Is It a Good Time to Invest in Trending Stock AppLovin Corporation (APP)?

AppLovin: Recent Performance and Outlook

AppLovin (APP) has recently attracted significant attention from investors. Let’s explore the main factors that could influence the stock’s short-term trajectory.

Stock Performance Overview

Over the past month, shares of this mobile app technology company have declined by 21.8%. In comparison, the Zacks S&P 500 composite index saw a slight increase of 0.6%, while the Zacks Technology Services sector, which includes AppLovin, dropped by 4.4%. This raises the question: What might be next for AppLovin’s stock?

While news headlines or speculation can cause swift price movements, long-term investors often focus on fundamental indicators when making decisions.

Earnings Estimate Trends

At Zacks, changes in projected earnings are a key focus, as they often signal shifts in a company’s underlying value. When analysts raise their earnings forecasts, it typically boosts a stock’s fair value, which can attract buyers and push the price higher. Historical data shows a strong link between earnings estimate revisions and near-term stock price changes.

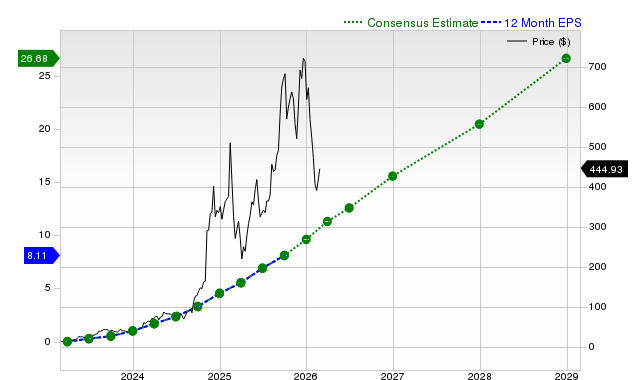

- For the current quarter, AppLovin is projected to earn $3.36 per share—a 101.2% increase from the same period last year. Over the past month, the consensus estimate has risen by 6.8%.

- The consensus for this fiscal year is $15.59 per share, up 55.3% year-over-year, with a 2.9% increase in the past 30 days.

- Looking ahead to next year, analysts expect $20.48 per share, a 31.4% jump from the prior year, with a 6.1% increase in the last month.

Zacks’ proprietary rating system, the Zacks Rank, incorporates these estimate changes and other factors. AppLovin currently holds a Zacks Rank #3 (Hold), suggesting a neutral outlook.

Forward 12-Month EPS Estimate Trend

Revenue Growth Projections

Consistent revenue growth is essential for sustained earnings expansion. For the current quarter, AppLovin’s sales are expected to reach $1.77 billion, reflecting a 19.2% increase from the previous year. Full-year revenue estimates stand at $8.02 billion for this year (+38.1%) and $10.38 billion for next year (+29.5%).

Recent Results and Earnings Surprises

In the latest quarter, AppLovin reported $1.66 billion in revenue, up 20.8% year-over-year. Earnings per share came in at $3.24, compared to $1.73 a year earlier. These results exceeded the Zacks Consensus Estimate for revenue by 2.88% and for EPS by 12.11%. The company has surpassed consensus EPS and revenue estimates in each of the last four quarters.

Valuation Analysis

Evaluating a stock’s valuation is crucial for investment decisions. Comparing current valuation ratios—such as price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF)—to historical averages and industry peers helps determine if a stock is fairly priced.

The Zacks Value Style Score, which grades stocks from A to F based on various valuation metrics, rates AppLovin as a D. This suggests the stock is currently trading at a premium compared to its peers.

Conclusion

The information above, along with additional resources on Zacks.com, can help investors decide whether to pay attention to the current market buzz around AppLovin. With a Zacks Rank #3, the stock is expected to perform in line with the broader market in the near future.

Featured Stock Picks

Zacks’ research team has identified five stocks with strong potential to double in value in the coming months. Among them, Director of Research Sheraz Mian highlights a lesser-known satellite communications company poised for significant growth as the space industry expands. Analysts anticipate a major revenue surge in 2025. While not all top picks achieve such gains, this one could outperform previous winners like Hims & Hers Health, which soared over 200%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Crypto winter fears dismissed as whale accumulation, ETF inflow signals snowball

3 Motives to Let Go of PCOR and One Alternative Stock Worth Purchasing

3 Expanding Companies We’re Reconsidering

The Zacks Analyst Blog Highlights Apple and Adobe