Tesla’s Challenges in Europe Persist: Is It Wise to Rely on Their Autonomy Commitments?

Tesla Faces Headwinds in Europe

Tesla continues to struggle in the European market, with January marking the 13th consecutive month of declining sales. The company sold just over 8,000 vehicles during the month, representing a 17% decrease compared to the previous year. Factors such as an aging vehicle lineup and fierce competition from Chinese manufacturers, which offer more budget-friendly options, have contributed to the drop in demand. Additionally, CEO Elon Musk’s political activities have negatively impacted Tesla’s reputation in the region.

These challenges are especially notable given that the overall European battery electric vehicle (BEV) market expanded by roughly 14% in January. In contrast, one competitor, which surpassed Tesla as the world’s leading EV seller in 2025, delivered over 18,000 vehicles in Europe last month.

With its main EV business under pressure, Musk is steering Tesla toward becoming a broader technology company, emphasizing artificial intelligence, self-driving technology, and robotics as future growth engines.

But do these long-term ambitions justify holding Tesla stock today? Let’s take a closer look.

Tesla’s Robotaxi Efforts Lag Behind

Tesla launched its initial robotaxi service in Austin in June 2025. The service now operates in both Austin and the California Bay Area, with plans to expand to seven additional cities—Dallas, Houston, Phoenix, Miami, Orlando, Tampa, and Las Vegas—within the first half of the year.

Musk has stated that, pending regulatory approval, fully autonomous Tesla vehicles could be available to about 25% to 50% of the U.S. population by year-end. However, similar promises were made in July 2025, and those targets were not met. Given this track record, skepticism remains about whether these new goals are achievable or simply optimistic projections. For now, the timeline remains uncertain.

Tesla also faces stiff competition from Alphabet’s autonomous driving business, which leads the U.S. robotaxi market and has recently expanded driverless operations to cities such as Dallas, Houston, San Antonio, and Orlando, now covering 10 cities in total.

That company’s vehicles operate at Level 4 autonomy, allowing them to function without human intervention in specific areas. In contrast, Tesla’s vehicles are still classified as Level 2, requiring drivers to remain attentive and ready to take control.

While Tesla has deployed a small number of driverless robotaxis in Austin without human safety operators, its scale is far behind its competitors. Since launch, Tesla’s Austin robotaxis have reportedly been involved in 14 accidents. The company reported nearly 700,000 paid miles driven by the fleet, while its main competitor logs over 450,000 paid rides each week in the U.S. The gap in both technology and operations is significant, and Tesla has considerable ground to cover.

Optimus: Ambitious Goals, Uncertain Timeline

Beyond autonomous vehicles, Musk is also focusing on Tesla’s humanoid robot project, Optimus. The third-generation Optimus is set to be revealed in the first quarter of 2026, with mass production as the target.

Last year, Musk made bold predictions, suggesting that Optimus could eventually bring in more than $10 trillion in revenue over time—a figure he himself admitted sounds “absolutely insane.”

While robotics could become a major market in the future, significant scaling is likely years away. The technology’s commercial viability, cost-effectiveness, and practical applications are still unproven. For now, Optimus remains more of a vision than a revenue driver.

Heavy Spending Amid Core EV Challenges

Tesla’s aggressive capital expenditure plans add further risk. Management expects to spend over $20 billion in 2026, a sharp increase from about $8.5 billion last year and well above the previous high of $11.3 billion in 2024.

This investment will support six major projects, including facilities for a refinery, LFP batteries, the CyberCab, Semi, a new megafactory, and Optimus. Tesla also plans to invest heavily in AI infrastructure to advance self-driving, robotaxi, and robotics initiatives.

While these investments could pay off in the long run, they come at a time when Tesla’s main EV business is slowing. Vehicle deliveries fell for the second straight year in 2025, dropping over 8% after a 1% decline in 2024.

In essence, Tesla is committing significant resources upfront, while meaningful revenue from AI, robotaxis, and robotics remains uncertain and likely years away. This increases short-term financial pressure on the company.

Tesla’s Stock Performance and Valuation

In the past six months, Tesla shares have risen 19%, but this lags behind the broader automotive industry.

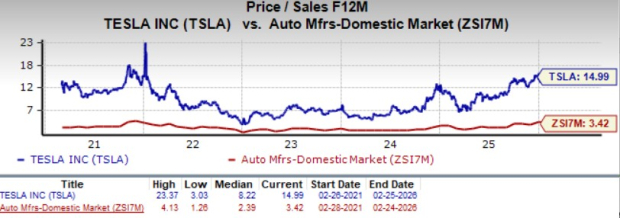

Currently, Tesla trades at a forward price-to-sales ratio of 15, which is much higher than the industry average and its own five-year average. The company’s valuation has often been disconnected from near-term fundamentals, but this does not eliminate the risk of a downturn. Much of the optimism about Tesla’s future in autonomy and AI is already reflected in the stock price. Tesla holds a Value Score of F.

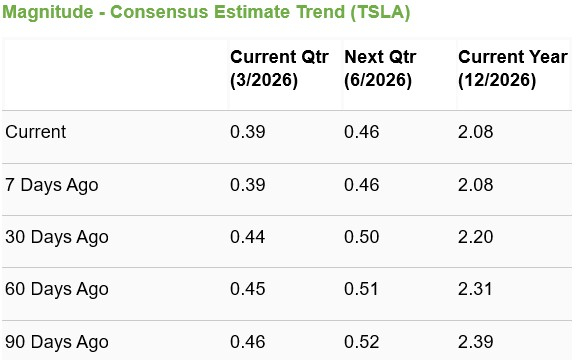

Analyst estimates for Tesla’s earnings per share have trended downward over the past two months.

Conclusion

Tesla’s aspirations in autonomous driving, robotaxis, and robotics are undeniably ambitious. However, the company faces significant execution risks. Tesla trails competitors in driverless technology, has a history of missing robotaxi rollout targets, and Optimus is still far from commercial viability.

Meanwhile, Tesla’s core electric vehicle business is weakening, and capital expenditures are set to surge. Until the company demonstrates substantial progress and results in autonomy and robotics, investing based solely on long-term promises may be premature.

For now, it may be wise for investors to avoid Tesla stock rather than buy or hold it based only on its AI and autonomy ambitions. The company currently holds a Zacks Rank #4 (Sell).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Can digital subscriptions serve as a fresh source of income for ISRG in 2026?

Viking Holdings (VIK) Surpasses Q4 Expectations for Earnings and Revenue

Neuronetics Q4 Results: Is This a Sell-the-News Opportunity or a Chance to Buy the Dip?

Gas prices jump by 30% again after Qatar halts additional output