3 Reasons to Steer Clear of BL and One Alternative Stock Worth Buying

BlackLine’s Recent Performance: A Tough Stretch for Investors

BlackLine has faced a challenging half-year, with its share price tumbling 38% to $32.81. This significant drop has left many shareholders uneasy and questioning their next move.

Should you consider adding BlackLine to your investment portfolio now, or is caution warranted?

Why We’re Not Enthusiastic About BlackLine

Despite the lower valuation, we’re not convinced BlackLine is a compelling buy at this time. Below are three key reasons for our skepticism, along with an alternative stock we prefer.

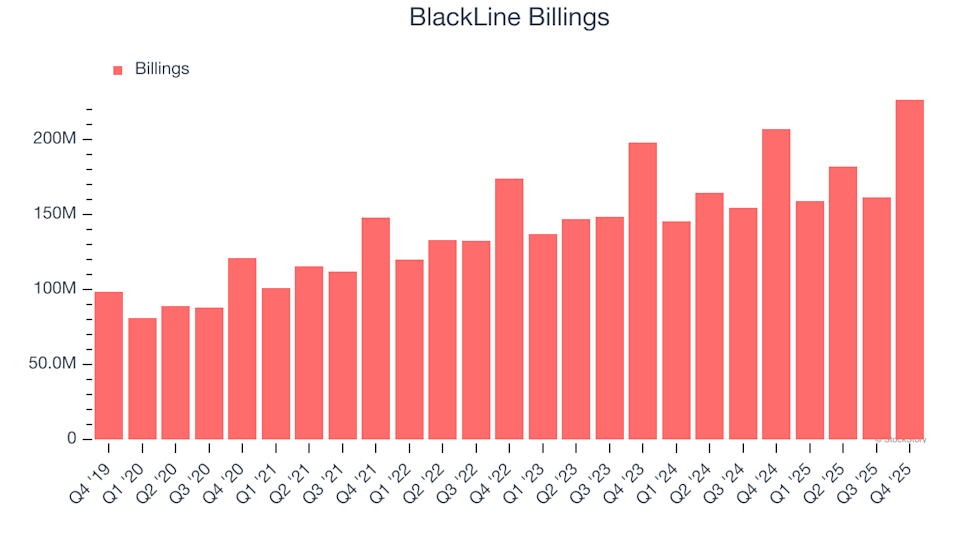

1. Sluggish Billings Signal Weak Demand

Billings, sometimes referred to as “cash revenue,” reflect the total payments collected from customers within a given period, differing from revenue, which is recognized over the duration of contracts.

In the fourth quarter, BlackLine reported $226.9 million in billings. Over the past year, billings have grown by an average of just 8.5% year-over-year—a lackluster result that points to intensifying competition and difficulties in attracting and retaining clients.

2. Customer Retention Challenges Impact Long-Term Prospects

One of the main advantages of the software-as-a-service (SaaS) model is the expectation that customers will increase their spending over time, supporting higher valuation multiples for these businesses.

BlackLine’s net revenue retention rate—a measure of how much existing customers from a year ago are spending today—stood at 104% in Q4. This means that, even without acquiring new clients, BlackLine’s revenue would have grown by 4.3% over the past year.

While this retention rate suggests BlackLine is maintaining its customer base, it falls short of the 120%+ rates seen at leading SaaS companies.

3. Stagnant Operating Margin Raises Concerns

Although many software firms highlight their adjusted profits (excluding stock-based compensation), we focus on GAAP operating margin, as stock-based compensation is a real cost tied to attracting and keeping talent. This metric reveals how much profit remains after all core expenses, including cost of goods sold, sales, and R&D, are accounted for.

Looking at BlackLine’s profitability, its operating margin has shown little improvement over the past two years, remaining relatively flat. This is concerning, as revenue growth should ideally lead to better cost efficiency and higher profitability. For the trailing twelve months, BlackLine’s operating margin was 3.6%.

Our Verdict

While BlackLine is not a poor business, it doesn’t meet our investment criteria. After its recent decline, the stock trades at three times forward price-to-sales (or $32.81 per share), which is a reasonable valuation. However, we lack confidence in the company’s future prospects and believe there are more attractive opportunities elsewhere. For example, consider one of our top picks in digital advertising.

Better Alternatives to BlackLine

It’s important to keep your portfolio forward-looking, as the risks associated with crowded trades continue to rise.

The next generation of high-growth stocks can be found in our Top 5 Strong Momentum Stocks for this week. This handpicked group of high-quality companies has delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Comfort Systems, which achieved a 782% five-year return. Discover your next winning investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

PBOC sets USD/CNY reference rate at 6.9124 vs. 6.9088 previous

Iraqi Supply Disruption May Reveal True Constraints of OPEC's Spare Capacity

APPLE formed the worst Bearish Cross that can crash it to $205

Surpassing FTX-Era Lows: 38% Of Altcoins Hit Record Lows As Liquidity Abandons The Crypto Fringe