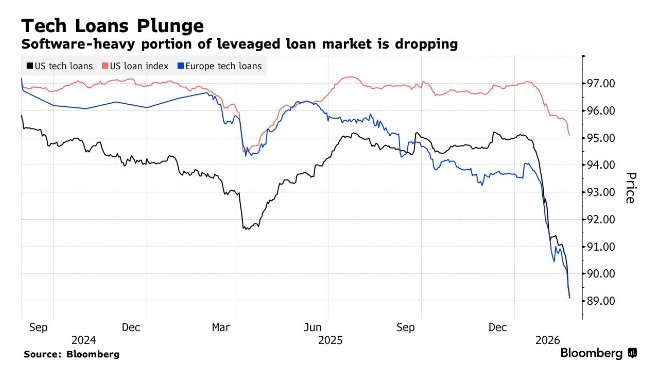

Debt Peak Meets AI Revolution: Bain Capital Warns of Impending Wave of Defaults in the Software Industry

According to Zhicheng Finance, Bain Capital recently warned that as the disruptive impact of artificial intelligence (AI) technology continues to expand, coupled with an approaching debt repayment peak, the software industry faces the risk of loan default rates soaring into double digits.

Angelo Rufino, Head of Bain Capital’s North American Special Situations and European Corporate Special Situations, said in an interview: “Market stress is about to emerge. This is just a typical credit cycle phenomenon—an industry first gets overly hyped, followed by an influx of massive capital.”

Rufino predicts that the software industry default rate may jump to the high single digits or low double digits. By contrast, the overall U.S. leveraged loan default rate is expected to reach a maximum of only 5% this year, remaining steady in 2025.

Currently, Wall Street has repeatedly sounded the alarm, warning that new AI productivity tools will not only impact the software industry but may also reshape financial services and asset management sectors.

Rufino’s viewpoint aligns with previous comments by Bruce Richards, Chairman of Marathon Asset Management LP. Earlier on Thursday, Richards said that in the private credit sector, the software industry default rate could reach 15%—about three times his projected overall direct loan default rate, and close to the worst-case scenario predicted by UBS analysts.

As an investment institution deeply involved in the software sector, Bain Capital holds assets such as Rocket Software Inc. Although the latter has recently come under debt pressure, Bain revealed that its Special Situations unit’s exposure to software industry risk is less than 5%, without disclosing the total amount of software debt holdings.

Rufino believes that although many software service companies have stable subscription revenues and provide practical products at relatively low costs, the rise of AI will limit their ability to negotiate price increases. This will drag down company valuation multiples and the sustainable enterprise value, making debt refinancing more difficult.

“As the credit cycle fully evolves, the market will be forced to readjust capital structures to match the profitability of these business models,” Rufino said. “Certainly, quite a few companies will face refinancing difficulties.”

However, he also noted that after years of deleveraging and with the U.S. economy growing steadily, a crisis in the software industry is unlikely to spread into a systemic credit market problem.

“This turmoil is most likely to be confined to a few specific industries. I do not think the overall credit market will see a significant surge in default rates,” Rufino stated.

But he also believes that considering the potential risks in the market, current credit spreads remain too narrow. The premium of high-yield bonds over U.S. Treasuries is about 300 basis points, “which is not attractive from a risk-reward perspective.”

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

RBC's Initiation: Assessing Lilly's Path to Obesity Market Leadership

Can Ethereum’s price rally to $2,400 after BlackRock’s latest bet?

Organogenesis: The Q4 Beat Was Priced In, Now the Guidance Reset Is the Game