Globalstar (NASDAQ:GSAT) Delivers Unexpected Q4 CY2025 Revenue

Globalstar Q4 2025 Earnings Overview

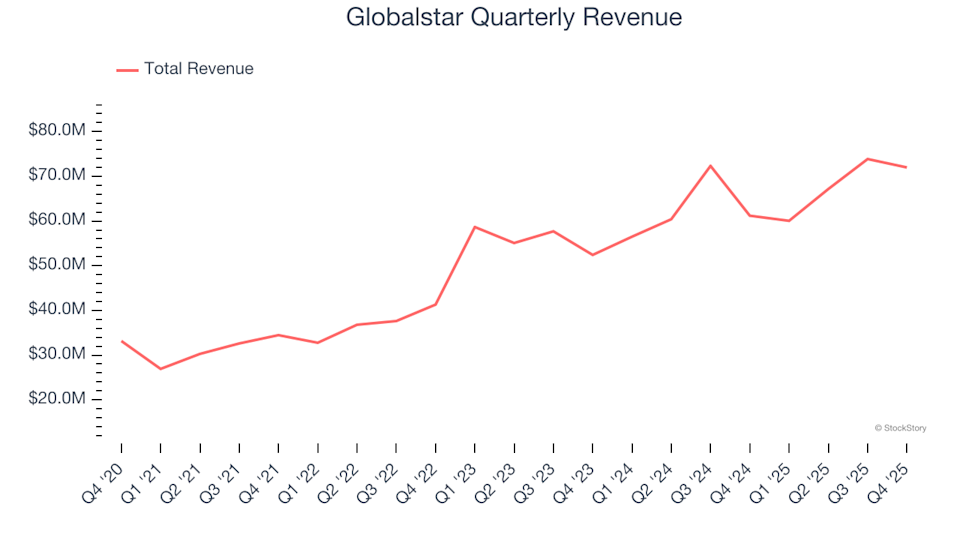

Globalstar (NASDAQ: GSAT), a provider of satellite communication services, released its fourth quarter results for calendar year 2025, surpassing revenue expectations with a 17.6% year-over-year increase to $71.96 million. However, the company’s projected full-year revenue of $292.5 million (midpoint) was 3.9% lower than what analysts anticipated. The reported GAAP loss per share of $0.11 was notably wider than consensus estimates.

Highlights from Globalstar’s Q4 2025 Results

- Revenue: $71.96 million, beating analyst forecasts of $70.64 million (17.6% growth year-over-year, 1.9% above expectations)

- GAAP EPS: -$0.11, compared to analyst estimates of -$0.04 (missed expectations)

- Adjusted EBITDA: $32.37 million, below analyst projections of $35.71 million (45% margin, 9.4% shortfall)

- Operating Margin: -0.5%, improved from -6.9% in the same quarter last year

- Free Cash Flow Margin: 53.2%, a decrease from 286% in the prior year’s quarter

- Market Cap: $7.34 billion

About Globalstar

Globalstar is recognized for enabling the emergency SOS feature on recent Apple iPhones. The company operates a constellation of low-earth orbit satellites, delivering voice and data connectivity in areas where traditional cellular networks are unavailable.

Revenue Performance

Consistent growth over time is a hallmark of a strong business. While any company can achieve short-term gains, sustained expansion signals lasting quality.

With $273 million in revenue over the past year, Globalstar is considered a smaller player in the business services sector. This size can present challenges compared to larger firms with broader resources and distribution networks, but it also allows for faster growth potential.

Over the last five years, Globalstar has achieved a compound annual revenue growth rate of 16.3%, indicating robust demand relative to many peers in the industry.

While we value long-term growth, recent developments and innovations are also important. Globalstar’s annualized revenue growth rate over the past two years was 10.4%, slightly below its five-year average, but still reflects healthy demand.

This quarter, Globalstar’s revenue rose 17.6% year-over-year, exceeding Wall Street’s expectations by 1.9%.

Looking forward, analysts predict Globalstar’s revenue will grow by 11.5% over the next year, aligning with its recent growth rate. This outlook suggests that new products and services may drive further improvements in top-line performance.

Profitability and Operating Margin

Operating margin is a key indicator of profitability, showing how much profit remains after covering core expenses such as marketing and research and development.

Although Globalstar broke even operationally this quarter, the company has generally faced challenges over a longer period. Its high costs have resulted in an average operating margin of -10.5% over the past five years. Companies in business services that remain unprofitable warrant careful scrutiny, as they may be vulnerable during market downturns.

On a positive note, Globalstar’s operating margin has improved by 57.9 percentage points over the last five years, thanks to sales growth providing operational leverage. Nonetheless, achieving sustained profitability will require further progress.

This quarter, Globalstar’s operating margin stood at -0.5%.

Earnings Per Share (EPS) Trends

Tracking EPS over time helps determine whether a company’s growth is translating into profits. While Globalstar’s annual earnings remain negative, the company has reduced its losses, improving EPS by an average of 27.5% per year over the past five years. The upcoming quarters will be crucial for evaluating its path to profitability.

Examining more recent EPS trends, Globalstar’s two-year annual EPS growth rate was 13.6%, below its five-year average but still positive. In Q4, the company reported an EPS of -$0.11, an improvement from -$0.42 in the same quarter last year, though it missed analyst expectations. Wall Street forecasts that Globalstar will continue to narrow its losses, with full-year EPS expected to improve from -$0.15 to -$0.04 over the next 12 months.

Summary and Investment Considerations

Globalstar’s Q4 results showed stronger-than-expected revenue, but its full-year guidance and EPS fell short of analyst forecasts. Overall, the quarter was somewhat weaker, and the stock declined 1.9% to $56.41 immediately after the announcement.

While the earnings report was mixed, investors may want to consider whether this creates a buying opportunity. Ultimately, long-term business quality and valuation are more important than a single quarter’s performance when deciding to invest.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Crypto Biz: A Bitcoin treasury shareholder revolt

Alchemy introduces autonomous payment rails for AI agents on Base

Why Walker & Dunlop (WD) Shares Are Down Today

Exclusive-QIA, Visa and ADIA set to anchor SoftBank's PayPay IPO, sources say