BRK.B Shares Are Below Their 52-Week Peak: How Should Investors Respond?

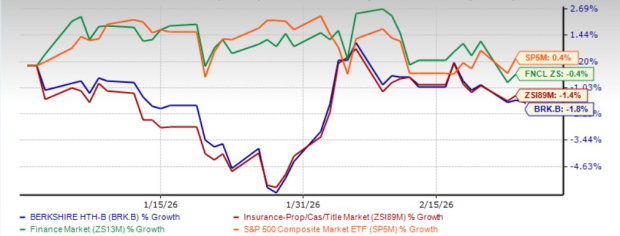

Berkshire Hathaway Stock Performance Overview

Berkshire Hathaway Inc. (BRK.B) ended Wednesday at $493.99, which is 8.9% below its highest price over the past year of $542.07.

So far this year, BRK.B shares have declined by 1.8%. In comparison, the property and casualty insurance industry is down 1.4%, and the finance sector has slipped 0.4%. Meanwhile, the Zacks S&P 500 composite has seen a modest gain of 0.4% during the same period.

Berkshire Hathaway operates as a diversified conglomerate, with over 90 subsidiaries spanning various industries, which helps the company maintain stability through different economic environments.

Comparing BRK.B to Peers and the Market

Among its competitors, Chubb Limited (CB) has advanced 7.2% year to date, while The Progressive Corporation (PGR) has dropped 10.2% over the same timeframe.

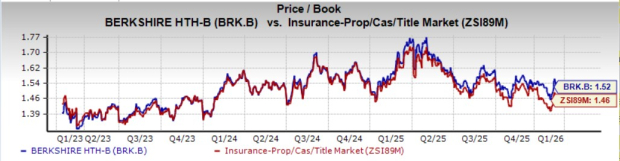

Valuation: Is BRK.B Overpriced?

Currently, Berkshire Hathaway trades at a price-to-book ratio of 1.52, which is above the industry average of 1.46, though slightly below its three-year median of 1.53. This suggests the stock is valued at a premium compared to its peers.

Berkshire Hathaway has received a Value Score of D. While it is less expensive than PGR, it remains pricier than CB.

Key Strengths of Berkshire Hathaway

The insurance segment is central to Berkshire Hathaway’s operations, contributing about 25% of total revenue and serving as a major driver of long-term value. The company’s insurance arm benefits from disciplined underwriting, broad market access, and consistent profitability, regardless of economic conditions. A significant advantage is the large underwriting float, which Warren Buffett has used as a low-cost funding source for investments across the company.

Berkshire Hathaway Energy (BHE), the regulated utility division, provides reliable cash flow and is expanding its renewable energy investments, positioning itself to benefit from trends like electrification and sustainability.

Burlington Northern Santa Fe (BNSF), one of the largest freight rail networks in the U.S., remains a valuable asset despite current challenges from a less favorable freight mix and reduced fuel surcharge revenue. BNSF continues to play a crucial role in U.S. transportation infrastructure.

The Manufacturing, Service, and Retail segment adds further diversification and growth opportunities. This segment could see significant gains if economic conditions and consumer demand improve, potentially boosting volumes and profit margins.

Financially, Berkshire Hathaway is highly conservative, holding over $100 billion in cash and equivalents, with nearly 90% in short-term U.S. Treasuries and government-backed securities. This strong liquidity allows the company to pursue acquisitions and generate steady income.

Recently, Berkshire has restructured its equity portfolio, selling its stake in BYD, reducing positions in Apple and Bank of America, and increasing investments in Japanese trading companies like Mitsubishi and Mitsui. The company also initiated a position in Alphabet. Under CEO Greg Abel, Berkshire plans to fully exit its Kraft Heinz investment, taking a $3.76 billion write-down in Q2 2025 as Kraft Heinz explores strategic options.

Overall, Berkshire Hathaway’s growing insurance float continues to provide a stable source of low-cost capital, reinforcing its financial strength and supporting long-term shareholder value growth.

Return on Capital Analysis

Over the past 12 months, Berkshire Hathaway’s return on equity (ROE) was 7.3%, which trails the industry average of 8%. However, the company’s ROE has shown steady improvement. Similarly, return on invested capital (ROIC) has increased annually since 2020, reflecting better use of capital to generate profits. Still, the latest ROIC of 5.9% is below the industry average of 6.2%.

Analyst Outlook

According to the Zacks Consensus Estimate, Berkshire Hathaway’s revenue is expected to grow by 4.7% year over year in 2026, while earnings are projected to decline by 0.5%. The company has been assigned a Growth Score of F.

There has been no change in the consensus earnings estimate for 2026 over the past month. In contrast, CB’s estimate has decreased by 0.6%, while PGR’s has increased by 0.4% during the same period.

Final Thoughts on BRK.B Shares

Berkshire Hathaway has long been a staple in many investment portfolios, delivering consistent value under Warren Buffett’s leadership for nearly six decades. The company is entering a new era, with Greg Abel set to become CEO on January 1, 2026, while Buffett will remain as executive chairman.

Despite its strong legacy, investors should be cautious. The stock is currently trading at a premium, returns on capital are moderate, and short-term earnings face pressure. Berkshire Hathaway holds a VGM Score of F and is currently rated as a Zacks Rank #4 (Sell), suggesting that it may be wise to avoid the stock for now.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Fed's Waller: Spike in gas prices unlikely to cause sustained inflation

Fed: Gradual cuts and steady inflation path – Danske Bank

Stablecoin Market Cap Hits Record $312B as Liquidity Floods Back into DeFi

3 Undervalued Stocks with Uncertain Financial Foundations