3 Motives to Offload PAYC and One Alternative Stock Worth Buying

Paycom’s Recent Performance: A Closer Look

Over the past half year, Paycom shareholders have faced a challenging period, with the stock declining by 43.8% to its current price of $128.00. This significant drop was influenced by weaker-than-expected quarterly results, leaving many investors uncertain about the best course of action moving forward.

Is Paycom a potential opportunity at these levels, or does it pose additional risk to your investments?

Why We’re Cautious About Paycom

Although the current valuation may seem attractive, we’re choosing to remain on the sidelines. Here are three reasons to approach PAYC with caution, along with a stock we prefer instead.

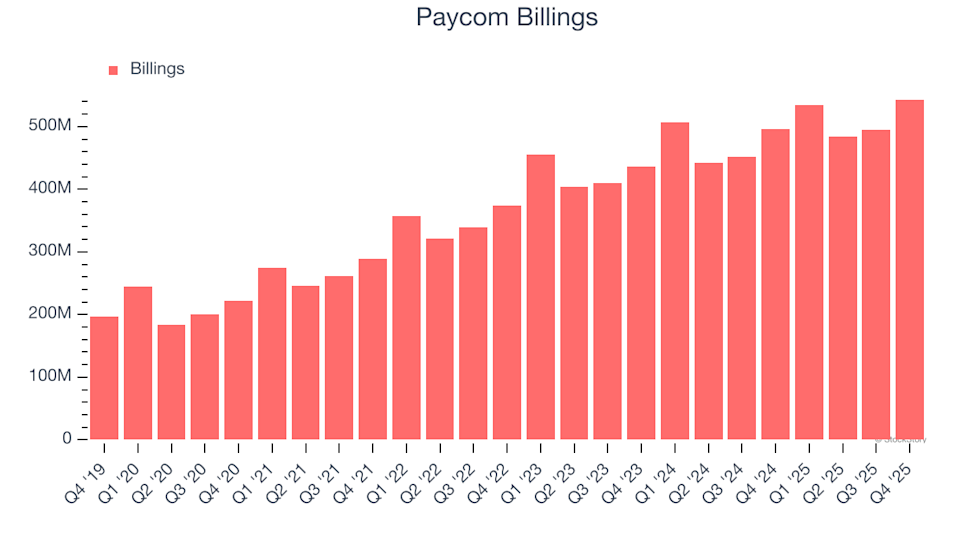

1. Billings Growth Signals Tepid Demand

Billings, often referred to as “cash revenue,” reflect the total payments collected from customers within a specific timeframe, differing from recognized revenue, which is spread out over contract periods.

In the fourth quarter, Paycom reported $543.4 million in billings. Over the past year, billings grew by an average of just 8.5% year-over-year—a lackluster result that points to mounting competition and difficulties in attracting and keeping clients.

2. Revenue Growth Forecasts Are Underwhelming

Analyst projections for future revenue offer insight into a company’s outlook. While forecasts are not always precise, faster growth tends to drive higher valuations and stock prices, whereas slowing growth can have the opposite effect.

Wall Street expects Paycom’s revenue to increase by just 6.6% over the next year, a notable slowdown compared to its 19.5% annualized growth over the past five years. This muted outlook suggests that demand for Paycom’s offerings may be softening.

3. Declining Operating Margins

While many software firms adjust their earnings for stock-based compensation (SBC), we focus on GAAP operating margin, as SBC represents a real cost for attracting and retaining talent. Operating margin is a key indicator of profitability, revealing how much profit remains after all core expenses.

Paycom’s operating margin has fallen by 6 percentage points over the last two years. This trend raises concerns about the company’s cost structure, especially since stronger revenue growth should have led to improved efficiency and profitability. For the trailing twelve months, Paycom’s operating margin stood at 27.6%.

Our Verdict

While Paycom is not a poor business, it doesn’t make our list of top picks. Following its recent decline, the stock trades at 3.1 times forward price-to-sales, or $128.00 per share. Although this valuation appears fair, the company’s weakening fundamentals introduce considerable downside risk. We believe there are more attractive opportunities in the market. One alternative to consider is the leading endpoint security platform.

Alternative Stocks to Consider

Relying on just a handful of stocks can leave your portfolio vulnerable. Now is the time to secure high-quality investments before the market shifts and these opportunities fade.

Don’t wait for the next bout of market turbulence. Explore our Top 9 Market-Beating Stocks, a handpicked selection of high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

This list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Comfort Systems, which achieved a 782% five-year return. Discover your next winning investment with StockStory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Director/PDMR Shareholding

Oracle Launches AI Tool To Predict Construction Safety Risks

Platts Adjustments to Middle Eastern Oil Pricing Stir Concerns Among Traders

These projects raised $1.2B and wasted it: how chains failed to deliver ROIs