Vulcan Materials Rises 1.13% Even with 473rd Volume Ranking and Uncertain Earnings Prospects

Market Overview

On Tuesday, Vulcan Materials (VMC) ended the trading day up by 1.13%, even as trading volume dropped sharply by nearly 30% to $0.29 billion, placing it 473rd in activity rankings. This movement came after the company released a mixed fourth-quarter 2025 earnings report: both revenue and earnings per share fell short of forecasts, but the company emphasized notable year-over-year improvements in adjusted EBITDA and operating cash flow. Institutional investors showed varied responses, with some increasing their positions and others scaling back.

Major Influences

The main factor behind VMC's recent price swings was its Q4 2025 earnings announcement on February 17. The company posted earnings per share of $1.70 and revenue of $1.91 billion, both below analyst expectations of $2.13 and $1.95 billion. This shortfall led to an 8.63% drop in pre-market trading, bringing the stock to $300.66. Despite missing estimates, Vulcan Materials demonstrated resilience in several financial areas: adjusted EBITDA climbed 13% year-over-year to $2.3 billion, EBITDA margins improved by 160 basis points to 29.3%, and operating cash flow increased 29% to $1.8 billion. These positive metrics helped offset the disappointment from the earnings miss, highlighting the company’s operational strength and effective cost controls.

Looking ahead, management’s guidance for 2026 influenced investor sentiment. The company expects aggregate shipments to grow by 1-3%, freight-adjusted selling prices to rise 4-6%, and adjusted EBITDA to land between $2.4 billion and $2.6 billion. While these projections suggest cautious optimism, seven analysts recently lowered their earnings forecasts, citing concerns about short-term execution risks. This skepticism was reinforced by DA Davidson’s downgrade, which reduced its price target from $330 to $320 and maintained a neutral stance.

Institutional activity further complicated the outlook. Vanguard Group and JPMorgan Chase raised their stakes in the third quarter of 2025, while Westfield Capital Management trimmed its holdings by 4.9%. These moves reflected differing perspectives on VMC’s prospects. Meanwhile, company insiders sold shares worth $2.69 million over the past three months, including transactions by SVP Denson Franklin III and Director Melissa Anderson. The combination of insider sales and earnings misses has prompted questions about internal confidence.

Despite these challenges, Vulcan Materials’ approach to returning capital to shareholders remains a bright spot. Vulcan distributed $698 million through dividends and share buybacks in fiscal 2025, and free cash flow jumped by more than 40%. The company recently raised its dividend to $0.52 per share, up 6.12% from the previous quarter, signaling ongoing commitment to shareholder value. However, the stock’s forward price-to-earnings ratio of 37.64 and beta of 1.07 indicate higher expectations compared to broader market averages.

External factors also play a role in VMC’s performance. As a supplier of construction materials, the company’s results are closely linked to infrastructure spending and economic cycles. Analysts noted that recent tariffs and infrastructure legislation could boost demand in the sector, though Vulcan’s conservative guidance suggests a measured approach to leveraging these opportunities. The stock’s 50-day moving average stands at $303.65, with the 200-day average at $297.27, hinting at a possible support level for near-term declines. The consensus analyst price target of $323.64 reflects ongoing optimism about future prospects.

Overall, VMC’s recent stock movement illustrates a balance between short-term earnings disappointments, robust operational performance, and mixed investor sentiment. While disciplined capital management and strategic initiatives provide a foundation for sustained growth, downward revisions from analysts and insider selling highlight the need for a cautious outlook. The company’s ability to maintain its upward momentum will depend on successful execution of its 2026 plans and broader economic trends.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

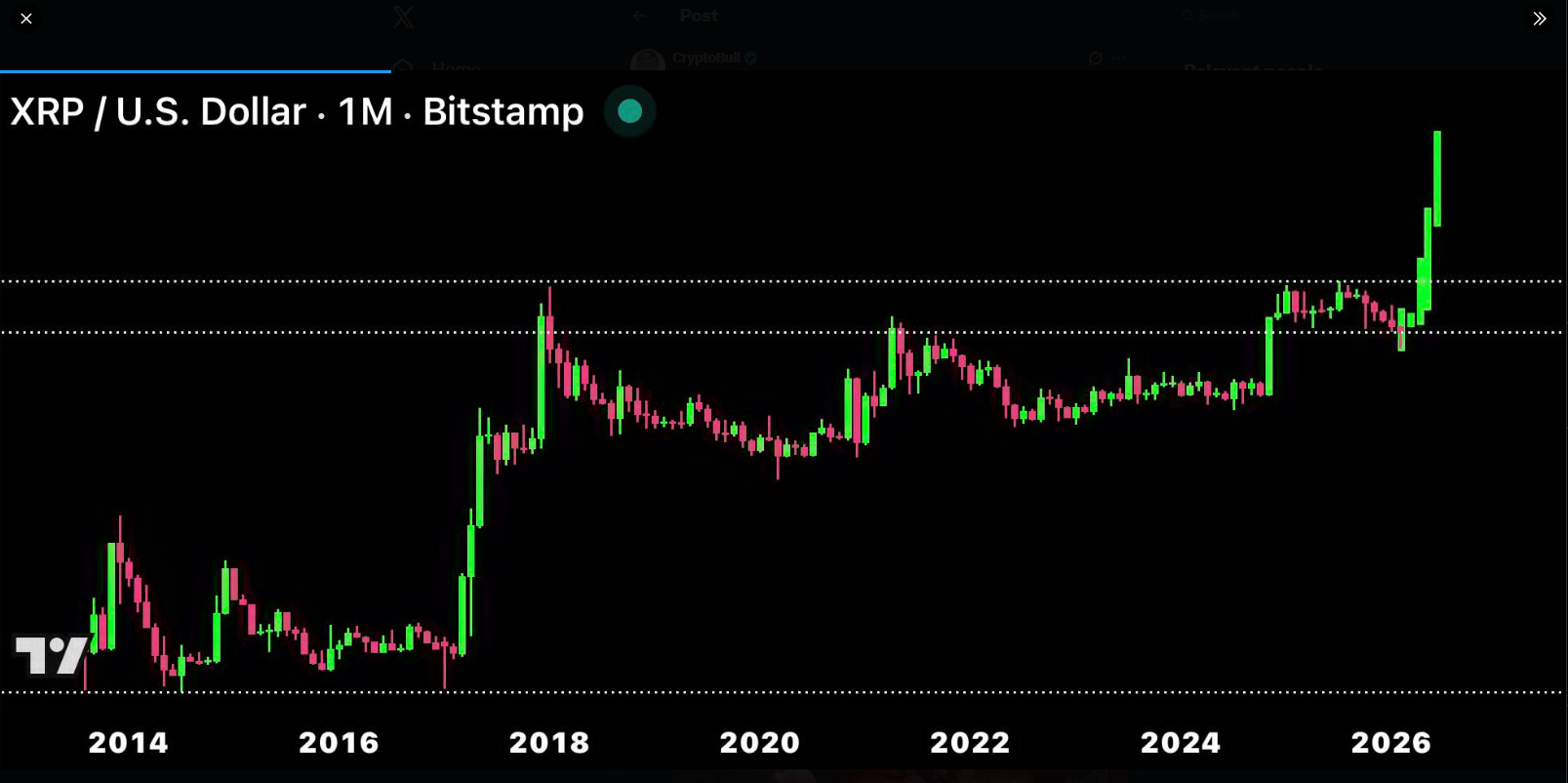

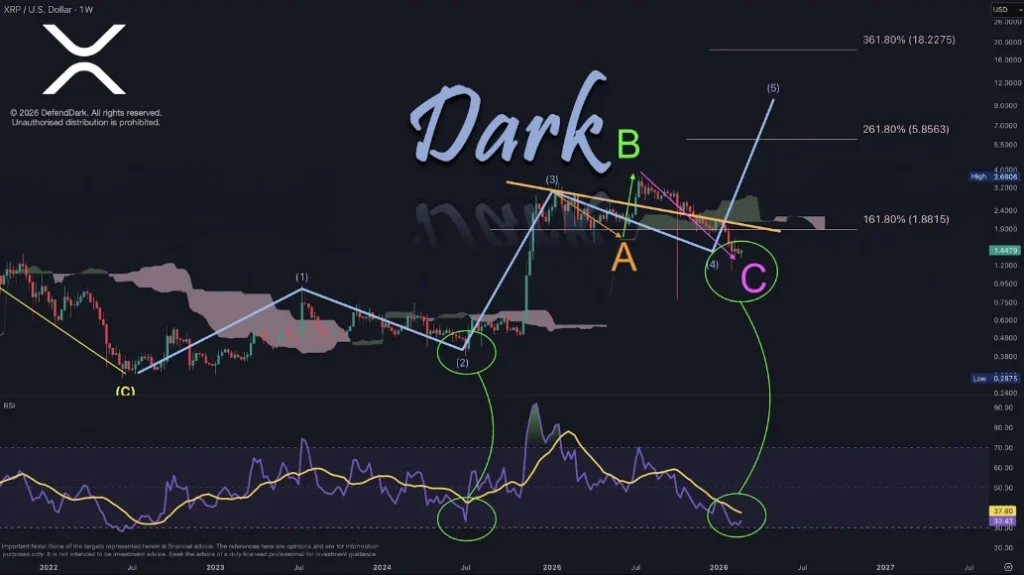

Say What You Want — XRP’s Chart Is Screaming $50 — Analyst

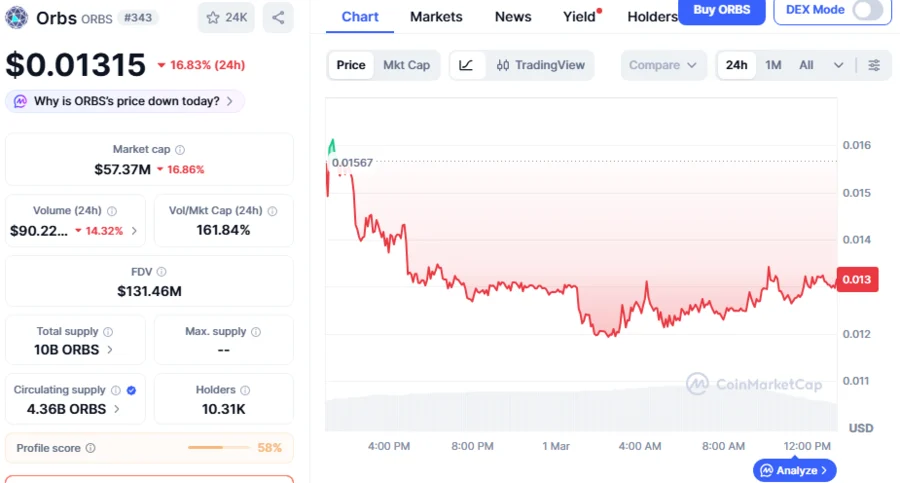

ORBS Price Erupts 36.9% As Analyst Identifies Large Bullish Candle That Sets To Trigger Further Market Rally

Uniswap Price Eyes $4.60 as Fee Burn Vote Advances