3 Motives to Offload NATR and One Alternative Stock Worth Buying

Nature's Sunshine: Recent Performance and Investor Considerations

Nature's Sunshine has experienced a remarkable surge in its stock price over the last half-year, climbing 63.7% and reaching a new annual peak of $27.62 per share. This impressive growth has been fueled in part by strong quarterly earnings, prompting investors to consider their next move.

Is now the right time to invest in Nature's Sunshine, or could it pose a potential risk to your investment portfolio?

Why We Remain Cautious on Nature's Sunshine

While shareholders have benefited from the recent price rally, we are choosing to stay on the sidelines for now. Below are three key reasons to approach NATR with caution, along with an alternative stock we prefer.

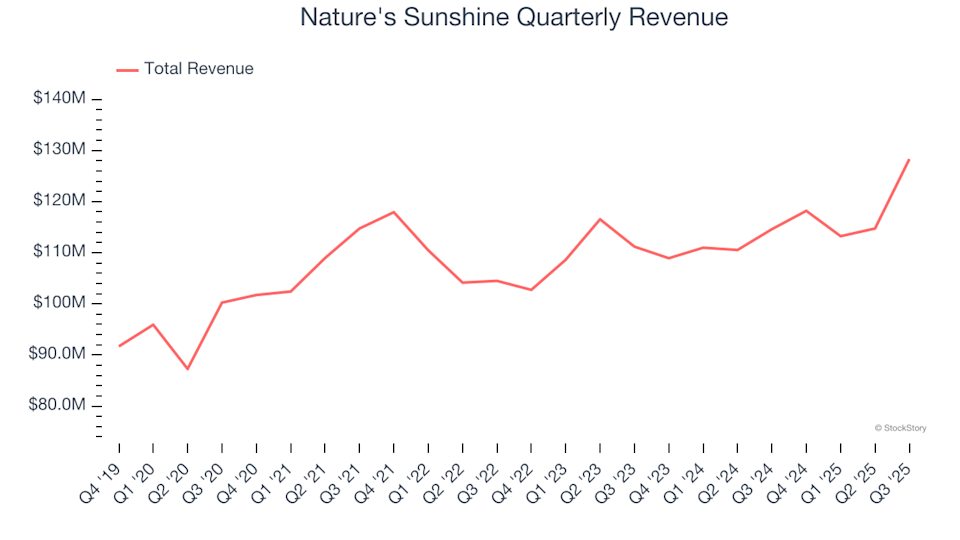

1. Lackluster Long-Term Revenue Expansion

Consistent sales growth is a hallmark of a high-quality business. While any company can post strong results for a quarter or two, sustained growth over several years is more telling. Over the past three years, Nature's Sunshine has only managed a modest 2.8% compound annual growth rate in revenue, which falls short of our expectations.

2. Limited Distribution Channels Restrict Potential

Generating $474.5 million in revenue over the last year, Nature's Sunshine is considered a smaller player in the consumer staples sector. This size disadvantage can limit its ability to negotiate with retailers and benefit from economies of scale, putting it at a disadvantage compared to larger competitors.

3. Tepid Revenue Growth Forecasts

Analyst projections provide insight into a company's future prospects. Although forecasts are not always precise, accelerating growth tends to drive higher valuations, while slowing growth can have the opposite effect.

Wall Street expects Nature's Sunshine's revenue to increase by just 3.1% over the next year—a figure that suggests its latest products are unlikely to drive significant top-line improvement in the near term.

Our Verdict

While Nature's Sunshine is not a poor business, it does not meet our investment criteria. Following its recent surge, the stock is trading at a forward price-to-earnings ratio of 29.8 (or $27.62 per share), indicating that much optimism is already reflected in the price. There are more attractive opportunities available. For example, we recommend considering the leading endpoint security platform in the industry.

Alternative Stocks to Consider

This year, the market has seen substantial gains, but it's important to note that just four companies are responsible for half of the S&P 500’s total increase. Such concentration can be concerning for investors. While many are flocking to popular stocks, savvy investors are seeking out high-quality businesses that are overlooked and undervalued. Explore our carefully selected Top 5 Growth Stocks for this month, a collection of High Quality companies that have delivered a 244% return over the past five years (as of June 30, 2025).

Our list features both well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, and lesser-known success stories such as Comfort Systems, which achieved a 782% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Russia Flags Crypto as Key Tool in Illegal Financial Schemes

Hedge funds push back against Labour’s ‘bold’ proposal to prohibit non-compete agreements

Geopolitical shifts are transforming the global economy as they happen – Rabobank

Vodafone teams up with Amazon's satellites to connect masts in Europe and Africa