Veracyte’s Fourth Quarter Outperformance: Opportunity for Traders or Reflected in the Price?

Veracyte’s Recent Performance: What’s Driving the Stock?

The primary reason for Veracyte’s recent momentum is its impressive fourth-quarter results. The company posted total revenue of $140.6 million, marking a 19% increase compared to the previous year and surpassing analyst expectations. While this headline figure is strong, it’s important to note that the growth was mainly fueled by higher average selling prices and collections from previous periods, rather than a significant uptick in the number of Decipher tests performed. This distinction suggests that the revenue beat was more about pricing and timing than a fundamental surge in patient testing volume.

More notably, Veracyte saw a dramatic improvement in profitability. For the full year, GAAP net income soared by 175% to $66.4 million, reflecting substantial margin gains. This wasn’t just a one-off event—adjusted EBITDA reached $42.3 million in Q4, accounting for 30.1% of revenue, and the company finished the year with a robust $412.9 million in cash. These results highlight a business operating with much greater efficiency.

Historically, such strong earnings beats have triggered sharp market reactions. After the third-quarter report, Veracyte’s stock jumped over 26% on the back of a positive earnings surprise. However, with the recent Q4 beat, there’s a risk that the market has already factored in much of this good news. Unless future growth is driven by a sustained increase in test volume rather than temporary pricing benefits, the stock may struggle to surprise investors again. The next phase depends on whether Veracyte can shift from growth driven by pricing and collections to growth powered by organic test volume increases.

Looking Ahead to 2026: Guidance and Market Expectations

Veracyte’s management has reaffirmed its outlook for 2026, offering a clear view of what’s ahead. The company expects total revenue to grow by 10% to 13%, reaching between $570 million and $582 million. Additionally, they are targeting an adjusted EBITDA margin of approximately 25%, up from around 21% in 2024. This margin improvement signals ongoing operational leverage and a focus on profitability.

However, the projected revenue growth rate represents a slowdown from the 16% increase seen in 2025. This deceleration is a key point of concern. After a year of robust expansion, investors will be watching closely to see if Veracyte can maintain its momentum or if growth is beginning to taper off.

On the positive side, Veracyte’s strong cash reserves—totaling $412.9 million at year-end—provide significant flexibility. This financial strength reduces immediate pressure to meet aggressive targets and allows the company to fund new initiatives, such as the launch of Prosigna LDT, without the need for additional capital.

Overall, the company’s guidance suggests a steady, sustainable approach, prioritizing profitability and cash flow over rapid top-line growth. While this provides a solid foundation, it may also limit the potential for dramatic stock price appreciation. Investors will need to decide if this measured strategy justifies the current valuation, especially after the recent earnings-driven rally.

Key Catalysts and Risks to Monitor

The upcoming earnings call, scheduled for 4:30 p.m. Eastern Time on Wednesday, February 25, 2026, is the next major event for Veracyte. The market will be focused on management’s comments regarding trends in Decipher test volumes. Confirmation that growth is shifting from pricing and collections to increased testing volume would support a more durable growth narrative.

One risk is that the company’s 2026 outlook may not fully reflect potential gains from new products. UBS has pointed out that Veracyte’s current revenue targets might underestimate the impact of upcoming launches, such as Prosigna LDT and other pipeline offerings. If management signals stronger-than-expected adoption of these products, it could indicate that the stock is undervalued and that there is upside to the $570–$582 million revenue target.

Another important metric is the adjusted EBITDA margin. The company is aiming for about 25%, up from 21% in 2024. Any indication that margins could exceed this target would be a positive surprise and could provide fresh momentum for the stock, especially given the recent rally following the Q3 results.

What’s Next for Veracyte?

The February 25th earnings call is a pivotal moment for Veracyte. The company’s future trajectory depends on whether management can demonstrate that growth is becoming more volume-driven and that new products are making a meaningful contribution. Any deviation from the current guidance could create significant trading opportunities.

Investment Perspective: A Tactical Opportunity

Veracyte’s current setup presents a tactical opportunity for investors. UBS has maintained a Buy rating with a $48 price target, suggesting about 26% upside from recent levels. This target is based on the company’s strong Q4 performance and improving margins. However, the stock’s reaction to the upcoming earnings call will be crucial in determining whether this bullish outlook remains valid or if the positive news is already reflected in the share price.

Key technical levels to monitor include the recent high near $38 and the 50-day moving average. If management fails to confirm a shift toward volume-driven growth for the Decipher test, the stock could retreat from these highs. While the market has rewarded Veracyte for its earnings beats, it also quickly adjusts to new information. If the earnings call reveals that new products are contributing more than expected, the stock could move toward the $48 target. Otherwise, the recent gains may not be sustainable. For now, Veracyte remains a tactical play, with the outcome of the earnings call likely to set the direction.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Marriott International Shares Beating the S&P 500 Index?

特朗普团队拟取消7500美元电动汽车税收抵免,电动汽车股大跌

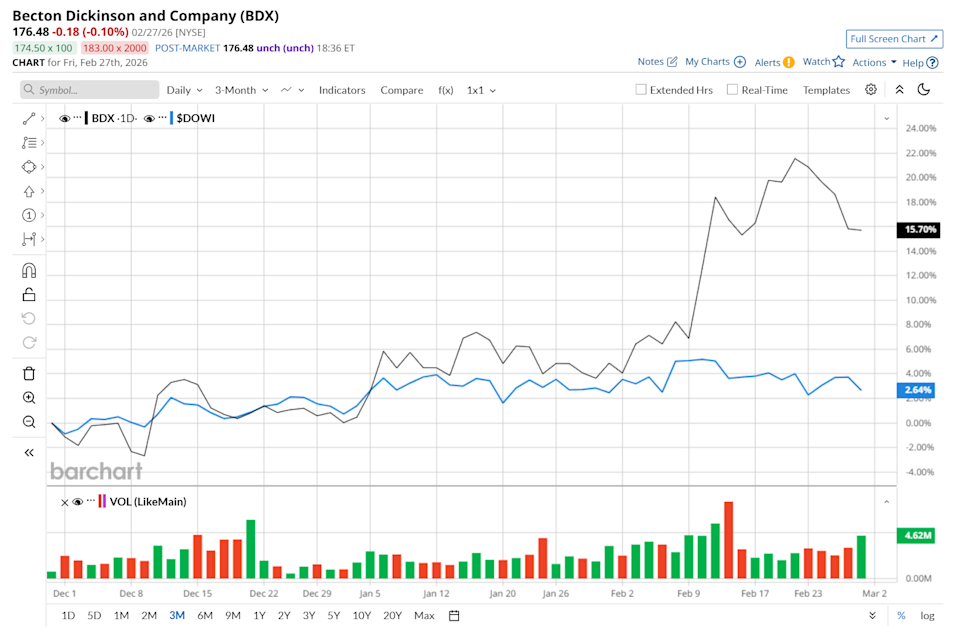

Is Becton, Dickinson and Company Shares Beating the Dow's Performance?

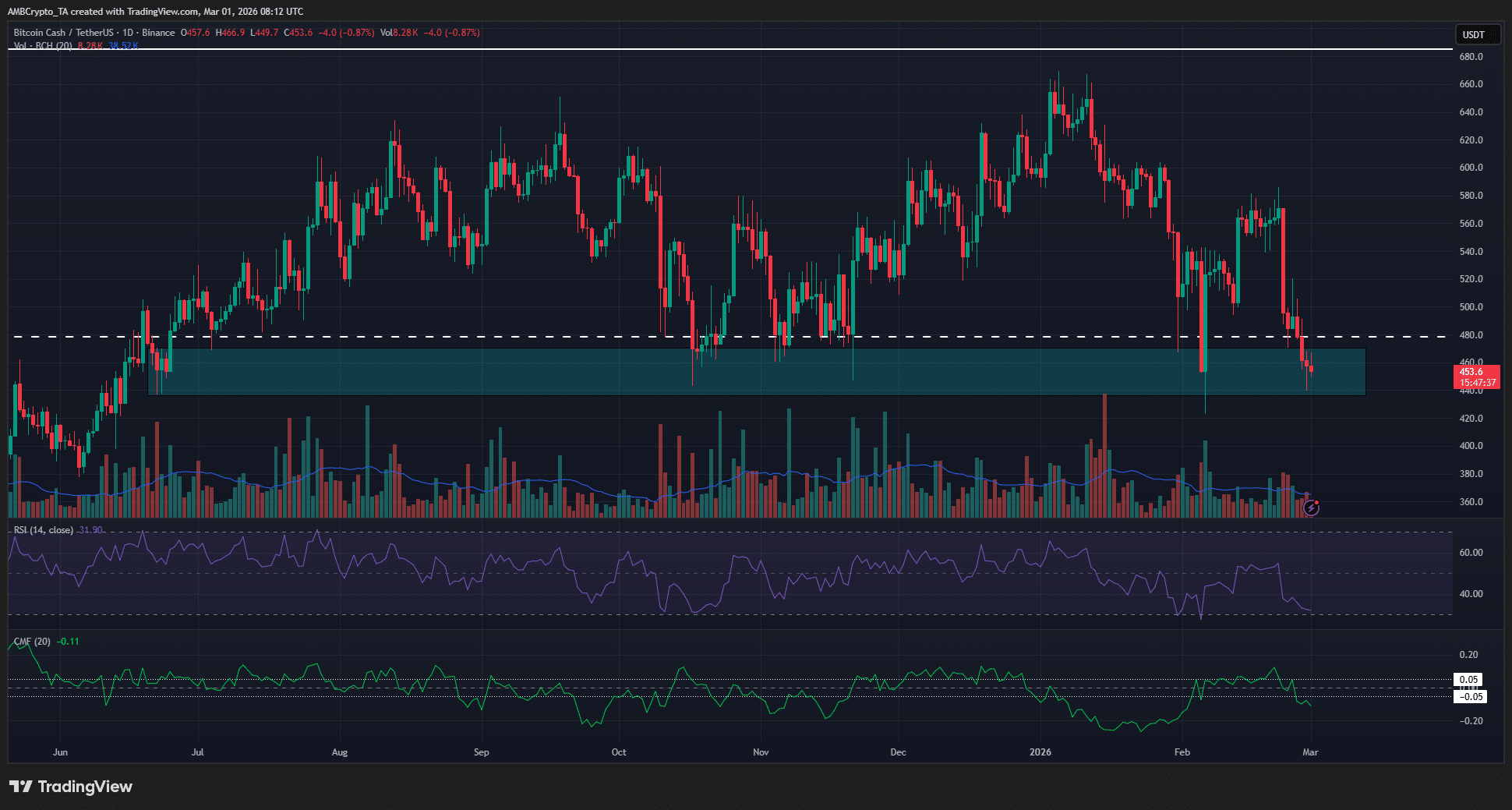

Crypto market’s weekly winners and losers – DOT, NEAR, BCH, PEPE