3 Factors That Make CHGG Risky and One Alternative Stock Worth Considering

Chegg’s Challenging Six Months

Chegg has faced a difficult half-year, with its share price plummeting by 52.8% to just $0.65. This sharp decline has left many investors unsettled and reconsidering their strategies.

Should you consider adding Chegg to your portfolio now, or is caution warranted?

Why We Expect Chegg to Lag Behind

Despite its lower valuation, we remain skeptical about Chegg’s prospects. Below are three key reasons we’re not optimistic about CHGG, along with an alternative stock we prefer.

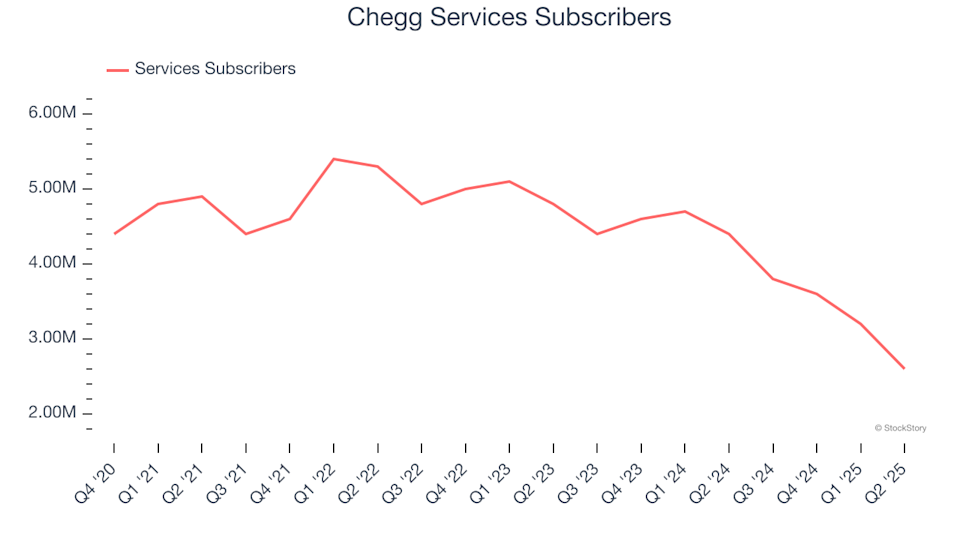

1. Subscriber Losses Signal Product Challenges

Chegg’s business model relies on growing its subscriber base and increasing customer spending. However, over the past two years, the company has seen its number of service subscribers fall by 20.7% annually. This is concerning, especially given the ongoing expansion of internet usage, which should present new opportunities. For Chegg to reignite growth, it will likely need to improve its current offerings or introduce innovative products.

2. Profit Margins Are Shrinking

To gauge a company’s true profitability, investors often look at operating income and EBITDA, which removes one-off and non-cash expenses for a clearer picture. Chegg’s EBITDA margin has dropped by 15 percentage points in recent years. Although the company once boasted strong margins, investors now want to see a return to greater profitability. Over the past twelve months, Chegg’s EBITDA margin stood at 18.2%.

3. Earnings Per Share on the Decline

Tracking long-term changes in earnings per share (EPS) helps reveal whether a company’s growth is sustainable. Unfortunately, Chegg’s EPS has fallen by an average of 71.5% per year over the last three years—outpacing its revenue decline. This suggests that Chegg’s fixed costs have made it difficult to adapt to weaker demand.

Our Verdict

While we support companies that serve everyday consumers, Chegg’s recent performance leaves us unconvinced. The stock now trades at 2.2 times forward EV/EBITDA (or $0.65 per share), which may look attractive at first glance. However, with its underlying issues, the risks appear significant. There are more promising opportunities available. For example, we favor a leading aerospace company with a proven M&A track record.

Top Stocks for Any Market Environment

This year’s market rally has been driven by just four stocks, which together account for half of the S&P 500’s gains. Such concentration can make investors uneasy. While many chase the same popular names, savvy investors are seeking out high-quality stocks that are overlooked and undervalued. Explore our Top 5 Strong Momentum Stocks for this week—a handpicked list of high-quality companies that have delivered a 244% return over the past five years (as of June 30, 2025).

Our selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Kadant, which achieved a 351% five-year return. Discover your next winning investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump SAVE act stalls crypto CLARITY act push

What's Fueling Hyperliquid’s Surge? HYPE Outperforms Top 100 Cryptos In Latest Rally