DTI or HAL: Which Oilfield Services Stock Provides Greater Value?

The Role of Oilfield Service Providers in the Energy Sector

Oil and gas field service companies are essential to the global energy landscape. Firms such as Drilling Tools International (DTI) and Halliburton (HAL) provide the specialized equipment, technology, and expertise that upstream operators rely on to locate, drill, complete, and maintain oil and gas wells. Their offerings range from drilling tools, well completion systems, and pressure control devices to well maintenance solutions. Without these services, energy production would be less safe, more costly, and far less efficient.

These companies are also at the forefront of technological advancement, introducing innovations that accelerate drilling, cut expenses, enhance recovery rates, and improve both safety and environmental outcomes.

Both DTI and HAL help operators increase productivity and minimize downtime, though their business models differ. Halliburton delivers a broad suite of integrated services, while DTI specializes primarily in drilling tools and equipment rentals.

Drilling Tools International: Growth and Challenges

Drilling Tools International currently operates in two contrasting markets. The company is experiencing robust, sustained growth in the Eastern Hemisphere, particularly in the Middle East, where demand for its Drill-N-Ream tools remains strong. This momentum allows DTI to command higher prices, keep its assets well utilized, and improve profit margins through cost management.

Conversely, the North American market—especially U.S. land operations—remains challenging, with lower rig counts and ongoing pricing pressures impacting results. As a result, management anticipates flat revenues and a decline in adjusted EBITDA for fiscal 2025. For investors, DTI’s story is one of balancing international expansion with domestic headwinds. While the company’s overseas growth demonstrates adaptability and the ability to seize new opportunities, its performance is still closely tied to the North American market. Investors may need patience as meaningful improvement could depend on a recovery in U.S. drilling activity.

Halliburton: Strategic Positioning in a Shifting Market

Halliburton is navigating a changing market environment with a disciplined approach, though it faces some short-term obstacles. The company’s main growth engine is its differentiated international strategy, which leverages advanced technologies—such as the Zeus electric fracturing system and iCruise drilling platforms—and collaborative partnerships. These innovations are gaining momentum in important regions like Latin America and the Middle East, positioning Halliburton to benefit from the next wave of global demand.

However, Halliburton remains cautious about North America, expecting a high-single-digit revenue decline in 2026 due to reduced customer activity and the company’s own decision to idle less profitable fleets. This signals a focus on capital efficiency and long-term returns over short-term market share, with the goal of generating sustainable free cash flow and resilience through industry cycles.

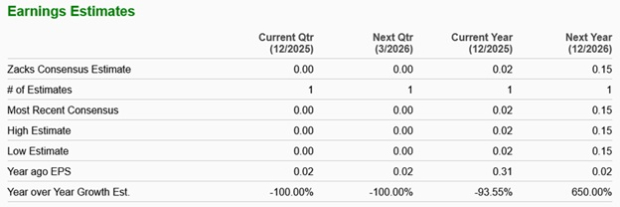

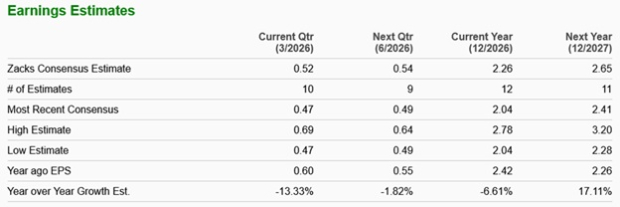

DTI vs. HAL: Zacks Earnings Estimates

According to Zacks, DTI’s consensus estimate for 2026 earnings per share points to a remarkable 650% increase compared to the previous year.

Image Source: Zacks Investment Research

For Halliburton, Zacks projects a 6.61% year-over-year decrease in 2026 EPS, followed by a 17.11% increase in 2027.

Image Source: Zacks Investment Research

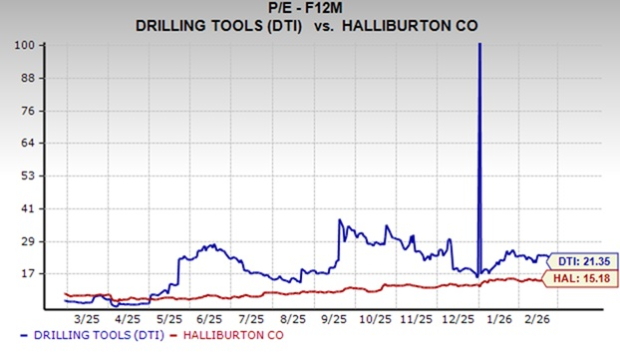

Valuation: Comparing DTI and HAL

Drilling Tools International currently trades at a forward 12-month price-to-earnings (P/E) ratio of 21.35, while Halliburton’s forward P/E stands at 15.18. This suggests that Halliburton is valued more attractively based on projected earnings.

Image Source: Zacks Investment Research

Stock Price Performance: DTI vs. HAL

Over the past six months, DTI’s share price has climbed 86.3%, while HAL has gained 60.2% during the same period.

Image Source: Zacks Investment Research

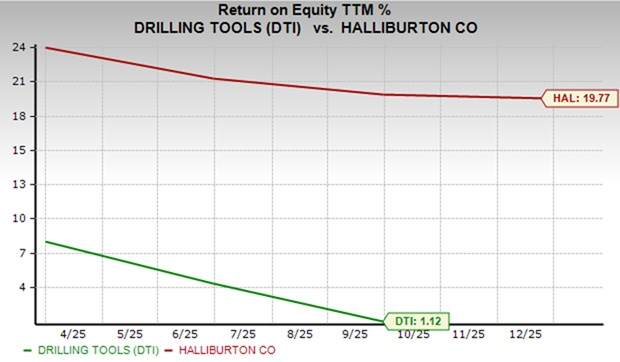

Return on Equity: Efficiency Comparison

Return on Equity (ROE) measures how effectively a company uses its shareholders’ capital to generate profits. Halliburton’s current ROE is 19.77%, significantly higher than DTI’s 1.12%.

Image Source: Zacks Investment Research

Which Stock Is the Better Choice: DTI or HAL?

DTI presents a higher-risk, higher-reward scenario. The company benefits from strong demand in the Middle East and has shown impressive recent stock performance and a sharp projected earnings increase. However, its significant exposure to the weaker North American market, higher valuation, and low return on equity add uncertainty. Investors who believe in a rebound in U.S. drilling and are comfortable with volatility may view DTI as a potential cyclical recovery opportunity, but patience and risk tolerance are key.

In contrast, Halliburton offers a more balanced and fundamentally solid investment case. With diversified global operations, advanced technology, superior return on equity, a lower valuation, and a mixed near-term earnings outlook, HAL is better equipped to weather industry cycles. While North American challenges persist, Halliburton’s disciplined strategy and stronger financials make it a more suitable option for those seeking stability, steady returns, and long-term value in the oilfield services sector. Currently, both DTI and HAL hold a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US Foods (USFD) Raised to Strong Buy: Find Out the Reasons

Sunrun (RUN) Raised to Strong Buy: What Are the Implications for Its Shares?