MasTec (NYSE:MTZ) Delivers Strong Q4 CY2025 Numbers

Infrastructure construction company MasTec (NYSE:MTZ) announced

MasTec (MTZ) Q4 CY2025 Highlights:

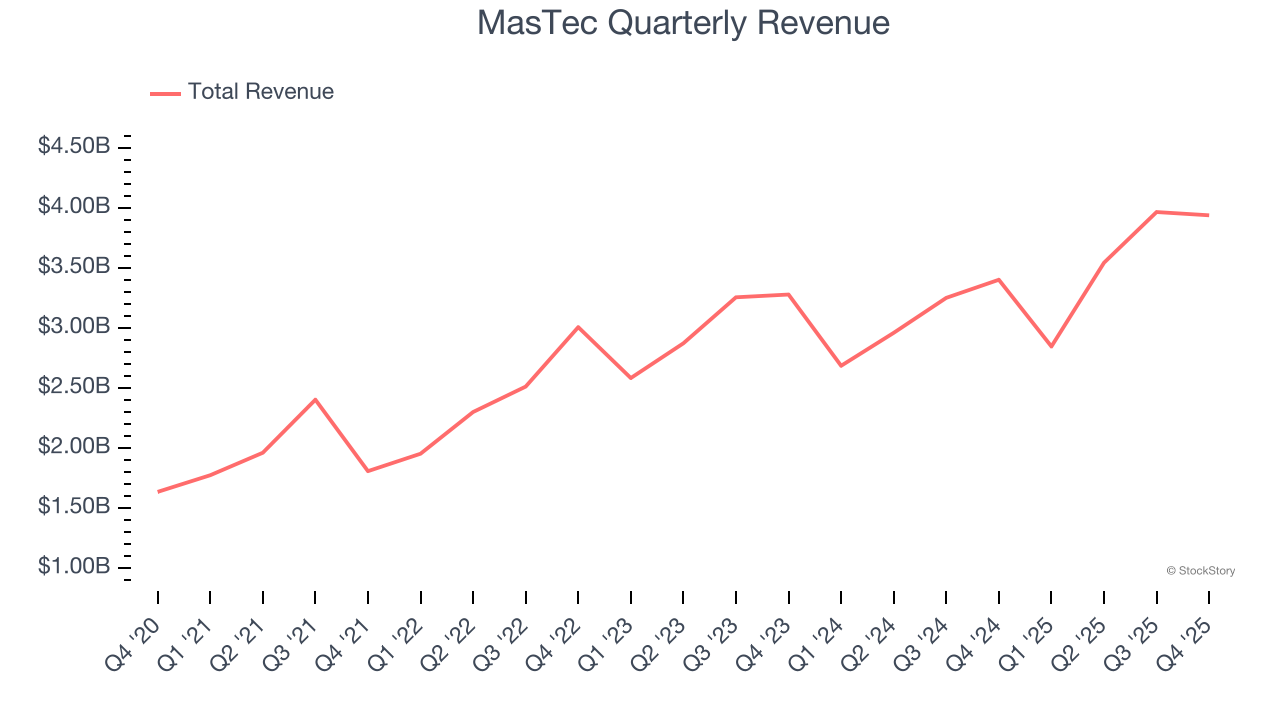

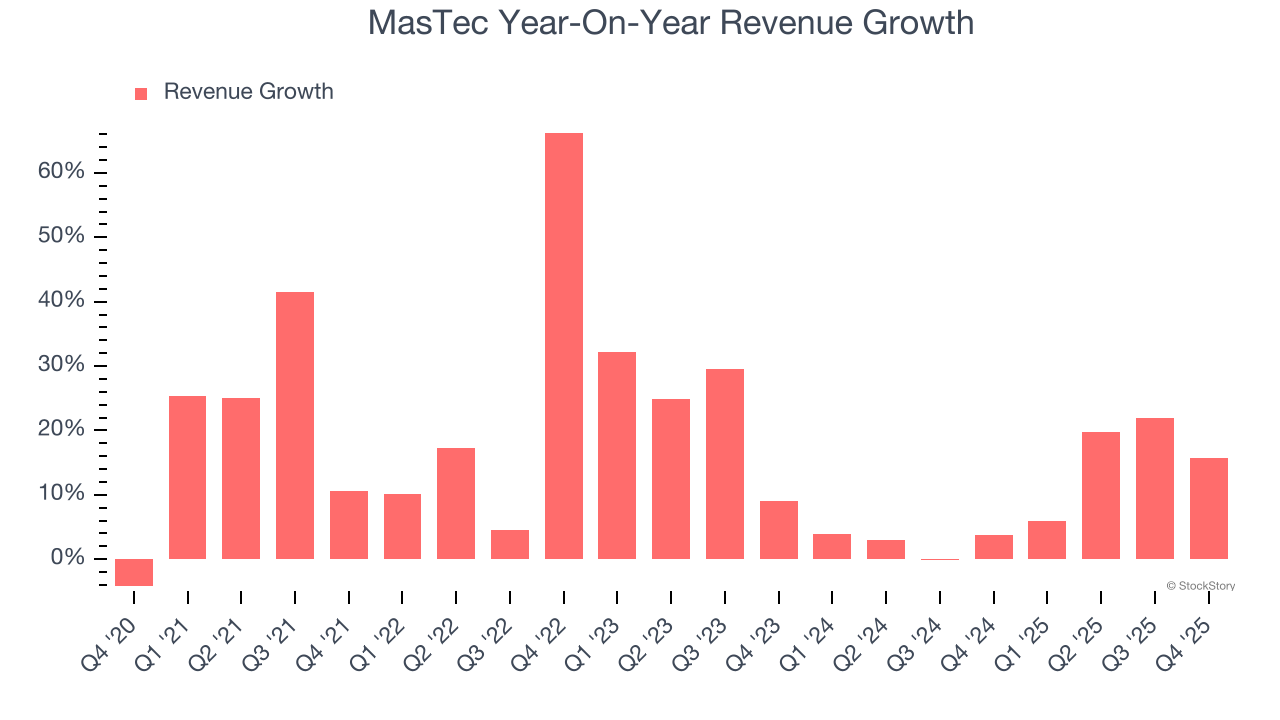

- Revenue: $3.94 billion vs analyst estimates of $3.72 billion (15.8% year-on-year growth, 5.9% beat)

- Adjusted EPS: $2.07 vs analyst estimates of $1.95 (6.4% beat)

- Adjusted EBITDA: $338.2 million vs analyst estimates of $325.5 million (8.6% margin, 3.9% beat)

- Revenue Guidance for Q1 CY2026 is $3.48 billion at the midpoint, above analyst estimates of $3.2 billion

- Adjusted EPS guidance for the upcoming financial year 2026 is $8.40 at the midpoint, beating analyst estimates by 3%

- EBITDA guidance for the upcoming financial year 2026 is $1.45 billion at the midpoint, above analyst estimates of $1.39 billion

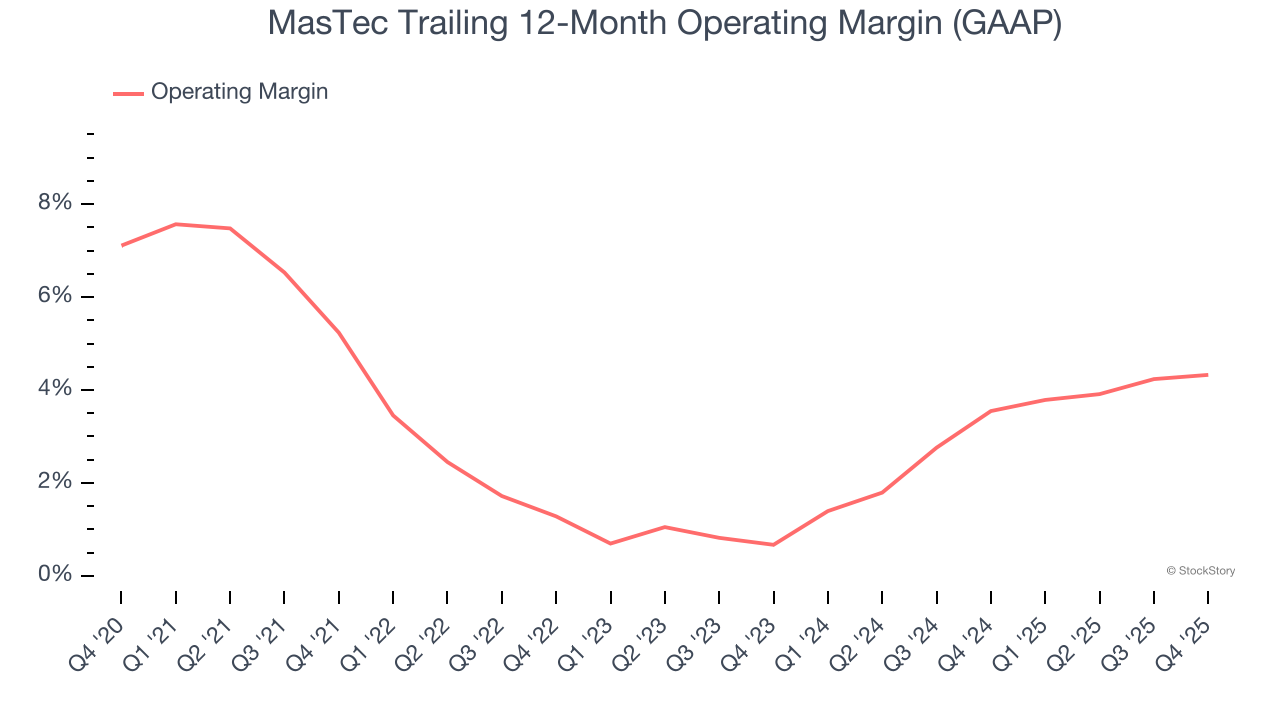

- Operating Margin: 4.4%, in line with the same quarter last year

- Free Cash Flow Margin: 9.5%, down from 12.4% in the same quarter last year

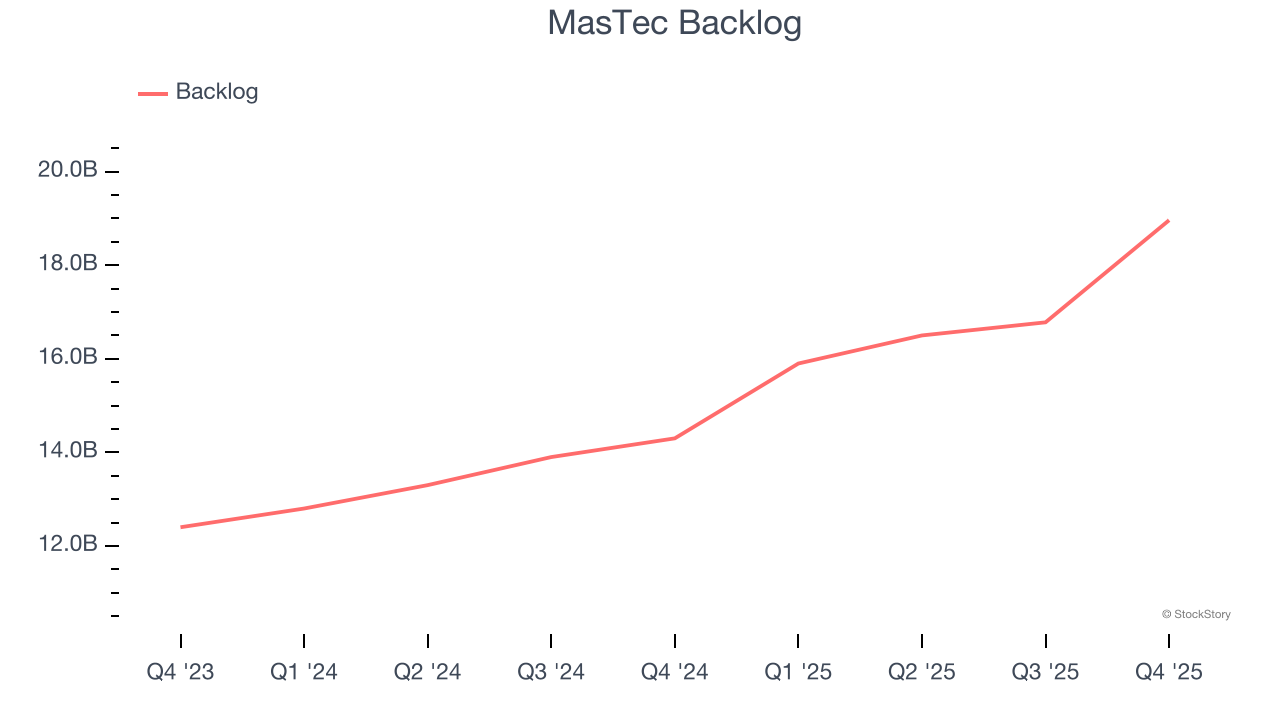

- Backlog: $18.96 billion at quarter end, up 32.6% year on year

- Market Capitalization: $22.15 billion

Company Overview

Involved in the 1996 Olympic Games MasTec (NYSE:MTZ) is an infrastructure construction company that specializes in the telecommunications, energy, and utility industries.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, MasTec grew its sales at an incredible 17.7% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. MasTec’s annualized revenue growth of 9.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. MasTec’s backlog reached $18.96 billion in the latest quarter and averaged 23.4% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for MasTec’s products and services but raises concerns about capacity constraints.

This quarter, MasTec reported year-on-year revenue growth of 15.8%, and its $3.94 billion of revenue exceeded Wall Street’s estimates by 5.9%. Company management is currently guiding for a 22% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, similar to its two-year rate. This projection is above the sector average and suggests its newer products and services will help sustain its recent top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without.

Operating Margin

MasTec’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 3% over the last five years. This profitability was lousy for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, MasTec’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, MasTec generated an operating margin profit margin of 4.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

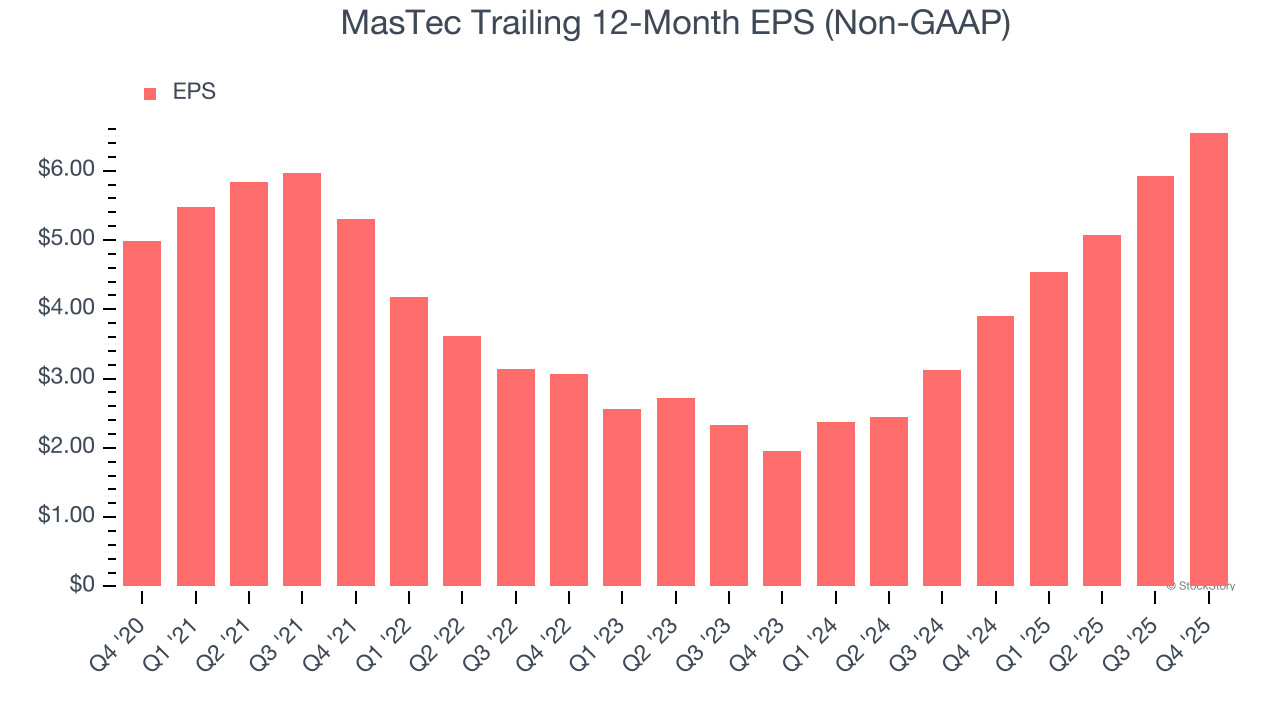

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

MasTec’s EPS grew at an unimpressive 5.6% compounded annual growth rate over the last five years, lower than its 17.7% annualized revenue growth. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

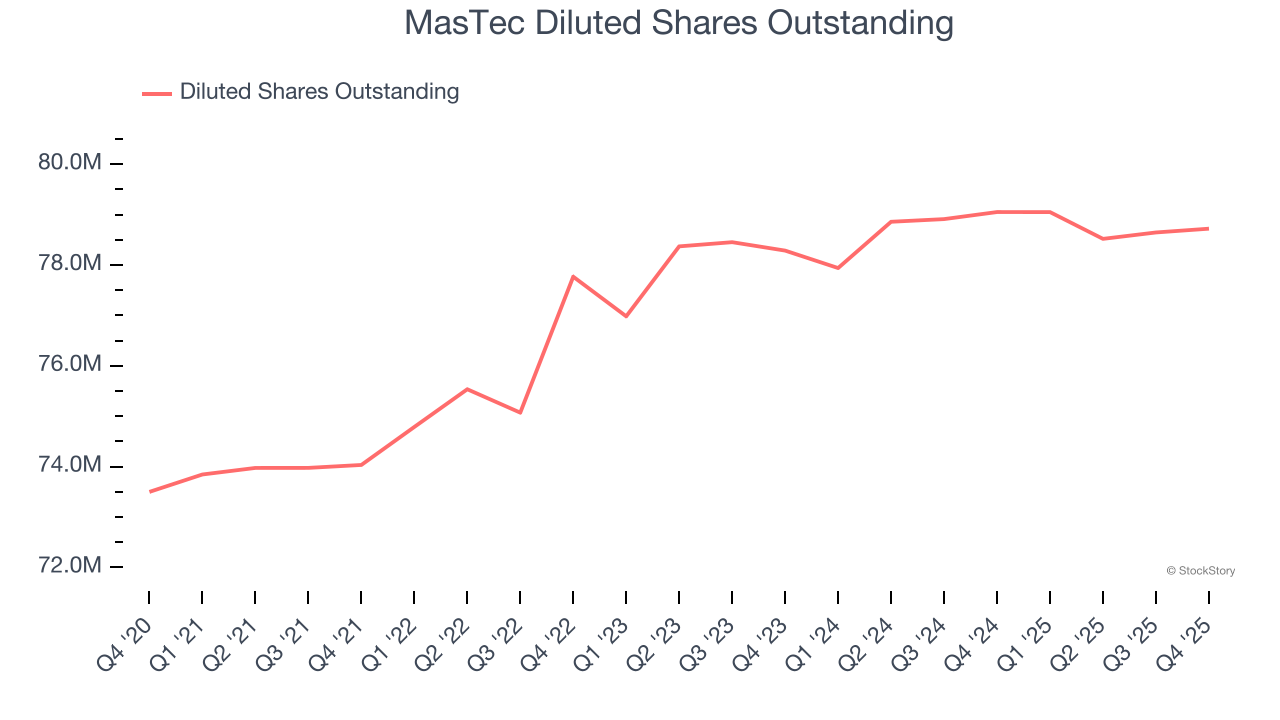

Diving into the nuances of MasTec’s earnings can give us a better understanding of its performance. A five-year view shows MasTec has diluted its shareholders, growing its share count by 7.1%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For MasTec, its two-year annual EPS growth of 82.8% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, MasTec reported adjusted EPS of $2.07, up from $1.44 in the same quarter last year. This print beat analysts’ estimates by 6.4%. Over the next 12 months, Wall Street expects MasTec’s full-year EPS of $6.55 to grow 25.4%.

Key Takeaways from MasTec’s Q4 Results

We were impressed by MasTec’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 3% to $298.58 immediately following the results.

MasTec may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Inspire Medical Systems (INSP) Shares Decline—Here’s What Caused It

US agency approves Charter Communications’ $34.5 billion deal to buy Cox

Argentina aprueba dos proyectos mineros, de oro y de plata, bajo el esquema RIGI