The Honest Company (NASDAQ:HNST) Reports Q4 CY2025 In Line With Expectations But Stock Drops

Personal care company The Honest Company (NASDAQ:HNST)

Is now the time to buy The Honest Company?

The Honest Company (HNST) Q4 CY2025 Highlights:

- Revenue: $88.04 million vs analyst estimates of $88.19 million (11.8% year-on-year decline, in line)

- EPS (GAAP): -$0.21 vs analyst estimates of $0.02 (significant miss)

- Adjusted EBITDA: $3.75 million vs analyst estimates of $3.91 million (4.3% margin, relatively in line)

- EBITDA guidance for the upcoming financial year 2026 is $21.5 million at the midpoint, above analyst estimates of $20.87 million

- Operating Margin: -27.5%, down from -1% in the same quarter last year

- Free Cash Flow was $18.06 million, up from -$17.17 million in the same quarter last year

- Market Capitalization: $252.6 million

"Our fourth quarter delivered results in line with our expectations and provides clear momentum as we enter 2026," said Chief Executive Officer, Carla Vernón.

Company Overview

Co-founded by actress Jessica Alba, The Honest Company (NASDAQ:HNST) sells diapers and wipes, skin care products, and household cleaning products.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

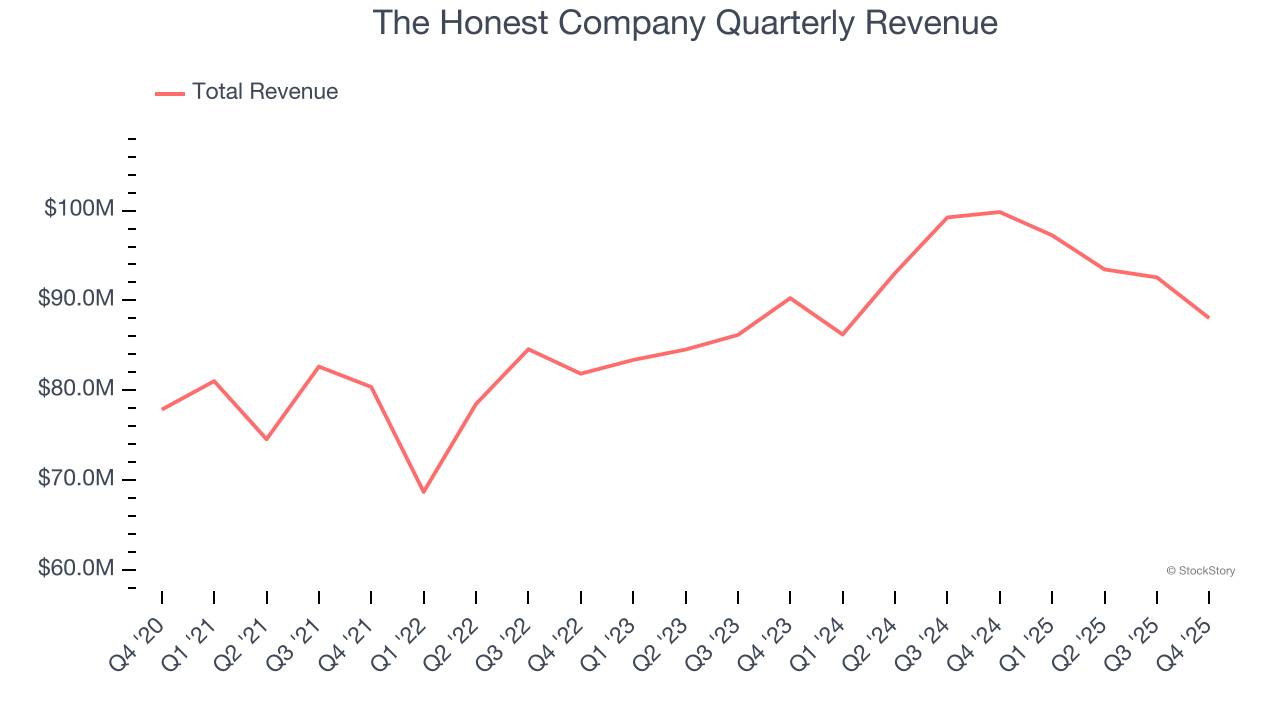

With $371.3 million in revenue over the past 12 months, The Honest Company is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, The Honest Company grew its sales at a mediocre 5.8% compounded annual growth rate over the last three years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

This quarter, The Honest Company reported a rather uninspiring 11.8% year-on-year revenue decline to $88.04 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 7.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products will see some demand headwinds.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking.

Cash Is King

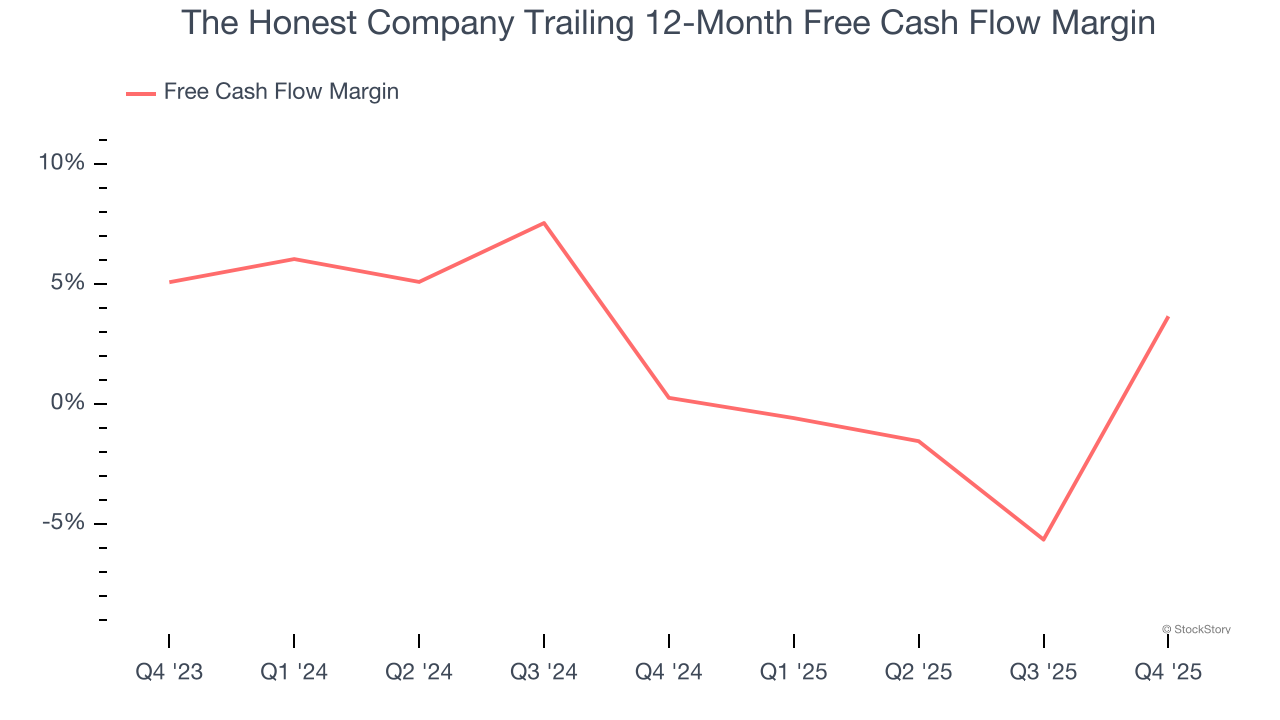

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

The Honest Company has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, subpar for a consumer staples business.

Taking a step back, an encouraging sign is that The Honest Company’s margin expanded by 3.4 percentage points over the last year. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

The Honest Company’s free cash flow clocked in at $18.06 million in Q4, equivalent to a 20.5% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

Key Takeaways from The Honest Company’s Q4 Results

It was encouraging to see The Honest Company’s full-year EBITDA guidance beat analysts’ expectations. On the other hand, its gross margin missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5.1% to $2.20 immediately after reporting.

The Honest Company’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Brazil's monetary council expands airlines' access to public aviation fund

Algoma Steel Group Inc. to Announce 2025 Fourth Quarter and Full Year Results March 11, 2026

Fox Factory Holding: Fourth Quarter Earnings Overview

Black Diamond Group: Fourth Quarter Earnings Overview