Goldman Sachs Research Report: Asset Repricing in the AI Era—From Asset-Light to HALO Heavy Assets

Hello everyone, this is Youdou.

On February 24, 2026, Goldman Sachs released a strategic report:

"The HALO Effect: Heavy Assets, Low Obsolescence in the AI Era"

The report proposes a framework:

HALO = Heavy Assets + Low Obsolescence

Heavy Assets + Low Technological Obsolescence Risk

In the AI era, will market leadership shift back from "light assets" to "heavy assets"?

Goldman Sachs provides a new framework—HALO—as the answer.

I. From "Asset-Light" to "Asset-Heavy": What Is the Market Repricing?

Over the past decade or so, the core logic of global capital markets has been very clear.

Zero interest rates, abundant liquidity, and extremely low discount rates.

The most favored companies were "long-duration assets"—high growth, high profit margins, highly scalable, and almost non-reliant on heavy asset investment.

Software, platforms, internet, SaaS, digital economy.

That was an era of "asset-light".

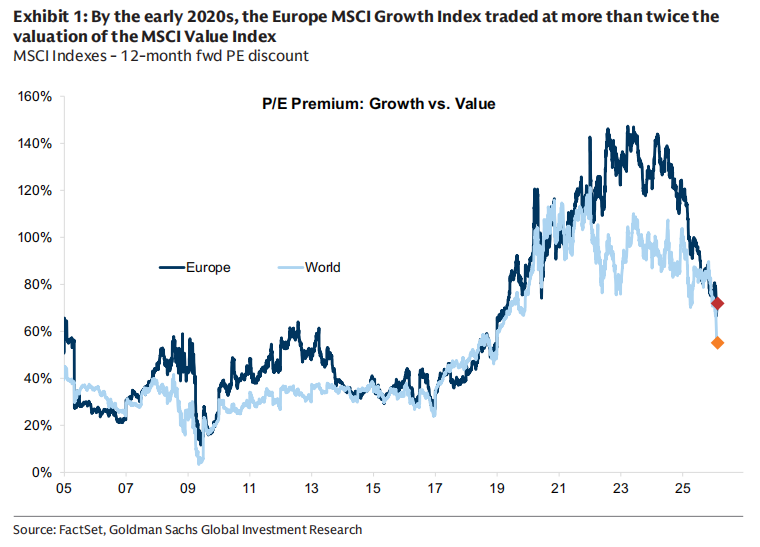

Goldman Sachs reviews in the report that around 2020, the valuation premium of MSCI Growth over Value exceeded 100%, and European growth stocks were once at a 150% premium.

But this structure was broken by the inflation shock after the pandemic.

Supply chain restructuring, Russia-Ukraine conflict, energy security, geopolitical fragmentation, fiscal expansion, rising real interest rates.

Capital began to rethink one thing:

What is "scarcity"?

Energy systems are scarce.

Power grids are scarce.

Transport infrastructure is scarce.

Heavy industrial capacity is scarce.

They are expensive, have long construction cycles, complex regulations, and cannot be quickly replicated.

When real interest rates rise and discount rates go up, the appeal of "future profits" declines, while "real capacity" regains its premium.

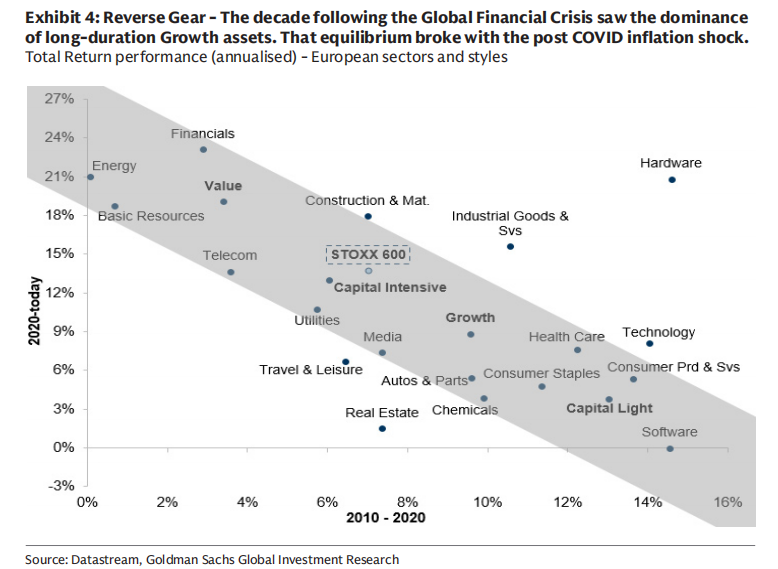

The report shows that since 2025, companies with high capital intensity have significantly outperformed those with low capital intensity, and the valuation gap between the two types of assets has clearly narrowed.

This is not simply a decline in growth stocks, but a re-rating of heavy assets.

II. AI: A Double Blow to "Asset-Light"

AI appears to further strengthen technology, but Goldman Sachs believes it puts "double pressure" on the asset-light model.

The first is at the business model level.

AI is compressing the moat of the software and information processing industry.

As information processing costs drop dramatically, many "differentiation capabilities" are quickly commoditized, leading the market to reassess the long-term profit margins and terminal values of software, IT services, publishing, gaming, and even some asset management businesses.

The recent valuation pullback in the software sector is not due to a collapse in profits, but an adjustment in "terminal value assumptions".

The second is at the capital expenditure level.

More interestingly—

AI is at the same time turning some of the most classic "asset-light" companies into the largest capital spending machines in history.

Goldman Sachs points out that since the release of ChatGPT in 2022, the five major US cloud giants are expected to invest about $1.5 trillionin capital expenditure from 2023 to 2026, far exceeding the previous historical cumulative total of about $600 billion.

In 2026 alone, these companies' capital expenditures could exceed $650 billion.

What does this mean?

It means—

Tech giants in the AI era are themselves becoming heavy-asset industrial enterprises.

Computing power, electricity, data centers, cooling systems, transmission networks...

These are all real assets.

III. What is HALO?

Goldman Sachs proposes a framework:

HALO —— Heavy Assets, Low Obsolescence

Two core characteristics:

Heavy Assets:

The business model is built upon a large amount of physical assets, with high replication costs, long construction cycles, and restrictions due to regulation or engineering complexity.Low Obsolescence:

Assets do not rapidly depreciate with technological upgrades and maintain long-term economic relevance.

Typical industries include:

Power grids

Pipelines

Utilities

Transport infrastructure

Critical industrial equipment

Long-cycle manufacturing capabilities

These assets do not rely on "conceptual upgrades," but on "physical presence."

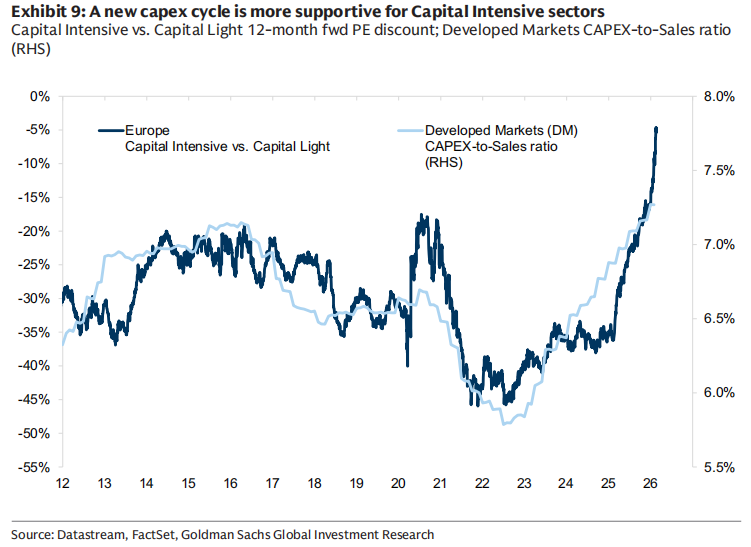

Goldman Sachs built a capital intensity scoring model, integrating six indicators such as the proportion of fixed assets, capital expenditure intensity, capital-labor ratio, etc., to distinguish capital-intensive from asset-light enterprises.

Within this framework, utilities, energy, resources, and communications are clearly capital-intensive;

Software, internet, media, and digital platforms are on the asset-light side.

IV. Driving Factors: Why Now?

The report lists several macro variables:

1. Interest Rate Structure

Capital-intensive stocks tend to perform better in a high interest rate environment, as higher discount rates compress long-duration asset valuations, while physical assets benefit from nominal growth and fiscal expansion.

2. Manufacturing Cycle

When the manufacturing PMI outperforms the services PMI, capital-intensive industries usually perform better.

3. Value Style Comeback

Capital intensity is highly correlated with value style. Recently, European value funds have seen inflows, while growth has seen outflows.

But in the long run, investors are still underweight value.

4. Earnings Momentum

Goldman Sachs expects capital-intensive companies to have a compound EPS growth of about 14% over the next few years, higher than the roughly 10% of asset-light companies.

At the same time, ROE for capital-intensive enterprises is expected to improve, while ROE for asset-light enterprises may remain stable.

This is a structural shift in earnings expectations.

My understanding:

This report discusses a more fundamental question:

In the AI era, what are the truly "scarce assets"?

In the past decade, scarcity was algorithms, code, platforms.

Now, scarcity may be in electricity, copper mines, transmission grids, engineering capability, industrial systems.

AI is not the "ultimate form of the asset-light era."

On the contrary, it makes the physical infrastructure of the real world even more important.

This is not just a simple style rotation.

It's more like an asset repricing under the combined effects of discount rates, inflation structure, geopolitical patterns, and technological revolution.

Of course, whether this structure can persist still depends on the path of interest rates, the realization speed of AI profits, and the global economic cycle.

But one thing is certain:

When tech companies start spending $1.5 trillion to build computing power,

when energy and power grids become prerequisites for AI,

the market's valuation logic for "physical assets" has already changed.

This may be the true meaning of HALO.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US Treasury yields move up as oil prices climb and concerns about inflation increase

Hyperliquid's Token Rises as Weekend Iran Shock Finds Few Open Markets

72 Hours of Life and Death! Decisive Factors That Will Determine the Market's Next Move

AUD/JPY trades above 111.00 after paring recent losses