BeiGene Q4 Revenue Up 33% Year-on-Year, Achieves Annual Profitability; Brukinsa Posts Record High Single-Quarter Sales of 1.1 Billion | Earnings Report Highlights

BeiGene announced its financial results for the fourth quarter and full year of 2025 on February 26, successfully crossing the breakeven point and ending years of “burning cash.”

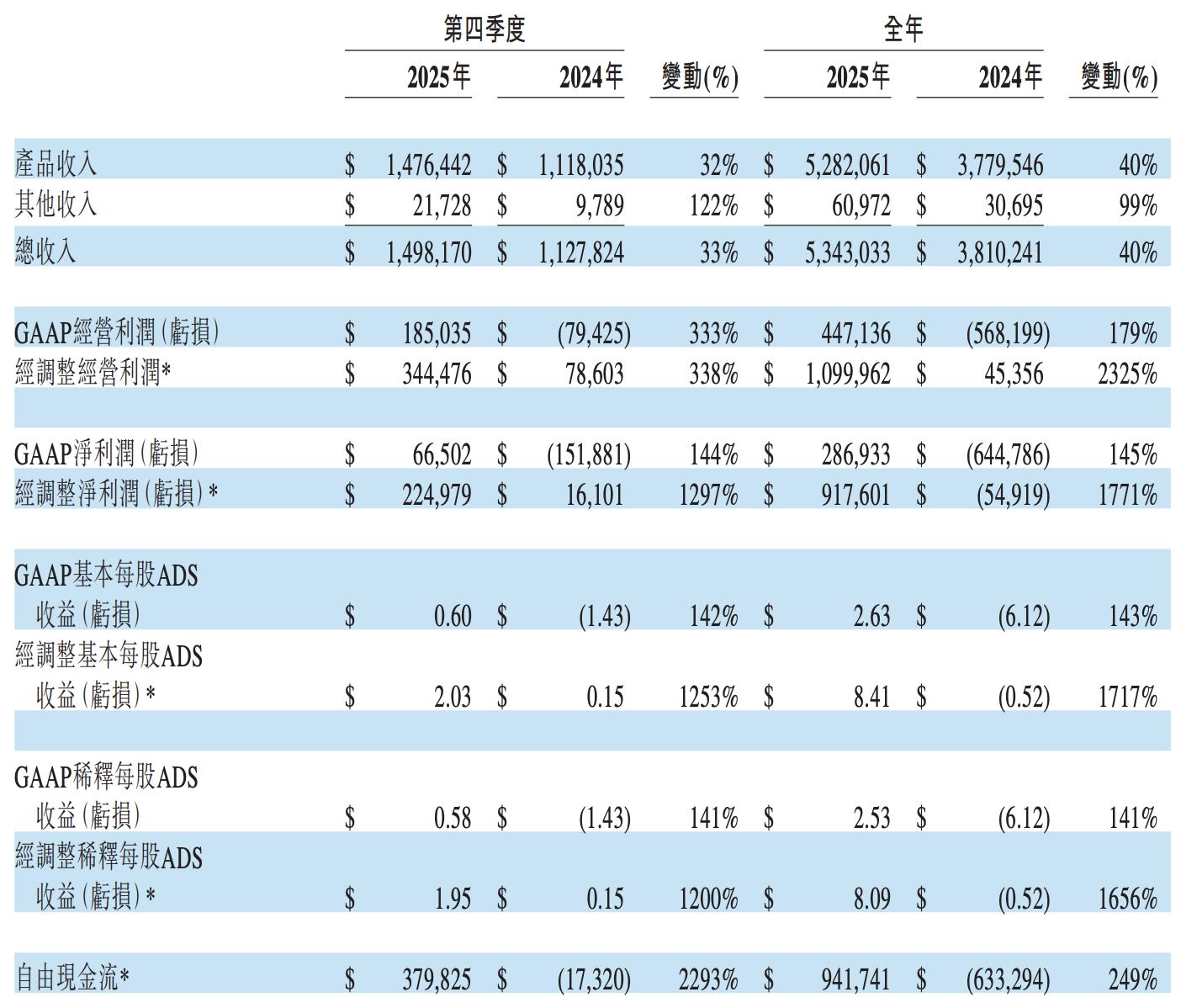

- Total annual revenue reached $5.343 billion, a year-on-year increase of 40%; total revenue for the fourth quarter was $1.5 billion, up 33% year-on-year.

- GAAP net profit for the full year of 2025 was $287 million, a historic turnaround from the net loss of $645 million in 2024, achieving profitability for the first time.

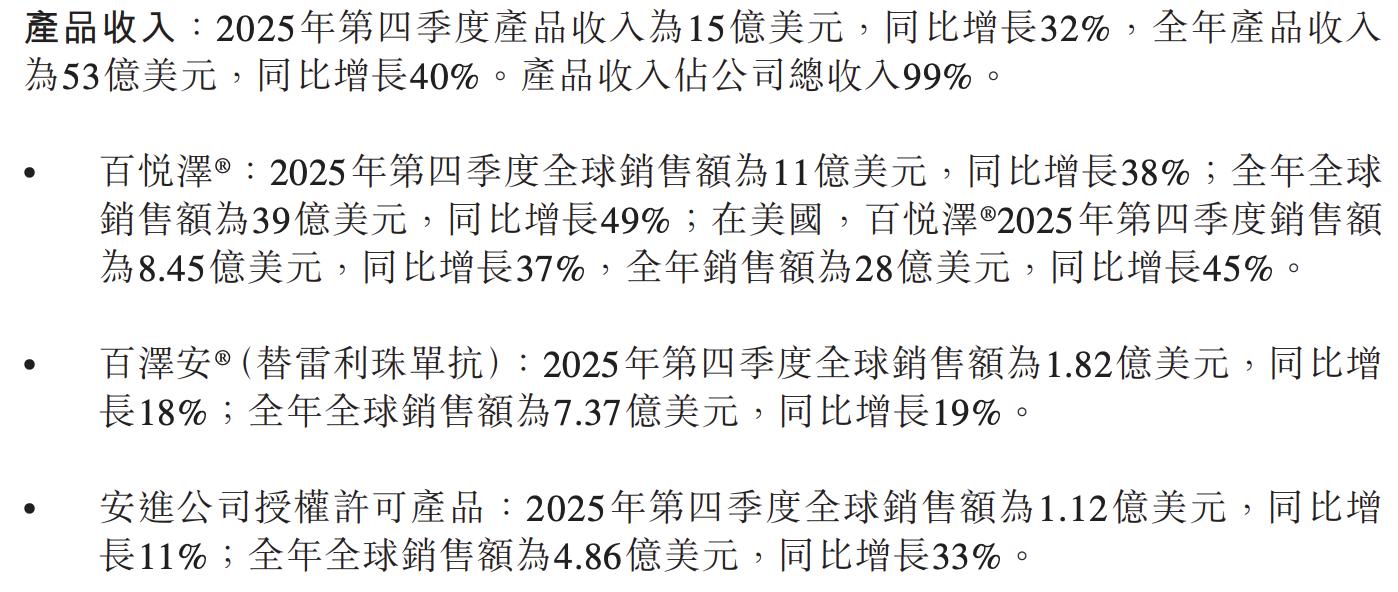

The flagship product Brukinsa (zanubrutinib) continued its rapid expansion, with global annual sales of $3.9 billion, up 49% year-on-year; single-quarter sales in the fourth quarter exceeded $1.1 billion (UTC+8), a 38% year-on-year increase. The US market contributed $2.8 billion for the year, up 45% year-on-year, firmly retaining the top position in the global BTK inhibitor market.

Profit quality surged significantly, with non-GAAP operating profit for the year reaching $1.1 billion, soaring over 23 times from $45.36 million in 2024. Free cash flow turned positive for the year to $942 million, a qualitative leap from negative $633 million in 2024, and the full release of operating leverage marks a new phase in the company’s commercialization.

Looking ahead to 2026, the company has provided total revenue guidance of $6.2 billion to $6.4 billion, representing a year-on-year increase of about 20%, and expects GAAP operating profit of $700 to $800 million. Late-stage blood cancer pipeline products such as sonrotoclax are nearing commercialization, set to inject new growth momentum into the company.

Core Products: Brukinsa dominates the market, tislelizumab expands steadily

Brukinsa has established an absolute dominant position in the BTK inhibitor market, leveraging broad regulatory approvals and robust clinical data barriers. Long-term follow-up data from the SEQUOIA trial (six years) and ALPINE study presented at the ASH Annual Meeting further validated its sustained benefits for treatment-naïve and relapsed/refractory CLL/SLL patients, consolidating its leading advantage.

Tislelizumab achieved global sales of $182 million in the fourth quarter (UTC+8), an 18% increase year-on-year; full-year sales amounted to $737 million, up 19%. Trial data showed statistically significant OS improvement in first-line treatment of HER2-positive gastroesophageal adenocarcinoma in combination with zanidatamab, laying the foundation for submitting a new indication application in 2026.

Amgen-licensed products recorded annual sales of $486 million, up 33% year-on-year.

Pipeline Progress: Sonrotoclax opens the second growth curve

The BCL2 inhibitor sonrotoclax (brunetoclax) was the most significant pipeline breakthrough this quarter: it received the world’s first approval in China, covering R/R MCL and CLL/SLL indications; it also obtained FDA Priority Review designation, and the EMA marketing application has been submitted.

The FDA is expected to make a regulatory decision on R/R MCL in the first half of 2026, potentially making it the company’s next core commercial product.

BTK CDAC candidate BGB-16673 presented Phase I CLL data at ASH, and is expected to submit an accelerated approval application in the second half of 2026.

Multiple early-stage solid tumor pipeline products have initiated first-in-human trials; CDK4 inhibitor BGB-43395 is expected to start a Phase 3 first-line trial in HR+/HER2- metastatic breast cancer in the first half of 2026 (UTC+8), further enriching the pipeline.

Profitability: Gross margin expansion and effective cost control

GAAP gross margin for the fourth quarter and full year of 2025 was 90.4% and 87.3%, respectively, higher than 85.6% and 84.3% in the same period of 2024. Non-GAAP gross margin (excluding depreciation and amortization) was 90.7% and 87.8%, with scale effects and improved production efficiency continuously reflected in profit quality.

Full-year GAAP operating expenses were $4.227 billion, up 12% year-on-year, far lower than the revenue growth of 40%, demonstrating significant operating leverage.

SG&A as a percentage of product revenue decreased from 48% in 2024 to 39%, while R&D expenses grew by 10% year-on-year. It should be noted that annual net profit includes $76 million in impairment of equity investments and $25 million in non-recurring tax items, among other one-off negative factors.

Balance Sheet and Cash Flow: Ample ammunition, greater confidence

By the end of 2025, the company’s cash and cash equivalents reached $4.61 billion, up approximately 75% from $2.64 billion at the end of 2024, significantly strengthening its financial position.

Annual net operating cash inflow was $1.128 billion, in stark contrast to the net outflow of $141 million in 2024, with operating cash flow turning significantly positive for the first time.

On the balance sheet, total assets rose to $8.19 billion, with shareholders’ equity at $4.36 billion.

Due to the Royalty Pharma agreement, an additional $907 million in future royalty liabilities was added. Annual capital expenditure was $186 million, significantly narrowed from $493 million in 2024, with free cash flow quality markedly improved.

2026 Guidance: Targeting $6.4 billion, further profit expansion expected

Full-year 2026 total revenue guidance is $6.2 billion to $6.4 billion, with a midpoint of $6.3 billion, representing an approximate 18% year-on-year increase. GAAP gross margin is expected to remain in the high 80% range, GAAP operating profit between $700 and $800 million, and non-GAAP operating profit between $1.4 and $1.5 billion, all representing substantial expansion compared to 2025.

The company notes that other income (expenses) is expected to be a net expenditure of $25 million to $50 million, mainly related to Royalty Pharma interest amortization.

If 2026 results provide sufficient positive evidence, the reversal of some valuation allowances will bring significant tax benefits, but the timing remains uncertain. The expected diluted outstanding ADS is about 118 million shares, roughly in line with current levels.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ripple CEO Stuns XRP Army With Bombshell Statement for Banks

dogwifhat at $0.20: Reversal or further drop, what’s next for WIF?

"A sharp divide": Wall Street assesses the gains and losses as AI-fueled tech stocks tumble

How to Identify an Effective CEO: A Practical Guide