourth quarter, highlighted by an 80.6% combined ratio and an annualized Operating ROAE of 18.3%, underscores the robustness of our platform and our consistent execution of our capital allocation strategy."

About Fidelis Insurance

Established in Bermuda in 2014, Fidelis Insurance (NYSE: FIHL) operates globally in the specialty insurance and reinsurance sector. The company is committed to delivering value through strategic capital deployment, expert risk management, and a network of enduring underwriting partnerships, enabling it to adapt swiftly to changing market dynamics.

Revenue Trends

Insurance companies generate income through three main avenues: underwriting (premiums earned), investment returns from the float (premiums held before claims are paid), and fees from services such as policy administration and annuities. Over the past three years, Fidelis Insurance achieved an impressive compound annual revenue growth rate of 24.4%, outperforming industry averages and indicating strong customer demand.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company's ongoing business fundamentals.

While we value long-term growth, it's important to consider recent shifts in interest rates, market performance, and industry trends. Fidelis Insurance's annualized revenue growth over the past two years was 9.2%, which is lower than its three-year average but still suggests steady demand.

Recent Revenue and Premiums Analysis

This quarter, Fidelis Insurance reported a 10.8% year-over-year drop in revenue, totaling $600.9 million and missing analyst forecasts. Net premiums earned accounted for 78.6% of total revenue over the last four years, highlighting the central role of insurance operations in the company's business model.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company's ongoing business fundamentals.

Market participants tend to prioritize growth in net premiums earned over investment and fee income, viewing it as a key indicator of underwriting performance and market reach.

Book Value Per Share (BVPS)

Insurance companies rely on their balance sheets, collecting premiums upfront and paying claims over time. The float—premiums not yet paid out—are invested, creating assets supported by liabilities. Book value per share (BVPS) measures these assets minus liabilities, representing the value available to shareholders.

BVPS is a crucial metric for insurers, offering insight into business quality. Unlike earnings per share, which can fluctuate due to one-off items or accounting adjustments, BVPS reflects sustained capital growth and is less susceptible to manipulation.

Fidelis Insurance's BVPS grew at a modest 8.8% annual rate over the past two years. Looking ahead, consensus forecasts anticipate BVPS to rise by 30% to $24.51 in the next 12 months—a notably strong growth rate.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company's ongoing business fundamentals.

Summary of Q4 Results

This quarter's results offered few positives. Both revenue and net premiums earned fell short of expectations, and overall performance was lackluster. Following the announcement, the stock price remained unchanged at $20.10.

Should you invest in Fidelis Insurance? The latest quarter is just one aspect of the company's broader business quality. Evaluating quality alongside valuation is key to making informed investment decisions.

Industry Perspective

Technology continues to reshape industries, fueling demand for solutions that support software developers—whether it's monitoring cloud infrastructure, integrating multimedia, or enabling seamless content streaming.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Lucrative Stocks We View with Prudence

THOR Prepares to Announce Second Quarter Results: What Investors Should Know

KB Plunges 4.55% Amid Regulatory Overhaul Hints and Sector Turmoil

T1 Energy Drops 14%: What Caused the Sharp Decline?