Vipshop’s 2025 Performance: Delivering Strong Cash Flow Amid a Competitive Discount Market

Vipshop 2025 Performance: A Showcase of Financial Discipline

Vipshop’s 2025 financial results highlight a company with strong operational control. The firm achieved market expectations for both its quarterly and annual revenues, reporting RMB32.5 billion in Q4 revenue and RMB105.9 billion for the full year. Notably, profitability remained robust, with net income attributable to shareholders rising to RMB2.6 billion in the fourth quarter. This solid bottom line underpins Vipshop’s reputation for reliable cash generation.

Vipshop’s ability to generate cash is a key attraction for institutional investors. In Q4 alone, the company produced RMB5.5 billion in operating cash flow, contributing to a total of RMB7.5 billion for the year. This healthy liquidity enabled Vipshop to return US$944.1 million to shareholders in 2025 through dividends and share repurchases. Such disciplined use of surplus cash is characteristic of a well-established, cash-rich business.

Growth Outlook: Stability Over Rapid Expansion

Looking forward, Vipshop’s revenue guidance for Q1 2026—RMB26.3 to 27.6 billion—suggests modest growth of 0% to 5% year-over-year. For institutional investors, this signals a shift from aggressive expansion to a focus on converting steady revenue into high-quality cash flow and returning value to shareholders. In an environment where discounts are prevalent, the company’s strong cash generation and prudent capital allocation stand out as key advantages.

Industry Trends: Discounting Drives Structural Change

The broader retail landscape is undergoing a significant transformation, with discounting becoming a central theme in 2025. What began as a consumer strategy has evolved into a sector-wide movement, as evidenced by major retailers like JD.com and Meituan launching physical discount stores. This shift emphasizes operational efficiency and value, validating Vipshop’s business model. By offering branded goods at reduced prices, Vipshop attracts a loyal customer base seeking quality bargains and provides brands with an effective channel to move excess inventory without harming their premium image.

However, this favorable trend also intensifies competition. The rapid adoption of "Hard Discount" strategies by companies such as Hema and Wumart has heightened the focus on cost control and efficiency. For Vipshop, the challenge lies in maintaining its pricing power and profit margins as the industry becomes increasingly competitive and cost-driven. While the company’s expertise and established partnerships offer advantages, the sector’s race to lower costs could put pressure on the margins that support Vipshop’s strong cash flow.

Portfolio Implications: Balancing Opportunity and Risk

From an investment perspective, Vipshop’s resilience in a changing Chinese retail environment makes it a compelling candidate for portfolios focused on the discount retail theme. Nevertheless, the sector’s volatility and the risk of shrinking margins remain concerns. The key for investors is Vipshop’s ability to sustain profitability and scale efficiently amid intensifying competition, which will ultimately determine its risk-adjusted returns.

Institutional Sentiment and Valuation: Navigating Uncertainty

Vipshop’s fundamentals are solid, with disciplined capital management and consistent cash returns to shareholders. However, institutional sentiment and valuation present a more nuanced picture. For instance, North of South Capital recently reduced its stake from 6.3% to 3.6% of its reportable assets, likely as part of a portfolio rebalancing rather than a negative view on Vipshop’s business model. The fund continues to hold a significant position, and Vipshop remains profitable while executing its buyback program.

Broader institutional analysis points to weak short- and medium-term sentiment and increased downside risk, even as the long-term outlook remains positive. This creates a tension between the company’s strong cash flow and the market’s concerns about near-term volatility. The stock’s five-year performance—a 48.6% decline—reflects ongoing skepticism and underperformance.

For investors, this sets up a clear trade-off. Vipshop’s disciplined capital allocation and steady buybacks provide support for earnings, but the market’s caution about execution in a highly competitive environment means uncertainty remains. The investment case depends on one’s time horizon: while long-term value may be present, short-term volatility is likely, requiring patience and conviction.

Key Catalysts and Risks for Re-Rating

Vipshop’s potential for a portfolio re-rating depends on several forward-looking factors that will test its cash flow strength amid rising competition and macroeconomic uncertainty. Investors should monitor liquidity trends and sector developments for signs of increased confidence or emerging challenges.

- Capital Allocation: Watch for continued or accelerated share buybacks, such as the recent US$305.4 million ADS repurchase in Q4. Sustained buybacks would signal management’s confidence in the company’s value proposition. Also, observe changes in institutional ownership; while North of South Capital’s reduction is notable, broader stability or increases among major holders would indicate renewed institutional support.

- Market Share Gains: Vipshop’s ability to leverage its discount model to capture share from traditional retailers will be crucial. Evidence of widening operating margins or faster-than-expected revenue growth would demonstrate the model’s resilience and leadership in the evolving retail landscape.

- Consumer Spending Trends: The main risk is a downturn in consumer spending, especially in discretionary categories, which could disproportionately impact the discount segment. While Vipshop’s cash flow provides some protection, prolonged margin pressure from weaker demand would challenge the investment thesis.

In conclusion, the path to a higher valuation for Vipshop involves maintaining strong capital allocation, achieving market share growth, and navigating consumer spending trends. Success in these areas would reinforce the company’s long-term potential, while setbacks could keep the stock trading at a discount despite its operational strengths.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Marriott International Shares Beating the S&P 500 Index?

特朗普团队拟取消7500美元电动汽车税收抵免,电动汽车股大跌

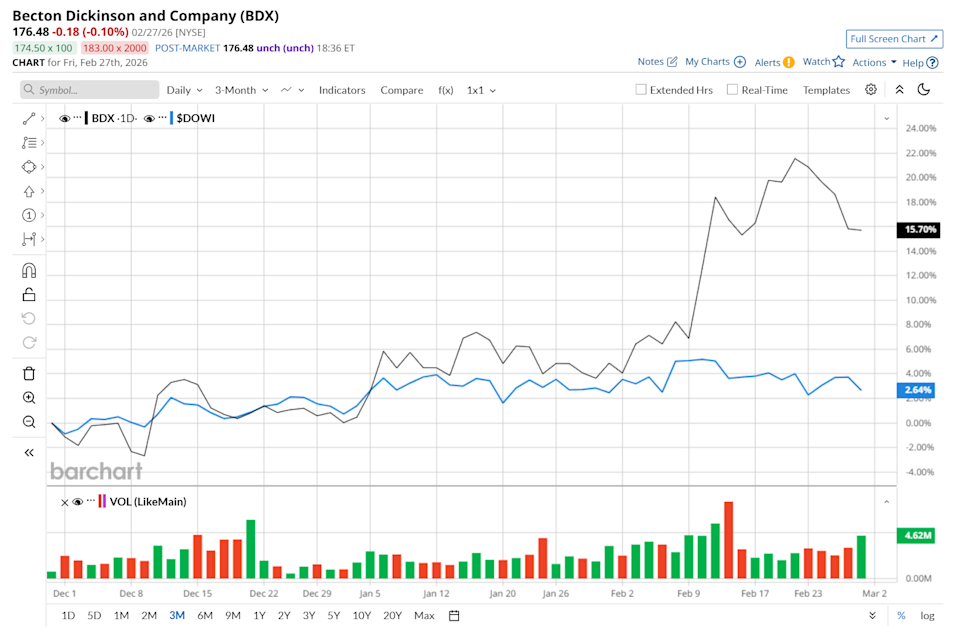

Is Becton, Dickinson and Company Shares Beating the Dow's Performance?

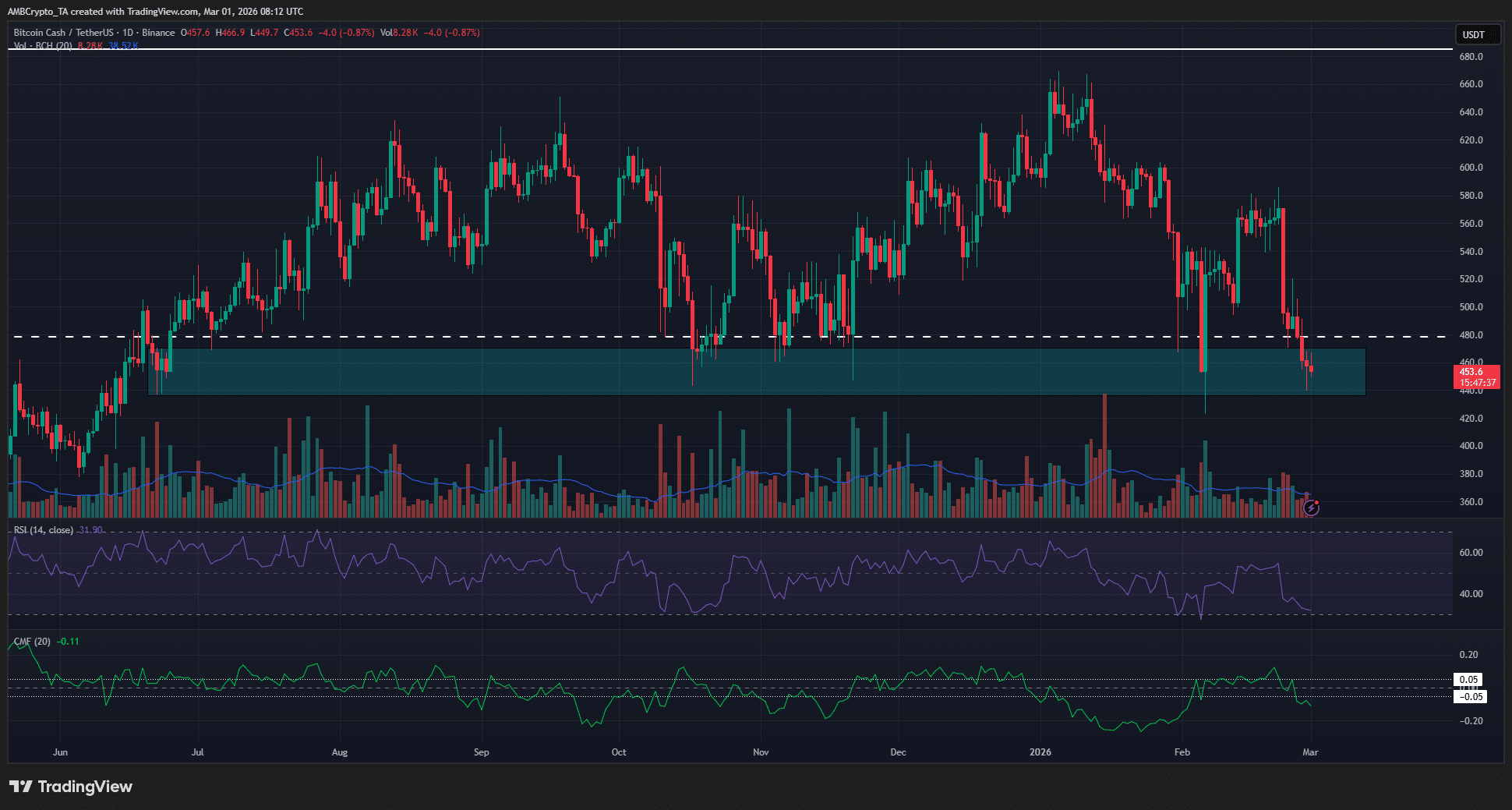

Crypto market’s weekly winners and losers – DOT, NEAR, BCH, PEPE