MakeMyTrip Q1: Discrepancy Between Growth Projections and Current Valuation

MakeMyTrip Q1: Growth Disappoints Despite Profit Upside

Recent financial results from MakeMyTrip have drawn a clear response from the market. For the first quarter, the company reported 7.8% year-over-year revenue growth, reaching $268.8 million—a figure that failed to meet the ambitious growth expectations set by investors. However, the company outperformed on profitability, with adjusted operating profit climbing 21% year-over-year to $47.3 million. This divergence between revenue and profit is at the heart of the current market narrative.

This scenario is a classic example where stronger profits are overshadowed by weaker-than-expected growth. The stock price reflects this disappointment, having dropped 44% over the past four months. While 7.8% revenue growth is respectable on its own, it fell short of the company’s guidance and the broader optimism around travel’s recovery. The market had already braced for a letdown, and the results confirmed those concerns.

Management has reiterated its full-year outlook, aiming for growth in the high teens to 20% range. Still, the latest quarter’s results fell well below that target. The profit beat highlights effective cost management, but in today’s environment, investors remain fixated on top-line expansion. The market appears to have already factored in the profit improvement, leaving the revenue miss as the main story.

Ancillary Services: MakeMyTrip’s New Growth Strategy

As the core travel segment faces growth challenges, MakeMyTrip is shifting its focus to ancillary services as a new source of margin and growth. This strategic move signals management’s intent to diversify revenue streams and boost profitability. In the third quarter of fiscal 2026, the company’s “other” segment—which includes offerings like visas, foreign exchange, insurance, and activities—delivered an adjusted margin of $27.5 million, up about 45% year-over-year. This substantial margin expansion demonstrates the potential of these add-on services to become a meaningful profit driver.

Management sees this as more than just a way to improve margins. According to Group COO Mohit Kabra, some ancillary businesses could eventually be large enough to report separately, creating a second growth engine alongside the core travel platform. This approach aims to shift market perception from a single, cyclical travel story to a dual-engine model with greater profitability. The company’s AI assistant, Myra, is central to this strategy, integrating these services into the booking process. A recent partnership with OpenAI is designed to turn conversational queries into bookable transactions.

Despite these promising developments, the market remains cautious. The AI integration and ancillary bundling are still in their early stages. Myra now handles over 50,000 conversations daily, but the impact on revenue is not yet significant. While the 45% margin increase is impressive, it comes from a relatively small base. The key question is whether this new growth engine can scale quickly enough to offset slower growth in the core business and support a higher valuation. For now, the ancillary story represents a future opportunity rather than a current reality.

Valuation Reset: Analyst Sentiment and Institutional Moves

Investors are now closely watching the gap between MakeMyTrip’s current valuation and its revised growth outlook. The stock is trading at a significant discount—about 50% below its 52-week high of $113.85, with the current price near $56. This suggests the market has already priced in a substantial revenue shortfall. The forward price-to-earnings ratio stands at 51.7, a premium that only makes sense if growth accelerates soon.

Analyst sentiment is becoming more cautious, with price targets being trimmed incrementally. The average target is $102, but recent updates show a trend of modest reductions. For example, Morgan Stanley lowered its target by $7 and Citi by $12, reflecting a more conservative outlook on future growth and profitability. The narrative is shifting from aggressive growth to a focus on execution and certainty.

Institutional investors are sending mixed signals. The sharp decline in the stock has attracted some buyers—Allianz Asset Management increased its stake by nearly 80% last quarter, indicating that some see value at current levels. Other funds have also added to their positions, suggesting a contrarian stance. However, these moves are isolated, and the overall sentiment remains cautious. The small target reductions and ongoing stock weakness indicate that most investors are waiting for clear evidence that the ancillary strategy can deliver sustainable growth.

Key Catalysts and Risks Ahead

The prevailing negative sentiment is driven by the gap between current growth and expectations. The next major test will be the Q2 earnings report, where MakeMyTrip must demonstrate progress toward its full-year growth target of high-teens to 20%. Any further shortfall could reinforce market concerns and put additional pressure on the stock. On the other hand, a rebound in growth—especially from international markets—could signal that the Q1 miss was temporary and prompt a re-evaluation.

Investors should also monitor the adoption and monetization of the new ancillary services. The AI-powered Myra assistant is central to this effort, and the partnership with OpenAI aims to convert conversational intent into bookings. Early usage metrics are encouraging, but the real test is whether these initiatives can drive a meaningful increase in revenue. Any signs of significant growth from the “other” segment would be a positive surprise.

Another important event is approaching in February 2026, when the company must repurchase its 0.00% Convertible Senior Notes due 2028 at par if holders exercise their rights. This scheduled cash outflow will affect the balance sheet and free cash flow in the short term. How management handles this obligation will be closely watched as the company navigates its growth transition.

In summary, MakeMyTrip’s next chapter will be defined by its ability to deliver on these catalysts. The stock’s steep decline has already priced in much of the disappointment. A positive shift in growth, driven by ancillary services and AI, could quickly change expectations. Until then, the risk of continued growth shortfalls and further guidance resets remains the dominant theme.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

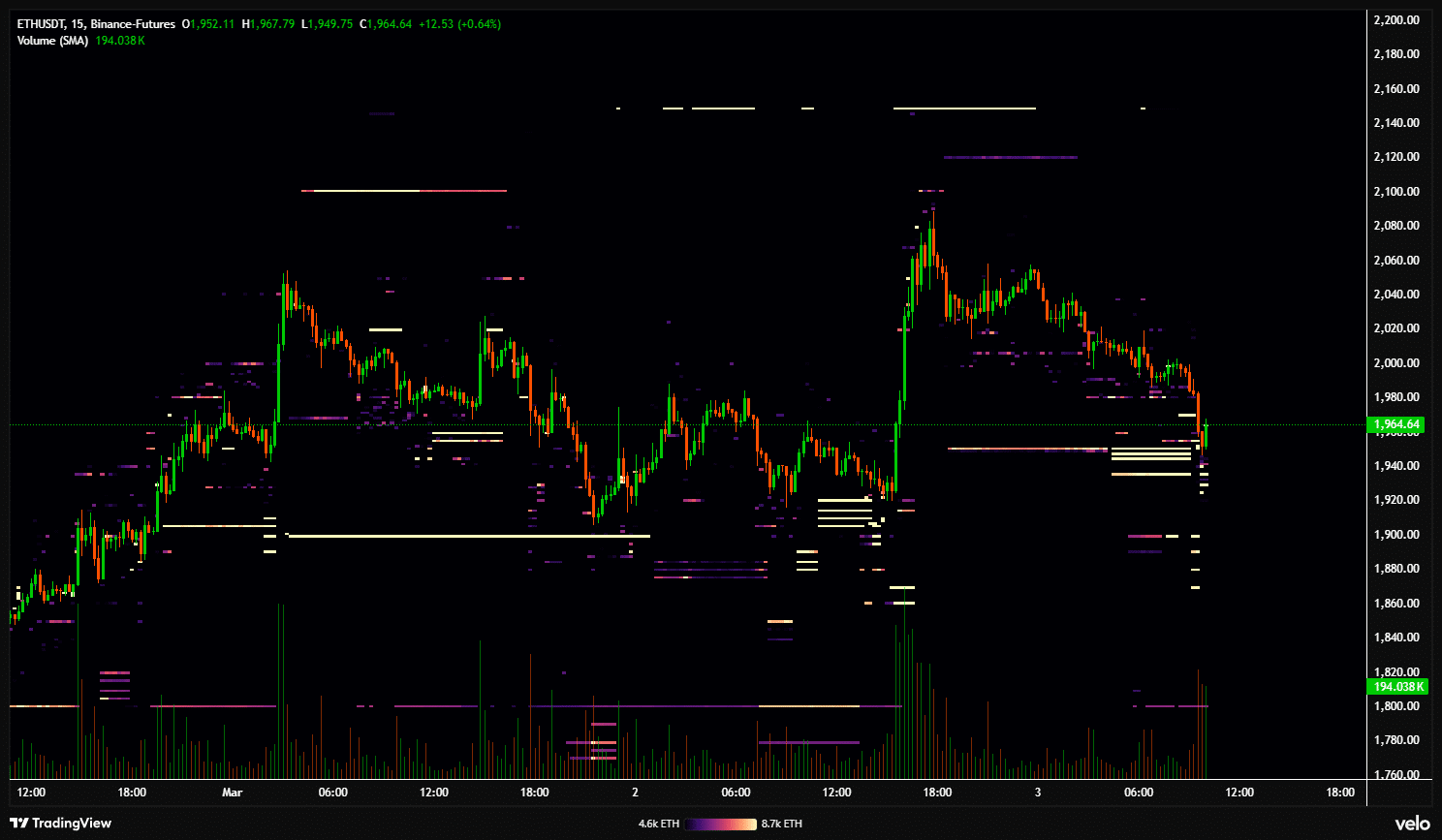

Ethereum – Accumulation spree meets whale-led sell pressure and that means…

Dana's March 25 Catalyst: Testing the $10B Math Against a $35 Price Target

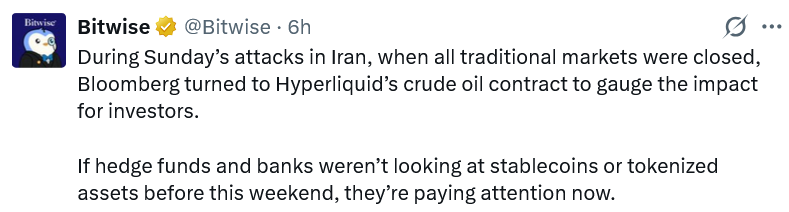

TradFi to adopt 24/7 crypto rails sooner than expected: Bitwise

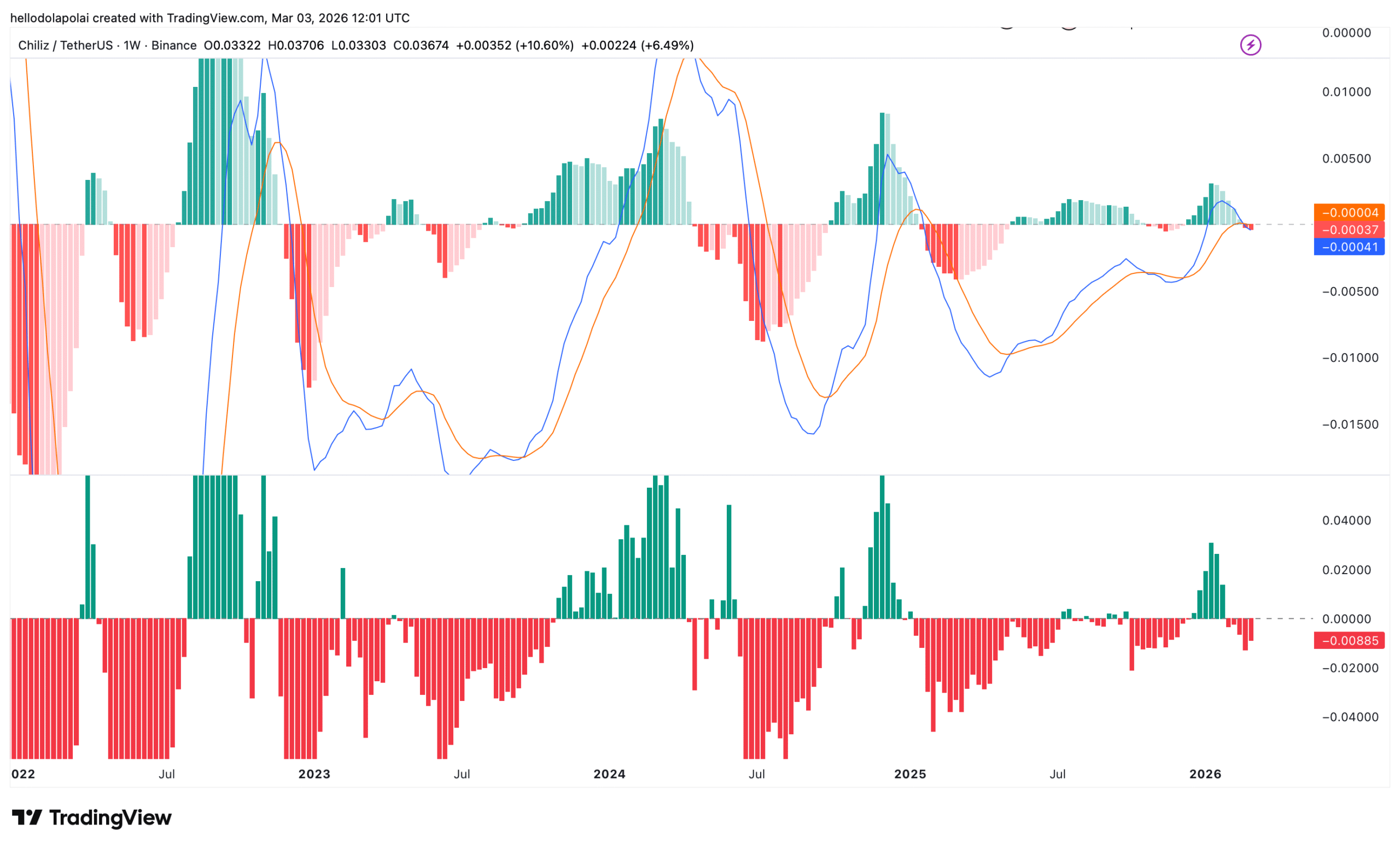

Chiliz nears key resistance: What’s behind CHZ’s fragile rally?