IDEX (IEX): Should You Buy, Sell, or Hold After Q4 Results?

IDEX’s Recent Performance: Outpacing the Market

Over the past half year, IDEX has delivered a 24.2% return, surpassing the S&P 500 by 17.7%. The stock now trades at $206.19 per share, prompting investors to consider their next move.

Should you consider adding IDEX to your portfolio, or is it a potential pitfall?

Why We’re Cautious on IDEX

Despite its impressive momentum, we’re choosing to stay on the sidelines for now. Here are three key reasons we’re steering clear of IDEX, along with a stock we prefer instead.

1. Core Business Growth Has Stalled

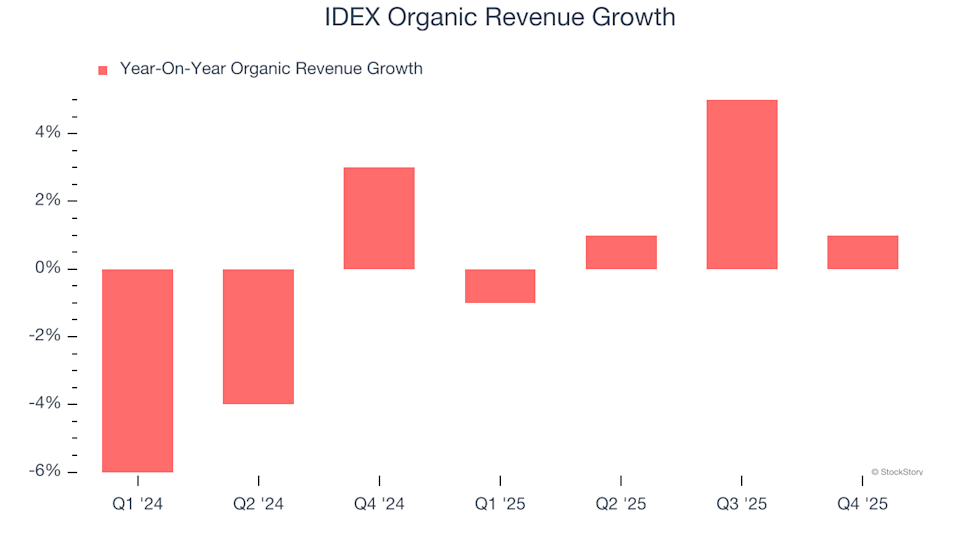

To get a clearer picture of companies in the Gas and Liquid Handling sector, we focus on organic revenue, which strips out the effects of mergers, acquisitions, divestitures, and currency changes. This approach highlights the true performance of IDEX’s main operations.

In the past two years, IDEX has not managed to increase its organic revenue—a sign that its core business may be struggling. This stagnation suggests the company might need to rethink its product offerings, pricing, or sales approach. It also raises the possibility that IDEX will rely more heavily on acquisitions to drive growth, a strategy that can be both costly and disruptive.

2. Earnings Per Share Have Declined

While long-term earnings trends are important, short-term changes in EPS can reveal new developments. Unfortunately, IDEX’s EPS has dropped by an average of 1.7% per year over the last two years, even as revenue increased by 2.8%. This means the company’s profitability per share has decreased, despite higher sales.

IDEX Trailing 12-Month EPS (Non-GAAP)

3. Return on Invested Capital Is Falling

We prefer companies that consistently generate strong returns on invested capital (ROIC), as this often signals a high-quality business. However, the direction of ROIC is just as important as the level. In IDEX’s case, ROIC has been trending downward in recent years. While management has made solid decisions in the past, the declining returns may indicate that profitable growth opportunities are becoming harder to find.

IDEX Trailing 12-Month Return On Invested Capital

Our Verdict

We appreciate companies that make life easier for their customers, but with IDEX, we’re choosing to watch from the sidelines. The stock’s recent outperformance has pushed its valuation to 25.2 times forward earnings (or $206.19 per share), suggesting that a lot of optimism is already reflected in the price. There are more attractive opportunities available. Consider exploring one of Charlie Munger’s favorite companies instead.

Stocks We Prefer Over IDEX

This year’s market rally has been driven by just four stocks, which together account for half of the S&P 500’s total gains. Such concentration can make investors uneasy. While many are crowding into these popular names, savvy investors are seeking out high-quality stocks that are still under the radar—and often available at much lower prices. Take a look at our Top 6 Stocks for this week, a handpicked selection of high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known leaders like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Tecnoglass, a former micro-cap that achieved a 1,754% five-year return. Discover your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold Rises As Middle East Conflict Intensifies

Here's Why You Should Add HEI Stock to Your Portfolio Right Now

XRP’s Moment: Strait Of Hormuz Chaos Could Trigger Ripple’s New Financial Era — Here's How

Turning Point Brands: The Sell-Off After a Beat That Missed the Street