Blackbaud and Fortune Brands Innovations have been featured as Zacks Bull and Bear of the Day

Press Release Overview

Chicago, IL – February 27, 2026 – Zacks Equity Research has identified Blackbaud (BLKB) as the Bull of the Day and Fortune Brands Innovations (FBIN) as the Bear of the Day. The report also features insights on The Trade Desk, Inc. (TTD) and Meta Platforms, Inc. (META).

Summary of Featured Stocks

- Bull of the Day: Blackbaud (BLKB)

- Bear of the Day: Fortune Brands Innovations (FBIN)

- Additional analysis: The Trade Desk (TTD) and Meta Platforms (META)

Bull of the Day: Blackbaud (BLKB)

As software stocks experience a significant downturn, Blackbaud stands out as a potential opportunity for investors seeking value. Currently holding a Zacks Rank #1 (Strong Buy), Blackbaud is highlighted as the Bull of the Day.

With shares trading near a 52-week low around $45, Blackbaud appears oversold, primarily due to widespread concerns about AI disruption rather than any company-specific weakness.

Investors interested in socially responsible investments may find Blackbaud appealing, as the company’s ESG-driven strategy and advanced cloud software solutions are tailored to support organizations focused on social impact.

About Blackbaud

Blackbaud delivers a comprehensive suite of cloud and on-premise software and services to organizations of all sizes. Their offerings include solutions for fundraising, marketing, advocacy, CRM, corporate social responsibility, peer-to-peer fundraising, financial management, payment processing, and analytics.

Why Blackbaud May Be Undervalued

- Resilient Market Niche: Blackbaud’s core customers—nonprofits, educational institutions, and social-impact organizations—rely on specialized workflows and compliance needs that are less susceptible to generic AI replacement. This means sector-wide AI fears may not directly affect Blackbaud’s business model.

- Stable, Recurring Revenue: The company’s client base is typically long-term and mission-critical, making customer turnover rare even during technological shifts. This stability is often overlooked during broad market selloffs. Blackbaud is projected to achieve 4% sales growth in both FY26 and FY27, with revenue estimates approaching $1.22 billion.

- Solid Fundamentals: There is no evidence of company-specific issues impacting Blackbaud. The recent decline in share price is a result of industry-wide repricing, not a deterioration in the company’s earnings or competitive standing.

- Market Overreaction: When investors exit software stocks en masse, fundamentally sound companies like Blackbaud can become undervalued, creating potential opportunities for rebound.

Upward EPS Revisions for Blackbaud

Supporting the case for a recovery, Blackbaud’s full-year EPS estimates have been revised upward by more than 4% for FY26 and FY27 after the company exceeded Q4 expectations. Annual earnings are forecasted to jump 16% this year, with FY27 EPS expected to climb another 11% to $5.76.

Attractive Valuation

Blackbaud’s recent share price decline, driven by sector sentiment rather than company performance, has made the stock more affordable relative to its cash flow and growth prospects. Currently, BLKB trades at just 9 times forward earnings—a significant discount compared to the S&P 500 and the Zacks Computer-Software Industry average of 22 times forward earnings, and an 80% discount to its 10-year median of 45 times.

Conclusion

When entire sectors are sold off indiscriminately, quality companies like Blackbaud can be pulled down despite strong fundamentals. As market volatility subsides, Blackbaud emerges as a compelling buy-the-dip candidate, especially for those seeking ESG-focused investments.

Bear of the Day: Fortune Brands Innovations (FBIN)

With a Zacks Rank #5 (Strong Sell), Fortune Brands Innovations is currently viewed as a stock to avoid within the construction sector. The company, which supplies home, security, and building products, faces several challenges.

Weakening fundamentals, conservative guidance, leadership changes, and a history of underperformance suggest ongoing instability for the company.

Over the past five years, FBIN has significantly lagged behind both the broader market and its industry peers in the Zacks Building Products-Air Conditioner and Heating category. The stock has not presented an appealing case for investors seeking growth or margin expansion.

Recent Performance and Challenges

- Disappointing Q4 Results: Fortune Brands reported Q4 EPS of $0.86, missing expectations by 14% and declining from $0.98 a year ago. Revenue fell 2% year-over-year to $1.07 billion, falling short of estimates.

- Market Pressures: Lower demand and increased competition have contributed to the revenue shortfall, with rivals gaining market share or forcing more aggressive pricing.

- Reduced Operating Leverage: Lower sales volumes have negatively impacted profitability.

- Rising Costs: Persistent input cost pressures, including materials and tariffs, have squeezed margins.

- Cost-Cutting Measures: The company reduced its workforce by 10% and implemented cost-saving initiatives, indicating profitability concerns.

Outlook and Leadership Concerns

Fortune Brands’ guidance for fiscal 2026 points to lower-than-expected earnings and sluggish revenue growth. Full-year EPS is projected at $3.35–$3.65, well below analyst expectations of $4.06, with sales expected to be flat or grow by up to 2%. EPS estimates for FY26 and FY27 have been revised downward by 10% and 16%, respectively.

Competition is intensifying in key product categories, and the company is undergoing a CEO transition following a challenging 2025. Activist investor Ed Garden is advocating for a leadership change, adding to strategic uncertainty.

Conclusion

Although FBIN trades at a reasonable 14 times forward earnings, the company’s weakening fundamentals, leadership instability, and deteriorating risk-reward profile suggest caution. At present, Fortune Brands appears to be under pressure rather than poised for a turnaround.

Additional Insights

The Trade Desk (TTD) Shares Drop 15% Despite Beating Q4 Earnings – Opportunity or Risk?

The Trade Desk, Inc. saw its stock fall 15% in after-hours trading following its Q4 and full-year 2025 results. Despite beating earnings expectations, the company’s cautious Q1 outlook triggered the selloff. Is this a buying opportunity? Here’s a closer look:

Strong Financial Results

The Trade Desk delivered adjusted Q4 EPS of $0.59, slightly above the $0.58 estimate. Net income rose to $187 million from $182 million a year earlier, and revenue increased 14% year-over-year to $847 million, surpassing forecasts. For 2025, net income reached $443 million, up from $393 million in 2024, with annual revenue climbing 18% to $2.9 billion. The company maintained a 95% customer retention rate for the 12th consecutive year and repurchased $1.4 billion in shares, reflecting management’s confidence.

Challenges Ahead

Despite strong results, The Trade Desk’s net income margin declined to 22% from 25% a year ago, and the full-year margin slipped to 15% from 16%. The company’s Q1 2026 revenue guidance of $678 million signals slower growth, and projected adjusted EBITDA of $195 million points to lower margins. Ongoing stock-based compensation could further pressure profitability. Additionally, the company is currently led by an interim CFO, contributing to near-term uncertainty.

Investment Perspective

Although The Trade Desk posted robust earnings and revenue growth, margin compression, a cautious near-term outlook, and leadership changes make the stock less attractive at this time. Management also cited macroeconomic uncertainty, while competitors like Meta Platforms, Inc. have provided more optimistic forecasts. Should The Trade Desk return to stronger growth and improved margins, the current dip could eventually present an entry point. For now, the stock holds a Zacks Rank #4 (Sell).

See the full list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Why Consider Zacks’ Top Stock Picks?

Since 2000, Zacks’ leading stock selection strategies have significantly outperformed the S&P 500’s average annual gain of 7.7%, with some strategies achieving average annual returns of +48.4%, +50.2%, and +56.7%. Access their latest recommendations at no cost or obligation.

Contact Information

Zacks Investment Research

Phone: 800-767-3771 ext. 9339

Website: https://www.zacks.com

Zacks’ Top Stock Set to Double

The Zacks research team has identified five stocks with the highest potential to gain 100% or more in the coming months. Among these, Director of Research Sheraz Mian spotlights a lesser-known satellite communications company expected to benefit from the rapidly expanding space industry. Analysts anticipate a major revenue surge in 2025. While not all picks are guaranteed winners, this stock could outperform previous high achievers like Hims & Hers Health, which soared over 200%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

又一美联储理事呼吁:谨慎对待进一步降息!

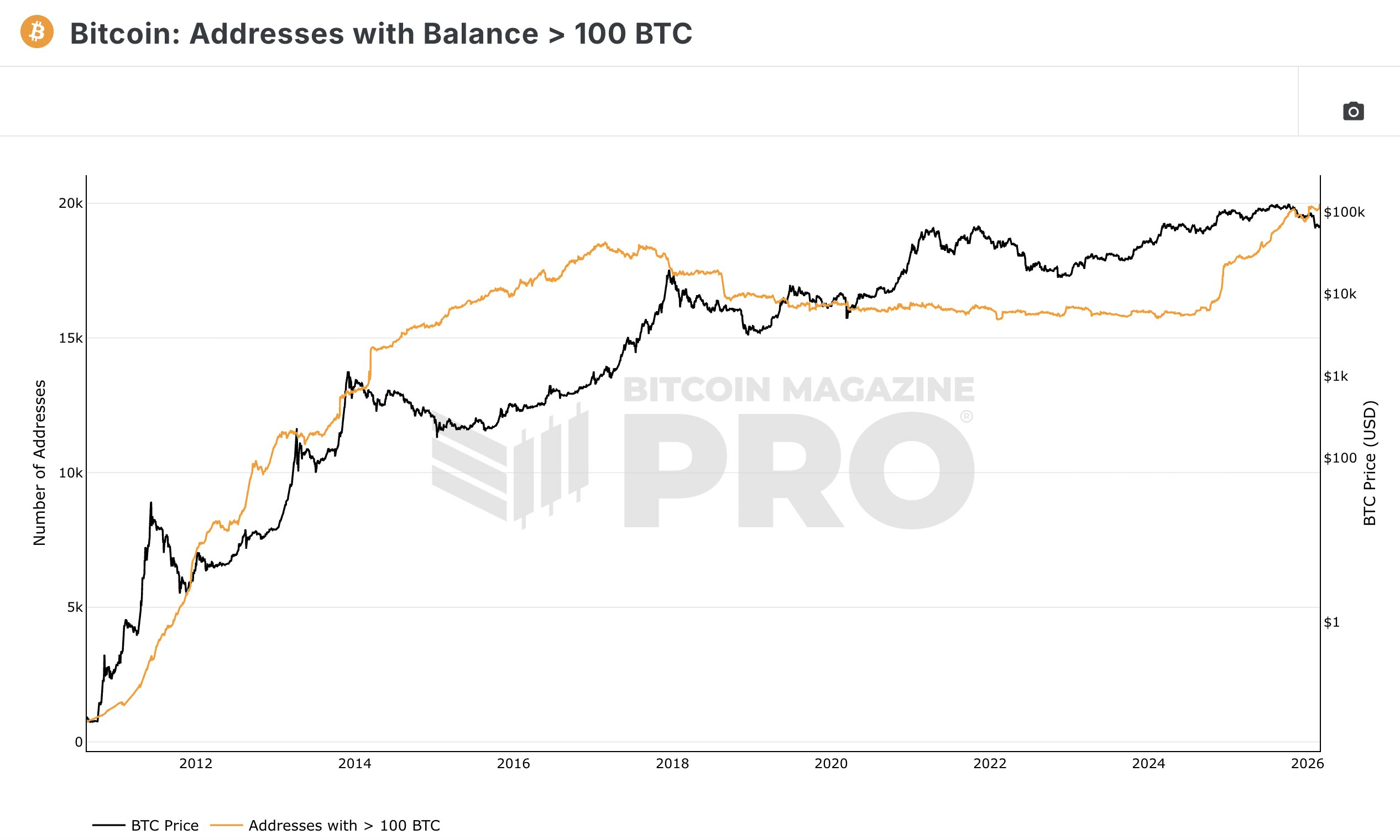

Bitcoin whale addresses holding 100 BTC hit ATH – Strategic play for H2 rally?

Ethereum smart accounts are finally coming 'within a year' — Vitalik Buterin