Ross Stores Shares Gain Traction Ahead of Q4 Earnings: Could Results Surpass Expectations?

Ross Stores Set to Announce Q4 Fiscal 2025 Results

Ross Stores, Inc. (ROST) is expected to reveal both revenue and earnings growth for the fourth quarter of fiscal 2025, with results scheduled for release after the market closes on March 3. Analysts are forecasting quarterly sales of $6.37 billion, which would represent a 7.8% increase compared to the same period last year.

The consensus estimate for earnings per share stands at $1.87, reflecting a 4.5% improvement from the prior year’s $1.79. Notably, this estimate has remained steady over the past month.

Recent Earnings Performance

Over the past four quarters, Ross Stores has exceeded earnings expectations by an average of 6.7%. In the most recent quarter, the company delivered a 12.9% earnings surprise.

Key Drivers for Ross Stores’ Q4 Performance

Ross Stores’ anticipated fourth-quarter results are likely to be driven by strong performance across its product lines and positive customer response at both of its retail banners. The company’s focus on offering value deals continues to attract budget-conscious shoppers, especially as consumers remain cautious with discretionary spending. Ongoing store expansion efforts are also expected to contribute to revenue growth.

Ross’s off-price retail strategy appeals to shoppers seeking branded merchandise at lower prices. Additionally, its micro-merchandising approach, which tailors inventory to local preferences, helps optimize product selection and support profit margins. These strategies are expected to boost store traffic, comparable sales, and overall profitability.

During the previous earnings call, management acknowledged ongoing economic challenges but noted that sales strength was broad-based across regions and income groups, with consistent engagement from its core customer base.

For the fourth quarter, Ross Stores projects comparable sales growth of 3-4% and total sales growth of 6-7% year over year. Operating margin is expected to range between 11.5% and 11.8%. According to our estimates, comparable sales are likely to rise by 3.1% for the quarter.

Despite these positives, the company remains cautious due to persistent macroeconomic and geopolitical uncertainties, as well as ongoing inflation, which continue to impact consumer spending on essentials. Tariffs and changing trade policies, particularly those affecting goods sourced from China, have also added to cost pressures.

Will Ross Stores Beat Earnings Expectations?

Our analysis suggests that Ross Stores is well-positioned to surpass earnings estimates this quarter. The company currently holds an Earnings ESP (Expected Surprise Prediction) of +4.39% and a Zacks Rank #2 (Buy), a combination that historically increases the likelihood of an earnings beat. Investors can use the Earnings ESP Filter to identify similar opportunities.

Valuation and Stock Performance

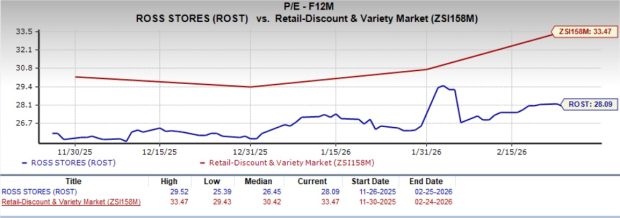

Ross Stores is currently trading at a forward 12-month price-to-earnings ratio of 28.09, which is below the Retail-Discount Stores industry average of 33.47.

Recent Stock Price Trends

Source: Zacks Investment Research

In the past three months, shares of Ross Stores have climbed 13.4%, outpacing the industry’s 11.4% gain.

Valuation Overview

Source: Zacks Investment Research

Other Stocks Poised for an Earnings Beat

According to our model, the following companies also have favorable setups for an earnings surprise this season:

- Dollar General Corporation (DG): Earnings ESP of +7.64% and Zacks Rank #2. The consensus estimate for Q4 fiscal 2025 earnings is $1.58 per share, a 6% decrease year over year. Revenue is projected at $10.75 billion, up 4.4% from the prior year. Dollar General has delivered an average earnings surprise of 22.9% over the last four quarters. See the full list of Zacks #1 Rank stocks here.

- Chewy, Inc. (CHWY): Earnings ESP of +0.36% and Zacks Rank #3. Expected Q4 revenue is $3.26 billion, a 0.3% increase from the previous year. The consensus for Q4 earnings is 28 cents per share, unchanged year over year. Chewy’s average earnings surprise over the past four quarters is 10.7%.

- Costco Wholesale Corporation (COST): Earnings ESP of +0.87% and Zacks Rank #3. Q2 fiscal 2026 revenue is estimated at $69.22 billion, up 8.6% from the year-ago period. The consensus for Q2 earnings is $4.53 per share, representing 12.7% growth. Costco’s average earnings surprise over the last four quarters is 0.5%.

Discover Zacks’ Top 10 Stocks for 2026

There’s still time to access Zacks’ Top 10 Stocks for 2026, a portfolio curated by Director of Research Sheraz Mian. Since its inception in 2012 through November 2025, this portfolio has delivered a remarkable gain of +2,530.8%, far surpassing the S&P 500’s +570.3% return.

Sheraz has carefully selected the top 10 stocks out of 4,400 covered by the Zacks Rank for 2026. Be among the first to see these high-potential picks.

See the New Top 10 Stocks >>

Get More Insights and Reports

Looking for more recommendations? Download the 7 Best Stocks for the Next 30 Days from Zacks Investment Research. Click here for your free report.

- Dollar General Corporation (DG): Free Stock Analysis Report

- Costco Wholesale Corporation (COST): Free Stock Analysis Report

- Ross Stores, Inc. (ROST): Free Stock Analysis Report

- Chewy (CHWY): Free Stock Analysis Report

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analyst Spots XRP Cup and Handle Formation, Sets Price Target

Will the Resumption of War in Iran Push Brent Crude Oil Past $80 Again?

Crypto : Ransomware attacks jump 50% in 2025, but ransoms decline

Nebius Drops 13%: Capital Expenditure Concerns and Related Market Sell-Off