Should you purchase, retain, or offload Target shares ahead of the fourth quarter earnings report?

Target Corporation Approaches Q4 2025 Earnings: What Should Investors Do?

With Target Corporation (TGT) set to announce its fourth-quarter fiscal 2025 results on March 3 before the opening bell, investors are weighing whether now is the right time to buy shares or maintain their current holdings.

Target has established itself as a major player in the retail sector, thanks to its broad business approach and robust omnichannel presence. As the earnings date nears, it’s important to assess the main factors that could impact Target’s performance and determine if the stock presents a compelling opportunity ahead of its report.

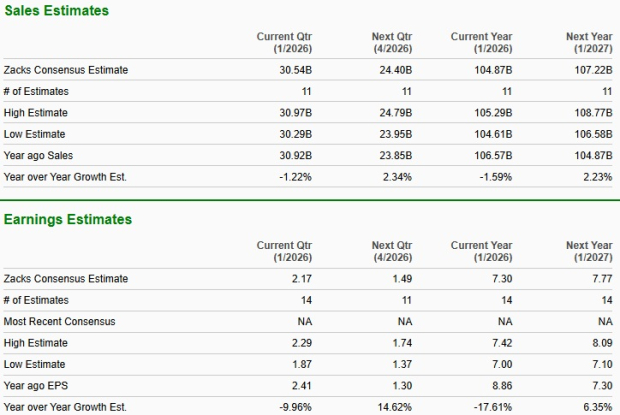

Analysts currently forecast Target’s Q4 revenue at $30.54 billion, which would represent a 1.2% decrease compared to the same period last year. The consensus estimate for quarterly earnings per share has edged up by one cent over the past month to $2.17, but this still marks a 10% drop from the previous year’s quarter. Over the last four quarters, Target has averaged a negative earnings surprise of 3.4%. However, in the most recent quarter, the company’s earnings surpassed expectations by 1.1%.

Image Source: Zacks Investment Research

Q4 Earnings Outlook: Insights from the Zacks Model

As the earnings announcement approaches, investors are eager to know whether Target will exceed or fall short of expectations. According to the Zacks model, there is no clear indication that Target will deliver an earnings beat this quarter. Typically, a positive Earnings ESP combined with a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) increases the likelihood of an earnings surprise. However, Target currently holds a Zacks Rank #2 but has an Earnings ESP of -2.24%, which does not support a strong case for an earnings beat. Investors can use the Earnings ESP Filter to identify stocks with the best potential before results are released.

Target’s Price, Consensus, and EPS Surprise Trends

For more details, see the Target price-consensus-eps-surprise chart and the latest Target Corporation quote.

Key Drivers and Challenges for Target’s Q4 Results

Despite a tough retail environment, Target’s integrated business model has likely supported its Q4 performance. The company’s unique brand portfolio and strong reputation help it stand out, especially during the critical holiday season. Target’s focus on trend-driven and design-focused merchandise likely kept its core customers engaged.

- Initiatives such as the transformation of Hardlines into Fun 101, renewed focus on Home and Baby categories, and a faster pace of new product launches likely boosted holiday traffic.

- Target’s omnichannel services, including same-day options like Drive Up and Target Circle 360, as well as marketplace expansion through Target Plus and digital advertising via Roundel, have likely contributed positively.

- Investments in artificial intelligence for merchandising, better inventory management, and fulfillment improvements aimed to increase stock availability, personalization, and speed.

- Enhanced inventory discipline and reduced shrinkage may have helped maintain operational efficiency and protect margins during a highly competitive season.

However, ongoing challenges such as tariffs and cautious consumer spending—especially in non-essential categories—may have limited growth. Softer store traffic, smaller basket sizes, and aggressive promotions across the industry likely weighed on sales productivity. Increased markdowns and pricing competition are expected to have pressured margins, making it difficult for Target’s strategies to fully counteract weaker demand.

Projections for the quarter include a 2.2% drop in transaction count and a 0.6% decrease in average transaction value, leading to an anticipated 2.8% decline in comparable sales.

Evaluating Target’s Valuation

Target’s shares are currently trading at a notable discount compared to the broader Retail - Discount Stores industry. With a forward 12-month price-to-earnings (P/E) ratio of 14.92, Target’s valuation is well below the industry average of 33.48, suggesting the stock may be undervalued at present.

Image Source: Zacks Investment Research

When compared to other major retailers, Target’s valuation appears even more attractive. Costco (COST) trades at a forward P/E of 47.15, Walmart (WMT) at 43.09, and Ross Stores (ROST) at 28.09—all significantly higher than Target’s multiple.

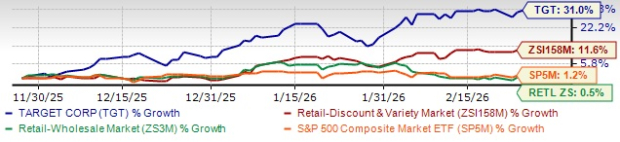

Stock Performance: Target vs. Industry Peers

In the last three months, Target’s share price has surged 31%, outpacing the industry’s 11.6% gain. Over the same period, the Retail-Wholesale sector and the S&P 500 have risen by just 0.5% and 1.2%, respectively.

Image Source: Zacks Investment Research

Target has also outperformed key competitors: Walmart shares are up 15.5%, Ross Stores have climbed 13.7%, and Costco has gained 9.7% during the same timeframe.

Image Source: Zacks Investment Research

Is Target a Buy Before Q4 Earnings?

Target enters its Q4 earnings release with notable strengths, including a diverse product lineup, expanding digital capabilities, and operational enhancements. However, ongoing pressures from cautious consumer spending, intense promotions, and margin challenges could temper results.

Given its relatively low valuation and recent momentum compared to peers, Target may be an appealing choice for investors with a long-term perspective. Existing shareholders might consider holding their positions to benefit from potential future growth and continued strategic progress.

Discover Zacks’ Top 10 Stocks for 2026

There’s still time to access Zacks’ handpicked list of the top 10 stocks for 2026, curated by Director of Research Sheraz Mian. This portfolio has delivered remarkable and consistent returns.

From its inception in 2012 through November 2025, the Zacks Top 10 Stocks soared by +2,530.8%, far outpacing the S&P 500’s +570.3% gain.

Sheraz has carefully selected the best 10 stocks from over 4,400 companies covered by the Zacks Rank for 2026. Be among the first to see these high-potential picks.

See the New Top 10 Stocks >>

Additional Resources and Free Reports

Looking for more investment ideas? Download Zacks’ 7 Best Stocks for the Next 30 Days for free: Get the free report here.

- Target Corporation (TGT): Free Stock Analysis Report

- Walmart Inc. (WMT): Free Stock Analysis Report

- Costco Wholesale Corporation (COST): Free Stock Analysis Report

- Ross Stores, Inc. (ROST): Free Stock Analysis Report

For more insights and the latest research, visit Zacks Investment Research.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Meta Experiments with AI Shopping Research Tool to Compete with ChatGPT and Gemini

Core Scientific's Colocation Expansion: An Analytical Perspective on the Strategic Shift

Dow Jones futures fall as investors turn more cautious