J. M. Smucker (NYSE:SJM) Surpasses Q4 CY2025 Projections, Shares Surge

J.M. Smucker Surpasses Expectations in Q4 CY2025

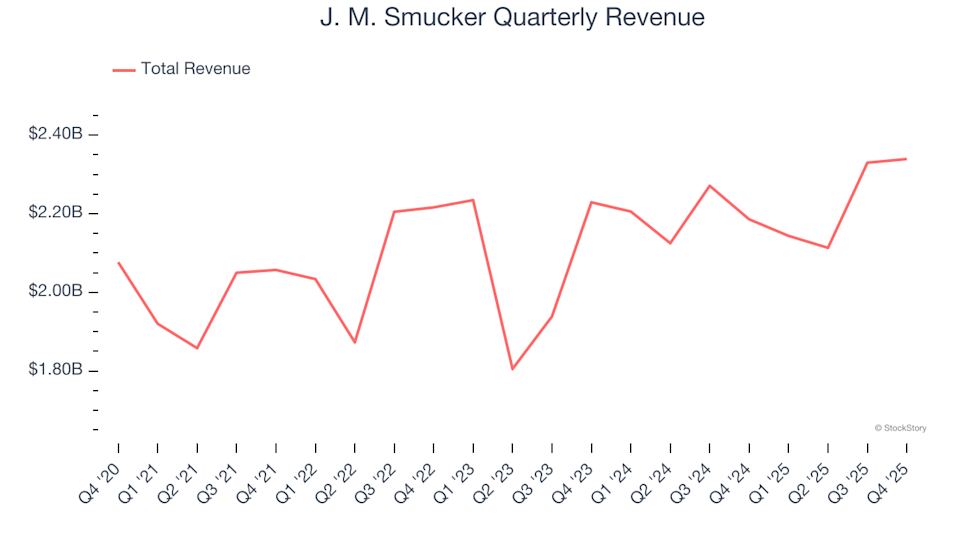

J.M. Smucker (NYSE:SJM), a leader in packaged foods, reported fourth-quarter sales of $2.34 billion, marking a 7% increase compared to the previous year and outperforming Wall Street’s revenue forecasts. The company’s adjusted earnings per share reached $2.38, exceeding analyst predictions by 5.2%.

Highlights from Q4 CY2025

- Revenue: $2.34 billion, beating estimates of $2.33 billion (7% year-over-year growth, 0.5% above expectations)

- Adjusted EPS: $2.38, surpassing forecasts of $2.26 (5.2% above consensus)

- Adjusted EBITDA: $548.4 million, ahead of projections of $499.9 million (23.4% margin, 9.7% beat)

- Management reaffirmed its full-year Adjusted EPS target of $9 at the midpoint

- Operating Margin: -23.4%, an improvement from -27.2% in the same period last year

- Free Cash Flow Margin: 20.8%, up from 6.9% a year ago

- Sales Volumes: Decreased 2% year-over-year (compared to a 5% drop last year)

- Market Cap: $11.37 billion

Mark Smucker, CEO, President, and Board Chair, commented, “Our company continues to achieve strong performance despite a changing market. This quarter, both net sales and adjusted earnings per share exceeded our expectations, demonstrating the strength of our brand portfolio and our disciplined approach to managing costs.”

About J.M. Smucker

J.M. Smucker (NYSE:SJM) is widely recognized for its fruit preserves and spreads. The company’s offerings extend to peanut butter, coffee, and pet food, making it a prominent player in the packaged foods industry.

Examining Revenue Trends

Consistent sales growth is often a sign of a high-quality business. While any company can deliver strong results in a single quarter, sustained growth over time is a true indicator of strength.

With $8.93 billion in revenue over the past year, J.M. Smucker stands among the larger consumer staples companies. Its established brand helps drive customer purchases, but its size also means growth opportunities are limited by the number of major retail partners. To boost sales further, the company may need to adjust pricing strategies, develop new products, or expand internationally.

Over the past three years, J.M. Smucker’s sales have grown at a modest 2.3% compound annual rate, largely due to stagnant sales volumes. We’ll delve deeper into this in the “Volume Growth” section.

This quarter, revenue increased 7% year-over-year, with sales of $2.34 billion topping Wall Street’s estimates by 0.5%.

Looking forward, analysts anticipate a 4% rise in revenue over the next year. While this suggests newer products may drive improved results, the forecast remains below the industry average.

Volume Growth Insights

Sales growth can be attributed to both pricing and volume changes. For consumer staples, volume is crucial since there’s a limit to how much customers will pay for everyday items—they can always opt for generic alternatives if branded products become too expensive.

J.M. Smucker’s sales volumes have remained steady over the past two years, which is typical for staple goods that generally see little fluctuation in demand.

In the fourth quarter of 2026, sales volumes declined by 2% year-over-year, indicating a slowdown and highlighting challenges in moving products.

Key Takeaways from the Quarter

J.M. Smucker’s performance this quarter was notable, with earnings per share and gross margin both exceeding analyst expectations. Following the announcement, shares rose 7.2% to $114.25.

While the latest results were strong, investors should consider long-term fundamentals and valuation before making decisions.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analyst Spots XRP Cup and Handle Formation, Sets Price Target

Will the Resumption of War in Iran Push Brent Crude Oil Past $80 Again?

Crypto : Ransomware attacks jump 50% in 2025, but ransoms decline

Nebius Drops 13%: Capital Expenditure Concerns and Related Market Sell-Off