3 Reasons Why ST Carries Risks and One Alternative Stock Worth Considering

Sensata Technologies: Recent Performance and Investment Outlook

Over the past half-year, Sensata Technologies has mirrored the S&P 500’s upward trend, advancing 11.6% to reach $37.41 per share, outpacing the index’s 7.2% gain.

Should investors consider adding Sensata Technologies to their portfolios, or does the stock carry more risk than reward?

Why We’re Cautious About Sensata Technologies

Our outlook on Sensata Technologies is reserved. Below, we outline three key reasons for our skepticism, along with a stock we believe offers better potential.

1. Lackluster Long-Term Revenue Expansion

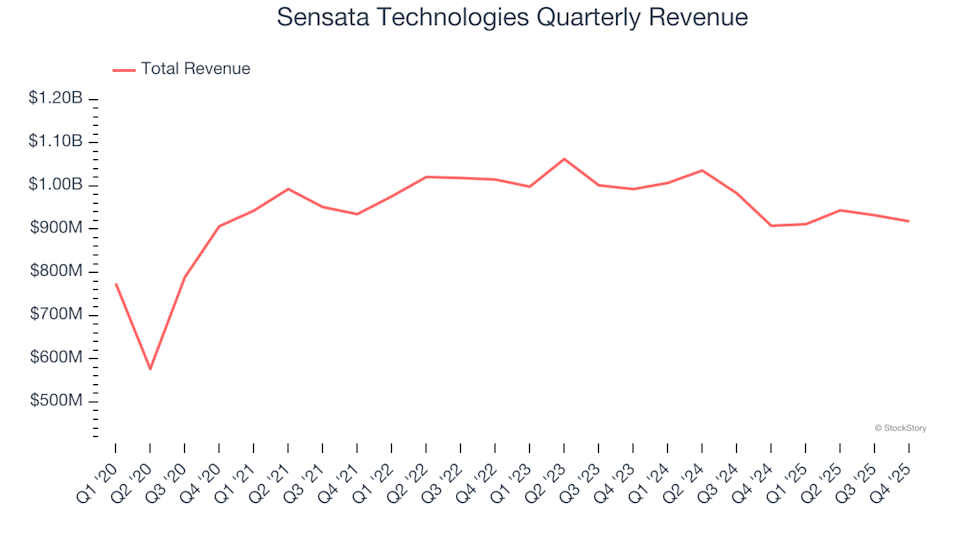

Consistent growth over time is a hallmark of high-quality companies. While short-term gains are possible for any business, sustained progress is what sets industry leaders apart. Over the last five years, Sensata Technologies has posted a modest 4% compound annual revenue growth rate, which falls short of what we expect from semiconductor firms. Given the cyclical nature of semiconductors, investors should anticipate alternating periods of rapid expansion and contraction.

2. Modest Growth Projections Ahead

Analyst forecasts provide insight into a company’s future prospects. While these predictions aren’t always precise, accelerating revenue growth tends to lift valuations and share prices, whereas deceleration can have the opposite effect.

Looking forward, Wall Street expects Sensata Technologies’ revenue to increase by just 2.9% over the next year. Although this suggests some improvement driven by new offerings, the growth rate remains below the industry average.

3. Weak Gross Margins Indicate Structural Challenges

Gross margin is a crucial measure for semiconductor companies, reflecting their pricing power, product complexity, and efficiency in sourcing materials and labor.

Sensata Technologies’ gross margin ranks among the lowest in its sector, highlighting its limited pricing leverage and the competitive environment it faces. Over the past two years, the company’s average gross margin was 29.2%, meaning it spent approximately $70.76 on costs for every $100 in revenue generated.

Our Verdict

While we appreciate companies tackling complex technological challenges, Sensata Technologies doesn’t currently meet our investment criteria. The stock is trading at a forward price-to-earnings ratio of 10.4 (or $37.41 per share), suggesting that much optimism is already reflected in its valuation. We believe there are stronger opportunities elsewhere. For example, consider an industry-leading aerospace company with a proven M&A track record.

Stocks We Prefer Over Sensata Technologies

Building a successful portfolio means focusing on future growth, not past performance. The risks associated with crowded trades are increasing daily.

Our Top 6 Stocks for this week features a handpicked selection of high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

This list includes well-known names like Nvidia, which soared 1,326% between June 2020 and June 2025, as well as lesser-known success stories such as Comfort Systems, which achieved a 782% five-year return. Discover your next standout investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Malaysia anti-graft agency probing government deal with chip firm Arm Holdings

BoJ’s Ueda says will closely watch impact of Middle East developments on domestic, overseas economy

Australia Approves AUDD Stablecoin for XRPL, XRP Price Steady

Streamex Names Shawn Matthews to Board Amid Institutional Expansion Push