J&J Shares Rise 38% Over Half a Year: Is It Time to Buy, Sell, or Keep Holding?

Johnson & Johnson: Recent Stock Performance and Market Trends

Over the last six months, Johnson & Johnson (JNJ) has seen its share price climb by 38.4%. The stock has consistently traded above both its 50-day and 200-day simple moving averages since mid-June 2025, reflecting strong earnings prospects and solid business fundamentals. The "golden cross"—when the 50-day average moves above the 200-day average—occurred in July, signaling a bullish trend that has persisted, indicating ongoing upward momentum for J&J shares.

Image Source: Zacks Investment Research

Key Drivers Behind J&J’s Growth

J&J’s impressive stock performance is fueled by multiple factors, including robust sales and earnings growth, strong results from its Innovative Medicine and MedTech divisions, an optimistic outlook for 2026, rapid advancement in its product pipeline, favorable regulatory developments, and ongoing mergers and acquisitions. Despite these positives, the company faces challenges such as patent expirations, most notably for Stelara.

This analysis will explore J&J’s strengths and vulnerabilities to help investors make informed decisions following the recent surge in share price.

Innovative Medicine Segment: Consistent Expansion

The Innovative Medicine division continues to deliver steady growth. In 2025, sales increased by 4.1% organically, even as Stelara lost market exclusivity and the Part D redesign impacted results. Key products like Darzalex, Erleada, and Tremfya were primary growth drivers, while newer treatments such as Carvykti, Tecvayli, Talvey, Rybrevant, and Spravato also made significant contributions.

This segment achieved over $15 billion in sales for three consecutive quarters and surpassed $60 billion in annual revenue for the first time in 2025, with 13 brands posting double-digit growth.

Looking ahead to 2026, J&J anticipates accelerated growth in Innovative Medicine, driven by both established and new products. The company expects new launches to have a greater impact in 2026 and projects annual growth of 5% to 7% for this segment through 2030.

Pipeline Advancements and Strategic Investments

In 2025, J&J invested more than $32 billion in research, development, and acquisitions, including the purchases of Intra-Cellular Therapies and Halda Therapeutics. The company achieved important clinical and regulatory milestones, positioning itself for continued growth in the coming years.

Notable approvals in 2025 included Inlexzoh/TAR-200, a novel drug delivery system for high-risk non-muscle invasive bladder cancer, and Imaavy (nipocalimab) for generalized myasthenia gravis. J&J sees significant potential in nipocalimab and has also submitted regulatory filings for Icotyde/icotrokinra, a once-daily oral treatment for moderate-to-severe plaque psoriasis.

Three new cancer therapies—Carvykti, Tecvayli, and Talvey—have begun contributing to revenue, generating a combined $3 billion in 2025. The acquisition of Intra-Cellular Therapies added Caplyta, an antidepressant approved for several psychiatric conditions, to J&J’s portfolio.

J&J believes that 10 of its new or pipeline products in Innovative Medicine, including Talvey, Tecvayli, Imaavy, Caplyta, Inlexzo, Rybrevant, Lazcluze, and Icotyde, could each achieve peak sales of $5 billion or more.

MedTech Segment: Improving Performance

The MedTech division has shown notable improvement over the past three quarters, supported by acquisitions in cardiovascular devices (Abiomed and Shockwave), as well as growth in Surgical Vision and wound closure. The electrophysiology business also contributed to the 4.3% organic sales increase in 2025.

J&J is considering spinning off its Orthopaedics business as a standalone company, DePuy Synthes, which could enhance growth and profitability for MedTech, as orthopedics has lagged in recent years.

For 2026, the company expects MedTech to grow faster than in 2025, driven by broader adoption of new products in Cardiovascular, Surgery, and Vision. However, challenges remain in China, where government cost-control measures (volume-based procurement) continue to pressure sales—a trend expected to persist into 2026.

Patent Expirations and Other Challenges

Stelara, a major revenue generator, lost U.S. patent protection in 2025, accounting for about 18% of Innovative Medicine sales in 2024. Multiple biosimilars entered the market in 2025, including those from Amgen, Teva, Samsung Bioepis/Sandoz, and others, significantly impacting J&J’s sales. The loss of exclusivity for Stelara reduced Innovative Medicine segment growth by 1040 basis points in 2025, with a greater effect expected in 2026. Patent expirations for Simponi and Opsumit are also anticipated to affect results starting in 2026.

Additionally, the Medicare Part D redesign under the Inflation Reduction Act has negatively affected sales of Stelara, Erleada, and pulmonary hypertension drugs.

J&J is also dealing with over 73,000 lawsuits related to its talc-based products, which plaintiffs allege caused cancer due to asbestos contamination. The company maintains that its products are safe and has discontinued its talc-based baby powder. In April 2025, a Texas bankruptcy court rejected J&J’s proposed settlement plan, forcing the company to address these lawsuits individually after multiple failed bankruptcy strategies.

Stock Performance, Valuation, and Analyst Estimates

J&J shares have outperformed the broader industry, rising 47.2% over the past year compared to a 10% gain for the large-cap pharmaceuticals sector. The stock has also exceeded the performance of its sector and the S&P 500 Index.

Image Source: Zacks Investment Research

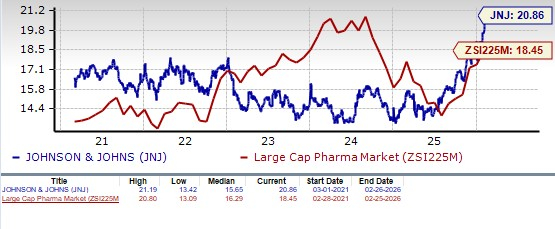

From a valuation perspective, J&J trades at a forward price-to-earnings ratio of 20.86, above the industry average of 18.45 and higher than its five-year average of 15.65, making it relatively expensive.

Image Source: Zacks Investment Research

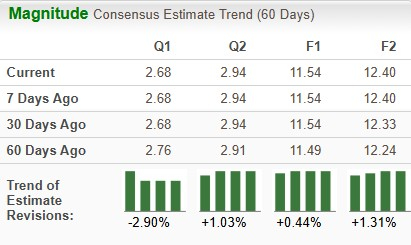

Analyst estimates have been trending upward, with the Zacks Consensus Estimate for 2026 earnings rising from $11.49 to $11.54 in the past two months, and the 2027 estimate increasing from $12.24 to $12.40 per share.

Image Source: Zacks Investment Research

Should Investors Stay with J&J?

J&J’s greatest advantage lies in its diversified operations, spanning pharmaceuticals and medical devices, with over 275 subsidiaries and 28 products generating more than $1 billion in annual sales. This diversification provides resilience against economic fluctuations. The company also maintains strong cash flow and has increased its dividend for 63 consecutive years.

After surpassing expectations in 2025, J&J is optimistic about sustaining its growth in 2026, targeting approximately $100 billion in annual revenue and expecting higher growth rates in both major segments.

While the company faces ongoing legal challenges, patent cliffs for key drugs, and headwinds in the Chinese MedTech market, management remains confident in its ability to overcome these obstacles.

Given the stock’s appreciation, rising earnings estimates, steady growth, new product launches, and pipeline progress, holding J&J shares appears prudent at this time.

Additional Investment Insights

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The pushback against prediction markets is now underway

China’s yuan poised to break its longest streak of weekly gains since 2012 amid Middle East unrest

**McKinsey: AI, Partnerships, and Commodity Divergence Create Alpha in Metals vs. Energy**

Zacks Investment Ideas feature highlights: Texas Pacific Land, DT Midstream and CMS Energy