3 Reasons to Steer Clear of NEO and One Alternative Stock Worth Buying

NeoGenomics: A Closer Look at Recent Performance

Over the past six months, NeoGenomics has experienced remarkable growth, with its stock price surging by 48.3% to reach $9.94. This impressive climb was fueled in part by strong quarterly earnings, prompting investors to consider their next steps regarding the company.

Should you consider adding NeoGenomics to your portfolio, or does it carry more risk than reward?

Why We Believe NeoGenomics May Not Outperform

While we’re pleased to see investors benefit from NeoGenomics’ rally, we remain cautious. Here are three key reasons we see more attractive opportunities elsewhere, along with a stock we prefer.

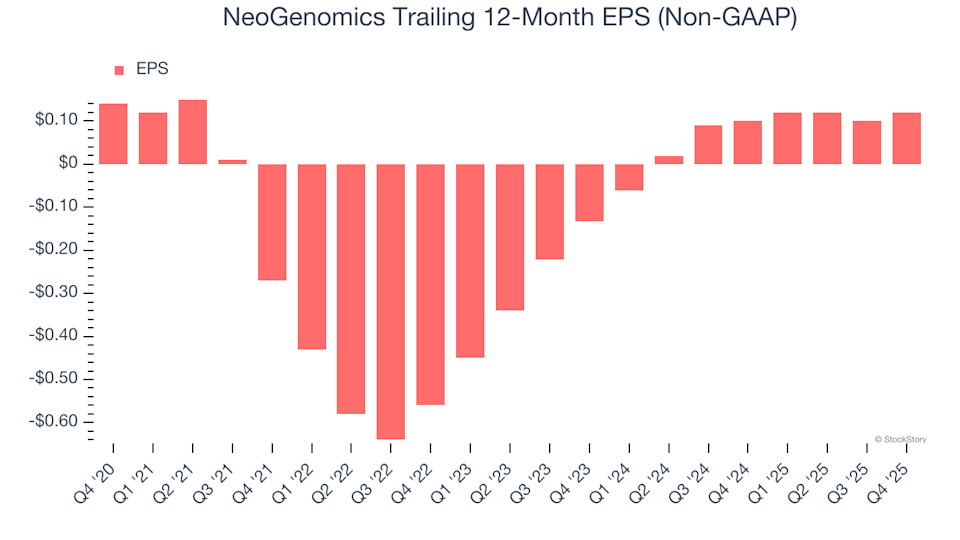

1. Declining Earnings Per Share

Monitoring long-term trends in earnings per share (EPS) helps us assess whether a company’s expansion is translating into profitability.

Unfortunately, NeoGenomics’ EPS has fallen by an average of 3% annually over the past five years, despite revenue increasing by 10.4% each year. This indicates that the company’s growth has not been accompanied by improved profitability for shareholders.

2. Unprofitable Growth Strategies

Growth potential is important, but it’s equally vital to evaluate how efficiently that growth is achieved. Return on invested capital (ROIC) measures how much operating profit a company generates for each dollar of capital raised.

NeoGenomics has posted an average ROIC of negative 10.5% over the last five years, meaning that its expansion efforts have resulted in losses. This performance ranks among the lowest in the healthcare industry.

3. Elevated Debt Poses Financial Risks

While debt can enhance returns, excessive borrowing can threaten a company’s stability. As long-term investors, we prefer to avoid businesses that take on too much debt, as it increases the risk of financial distress.

NeoGenomics currently holds $409.5 million in debt, far surpassing its $159.6 million in cash. Its net-debt-to-EBITDA ratio stands at 6×, based on $43.36 million in EBITDA over the past year, indicating a high level of leverage.

With this amount of debt, further borrowing becomes costly, and a decline in profitability could lead to credit downgrades. Should market conditions deteriorate, NeoGenomics could find itself in a vulnerable position—something we aim to avoid when seeking quality investments.

We remain hopeful that NeoGenomics will strengthen its financial position, but we advise caution until the company either boosts profitability or reduces its debt burden.

Our Verdict

We appreciate companies that contribute to better health outcomes, but at this time, we’re steering clear of NeoGenomics. Following its recent surge, the stock is trading at a forward P/E of 57× (or $9.94 per share). At this valuation, much optimism is already reflected in the price, and we believe more compelling investment options exist. Consider exploring instead.

Alternative Stocks to Consider

Building a successful portfolio means looking forward, not relying on past winners. The risks associated with crowded trades are increasing every day.

Discover the next generation of high-growth companies in our curated list of . These high-quality selections have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known leaders like Nvidia, which soared 1,326% between June 2020 and June 2025, as well as lesser-known companies such as Comfort Systems, which achieved a 782% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is the Invesco RAFI Developed Markets ex-U.S. ETF (PXF) Currently a Top ETF Choice?

Wix's AI Playbook Takes Shape: Strong Growth, $250 Million Investment And Massive Buyback

Esperto trader: in arrivo un’impennata di Bitcoin a 220.000 $, ma prima accadrà questo

Republic Airways Holdings: Fourth Quarter Earnings Overview