Wall Street experts predict Aecom (ACM) shares could climb by 29.65%. Is it possible for the stock to reach this level?

ACM Stock Outlook: Analyst Targets and Earnings Trends

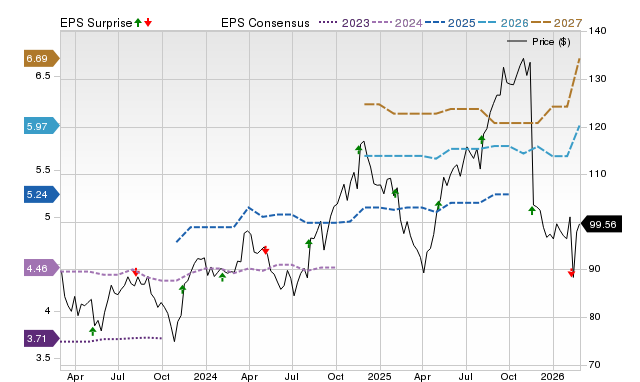

ACM (Aecom Technology) finished its most recent trading session at $99.56, marking a 2.1% increase over the past month. Despite this gain, analysts on Wall Street suggest there may be significant room for further growth, with an average price target of $129.08—representing a potential 29.7% rise.

The average target is based on 12 short-term projections, with a standard deviation of $12.09. The most conservative estimate stands at $110.00, which would be a 10.5% increase from the current price, while the most bullish forecast predicts the stock could climb 50.7% to $150.00. The standard deviation is key for understanding how much analysts agree; a lower value means greater consensus.

Although investors often focus on consensus price targets, relying solely on these figures can be risky, as analysts’ objectivity and accuracy have been questioned. Making investment decisions based only on price targets may not be wise.

Beyond the consensus price target, optimism among analysts regarding ACM’s earnings outlook further supports the case for potential gains. Many experts now expect the company to deliver stronger earnings than previously forecasted. While upward revisions in earnings estimates don’t specify how much the stock might rise, they have historically been reliable indicators of positive price movement.

Price Targets, Consensus, and Earnings Surprises

Understanding Analyst Price Targets

Research from universities worldwide suggests that price targets often mislead investors more than they help. Studies show that, regardless of analyst agreement, these targets rarely predict a stock’s actual trajectory.

Wall Street analysts possess deep knowledge of company fundamentals and industry dynamics, but many set overly optimistic targets. This is often done to generate interest in companies their firms are connected to or wish to partner with, leading to inflated projections.

However, when price targets are closely grouped—reflected by a low standard deviation—it signals strong analyst consensus about the stock’s direction and potential. While this doesn’t guarantee the stock will reach the average target, it provides a useful starting point for further research into underlying drivers.

Investors should approach price targets with caution. While they shouldn’t be ignored, relying on them alone can result in disappointing returns. Skepticism is advised.

Reasons ACM May See Further Gains

Analysts’ increasing confidence in ACM’s earnings prospects, shown by consistent upward revisions to EPS estimates, is a solid reason to expect the stock to rise. Empirical evidence links trends in earnings estimate changes to short-term stock price movements.

The Zacks Consensus Estimate for ACM’s current year has risen 5.8% in the past month, with three upward revisions and no downgrades.

ACM currently holds a Zacks Rank #1 (Strong Buy), placing it among the top 5% of over 4,000 ranked stocks based on four earnings-related factors. This ranking, backed by an externally audited track record, offers a strong indication of near-term upside potential.

In summary, while the consensus price target may not precisely predict ACM’s future gains, the direction it suggests aligns with positive analyst sentiment and earnings trends.

Top Stock Picks: Potential to Double

Zacks’ research team has identified five stocks with the highest likelihood of gaining 100% or more in the coming months. Among these, Director of Research Sheraz Mian highlights a standout pick—a lesser-known satellite communications company. With the space industry expected to reach a trillion-dollar valuation and a rapidly expanding customer base, analysts anticipate a major revenue surge in 2025. While not all picks succeed, this one could outperform previous winners like Hims & Hers Health, which soared over 209%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Heavy Transportation Equipment Stocks Q4 Analysis: Comparing Federal Signal (NYSE:FSS) With Its Competitors

Azitra's Failed Vote: A Tactical Play on Distressed Pricing and Dilution Risk