J. M. Smucker (NYSE:SJM) Surpasses Q4 CY2025 Forecasts, Shares Surge

J.M. Smucker Surpasses Q4 CY2025 Revenue Forecasts

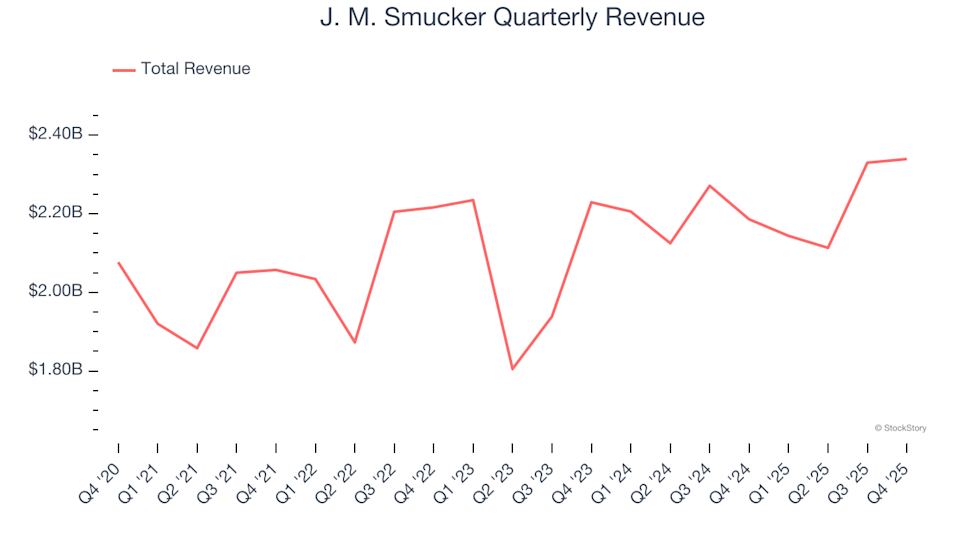

J.M. Smucker (NYSE:SJM), a leader in packaged foods, reported fourth-quarter revenue of $2.34 billion for CY2025, marking a 7% increase compared to the previous year and exceeding analyst projections. The company’s adjusted earnings per share reached $2.38, outperforming consensus estimates by 5.2%.

Curious if J.M. Smucker is a smart investment right now?

Highlights from J.M. Smucker’s Q4 CY2025 Performance

- Revenue: $2.34 billion, surpassing the $2.33 billion analyst estimate (7% year-over-year growth, 0.5% above expectations)

- Adjusted EPS: $2.38, beating the $2.26 forecast (5.2% above estimates)

- Adjusted EBITDA: $548.4 million, compared to the $499.9 million estimate (23.4% margin, 9.7% beat)

- Management reaffirmed its full-year Adjusted EPS outlook at $9 (midpoint)

- Operating Margin: -23.4%, an improvement from -27.2% in the same period last year

- Free Cash Flow Margin: 20.8%, up from 6.9% a year ago

- Sales Volumes: Decreased 2% year-over-year (compared to a 5% decline last year)

- Market Cap: $11.37 billion

“Our business continues to perform well despite a challenging environment. In the third quarter, both net sales and adjusted EPS exceeded our expectations, highlighting the resilience of our leading brands and our disciplined approach to cost management,” commented Mark Smucker, CEO, President, and Board Chair.

About J.M. Smucker

J.M. Smucker is widely recognized for its fruit spreads and jams, but its product range extends to peanut butter, coffee, and pet food, making it a significant player in the packaged foods industry.

Examining Revenue Trends

Consistent revenue growth is a hallmark of a strong business. While any company can have a standout quarter, sustained expansion over time is a true indicator of quality.

With annual revenue of $8.93 billion, J.M. Smucker stands among the larger consumer staples companies, benefiting from strong brand recognition that influences consumer choices. However, its size also means limited opportunities for new retail partnerships, which can restrict growth. To boost sales, the company may need to adjust pricing strategies, introduce new products, or expand internationally.

Over the past three years, J.M. Smucker’s sales have grown at a modest 2.3% compound annual rate, largely due to stagnant sales volumes. We’ll delve deeper into this in the “Volume Growth” section.

This quarter, the company achieved 7% year-over-year revenue growth, with its $2.34 billion in sales topping Wall Street’s expectations by 0.5%.

Looking forward, analysts anticipate a 4% revenue increase over the next year. While this suggests that newer products may drive improved results, the growth rate remains below the industry average.

Volume Growth Analysis

Revenue increases can result from higher prices or greater sales volumes. For consumer staples, volume is especially important since there’s a limit to how much consumers will pay for everyday items—they can always switch to generic alternatives if branded products become too expensive.

J.M. Smucker’s quarterly sales volumes have remained relatively stable over the past two years, which is typical for staple goods as demand tends to be steady.

In the fourth quarter of 2026, sales volumes declined by 2% year-over-year, a further slowdown compared to previous periods, indicating some challenges in driving product movement.

Summary of J.M. Smucker’s Q4 Results

J.M. Smucker’s ability to exceed earnings expectations and deliver a stronger-than-anticipated gross margin stood out this quarter. The stock responded positively, climbing 7.2% to $114.25 immediately after the results were announced.

While the latest quarterly performance was robust, investors should consider long-term fundamentals and valuation when evaluating the stock’s potential.

Discover More Growth Stories

While many investors are focused on high-profile names like Nvidia, a lesser-known semiconductor supplier is quietly dominating a crucial AI component that industry giants rely on.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Marriott International Shares Beating the S&P 500 Index?

特朗普团队拟取消7500美元电动汽车税收抵免,电动汽车股大跌

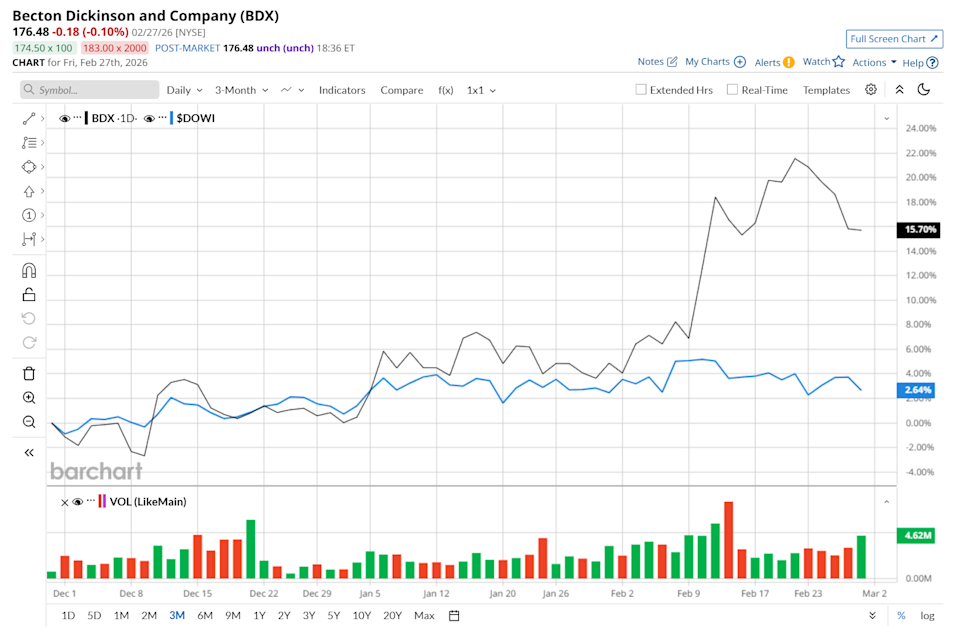

Is Becton, Dickinson and Company Shares Beating the Dow's Performance?

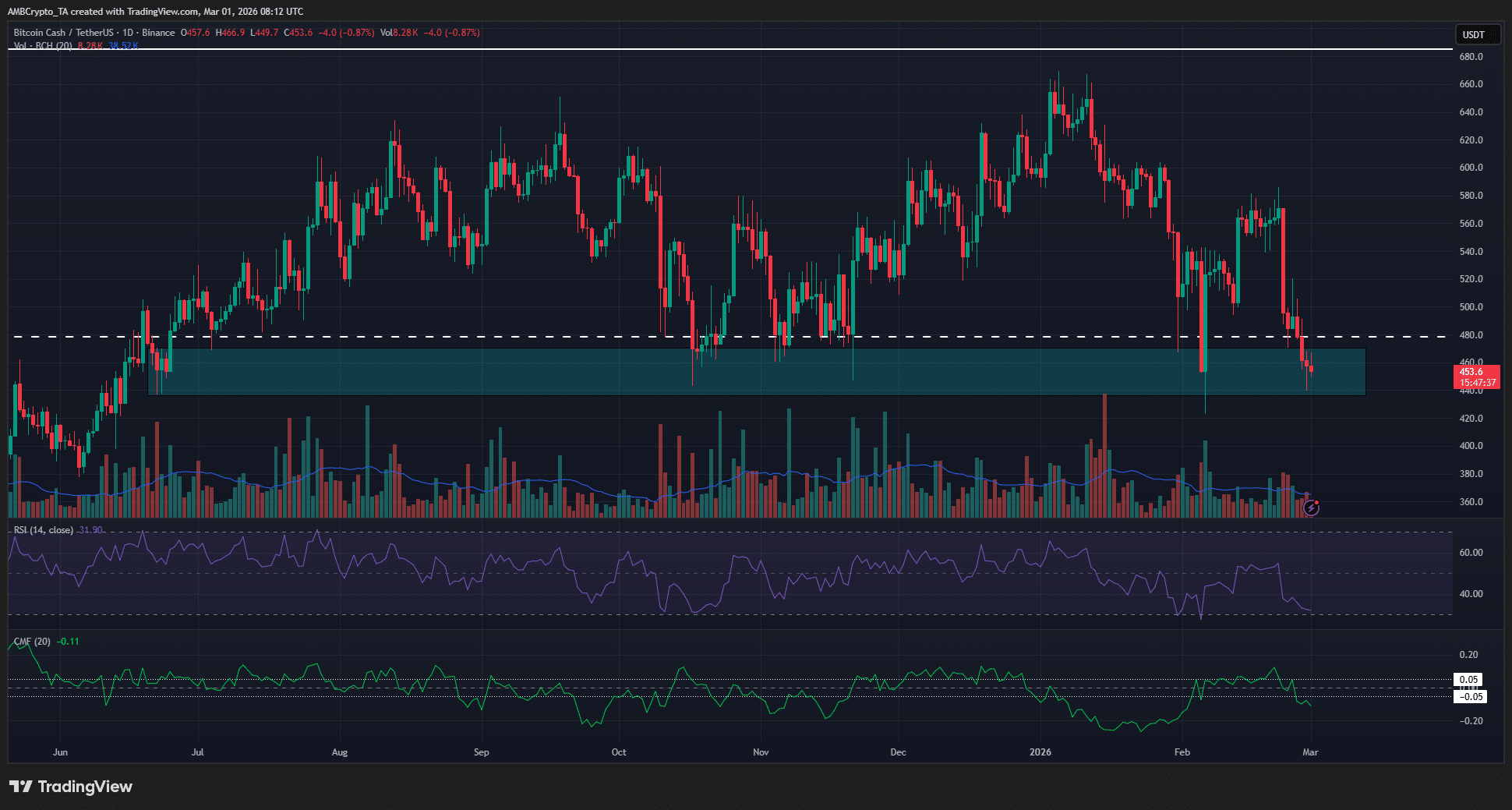

Crypto market’s weekly winners and losers – DOT, NEAR, BCH, PEPE