Is Investing in Netflix Shares a Wise Choice as Content Expenses Climb?

Netflix’s 2025 Results and Strategic Outlook

Netflix (NFLX) posted impressive results for the fourth quarter of 2025, but its future path involves a conscious decision to ramp up spending in pursuit of greater growth. The effectiveness of this approach will depend on how successfully Netflix implements its content-focused plan for 2026, which is already challenging investor patience.

During Q4, Netflix reported $12.05 billion in revenue, marking an 18% increase year-over-year. Operating income climbed 30% to $2.96 billion, and the operating margin improved to 24.5%. The company closed out the year with 325 million paying subscribers and generated $9.5 billion in free cash flow, exceeding its forecast of $9 billion. Total revenue for 2025 reached $45 billion, with an operating margin of 29.5%, up from 26.7% in 2024.

Looking ahead to 2026, Netflix anticipates revenue between $50.7 billion and $51.7 billion, representing 12% to 14% growth and a projected operating margin of 31.5%. This margin includes approximately $275 million in expenses related to its pending acquisition of Warner Bros. Studios and HBO, as well as about 10% growth in content amortization compared to the previous year. To conserve funds for the acquisition, Netflix has temporarily suspended its share repurchase program, after buying back $2.1 billion in shares during Q4.

The company plans to concentrate content spending in the first half of 2026, which will temporarily impact operating income before a recovery in the latter half of the year. The upcoming lineup reflects this investment: March 2026 will feature Peaky Blinders: The Immortal Man, the second season of live-action One Piece, Virgin River Season 7, MLB Opening Night live coverage, and a BTS comeback special. This diverse mix of high-profile drama, live sports, and global entertainment is intended to keep subscribers engaged.

Advertising revenue, which grew 2.5 times in 2025, is expected to nearly double again to around $3 billion in 2026. While this segment is expanding, it remains a relatively small part of Netflix’s overall revenue. Free cash flow guidance for 2026 is approximately $6 billion, a decrease from 2025’s $9.5 billion, reflecting increased investment activity.

For investors, Netflix offers strong revenue growth and a robust content pipeline, but faces rising costs, acquisition-related uncertainties, and a reduced free cash flow outlook that merits close attention moving forward.

Comparing Content Investment: Amazon and Disney

Netflix is not the only company balancing content spending and profitability. Amazon (AMZN), through Prime Video, continues to invest heavily in original programming and live sports, including its NFL Thursday Night Football deal, as part of a broader strategy to boost subscriptions and advertising. In contrast, Disney (DIS) has been actively reducing content expenses to achieve sustainable streaming profits. While Amazon focuses on expanding its content library to enhance the value of Prime, Disney relies on its established franchises and cost management, highlighting distinct approaches to the same challenge faced by Netflix.

Netflix’s Stock Performance, Valuation, and Analyst Estimates

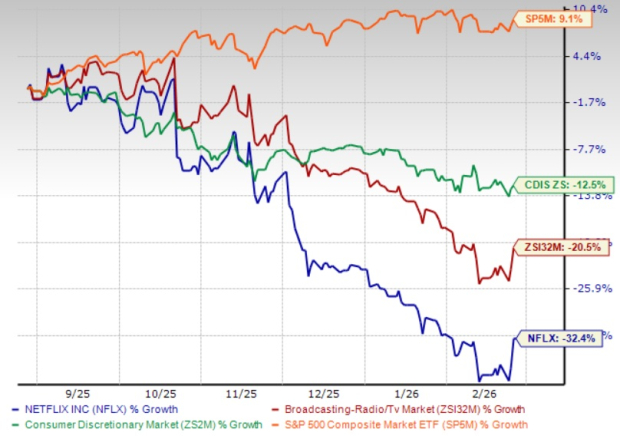

Over the past six months, Netflix shares have dropped 32.4%, compared to a 20.5% decline for the Zacks Broadcast Radio and Television industry.

Six-Month Price Trend for NFLX

Source: Zacks Investment Research

From a valuation perspective, Netflix is trading at a forward 12-month price-to-sales ratio of 6.7, higher than the industry average of 4.04. NFLX holds a Value Score of C.

NFLX Valuation Overview

Source: Zacks Investment Research

Analysts at Zacks estimate Netflix’s 2026 revenue at $51.91 billion, implying 13.3% growth year-over-year. Projected earnings for 2026 are $3.12 per share, a 23.23% increase from the prior year.

Price and Consensus for Netflix, Inc.

For more details, see the Netflix, Inc. price-consensus-chart and Netflix, Inc. Quote.

Currently, NFLX stock has a Zacks Rank #3 (Hold). You can view the full list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Top 10 Stocks for 2026

Act quickly to access Zacks’ top 10 stock picks for 2026, selected by Director of Research Sheraz Mian. This portfolio has delivered remarkable and consistent results.

Since its launch in 2012 through November 2025, the Zacks Top 10 Stocks have achieved gains of +2,530.8%, far outpacing the S&P 500’s +570.3%.

Sheraz reviewed 4,400 companies covered by the Zacks Rank and chose the best 10 for 2026. You can still be among the first to discover these newly released stocks with significant growth potential.

See New Top 10 Stocks >>

Interested in the latest stock recommendations from Zacks Investment Research? Download the 7 Best Stocks for the Next 30 Days for free: Click to get this free report

- Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin jumps 5% before Trump Iran speech

Netflix - This chart is just wonderful!

Top Research Reports for Broadcom, AT&T & Vertex Pharmaceuticals

Rocket Lab's Stock Tumbles Despite 36% Revenue Surge Ranks 112th in $1.22B Trading Volume