Central Garden & Pet (CENT): Should You Buy, Sell, or Hold After Q4 Results?

Central Garden & Pet: Recent Performance Overview

Central Garden & Pet is currently priced at $39.25 per share, closely mirroring the broader market with an 8.5% gain over the past six months. In comparison, the S&P 500 has increased by 7.2% during the same period.

Is Central Garden & Pet a smart addition to your portfolio, or does it carry unnecessary risk?

Why We Believe Central Garden & Pet May Lag Behind

Our outlook on Central Garden & Pet is cautious. Below, we outline three reasons we’re steering clear of CENT, along with a stock we prefer instead.

1. Core Business Faces Headwinds as Organic Sales Drop

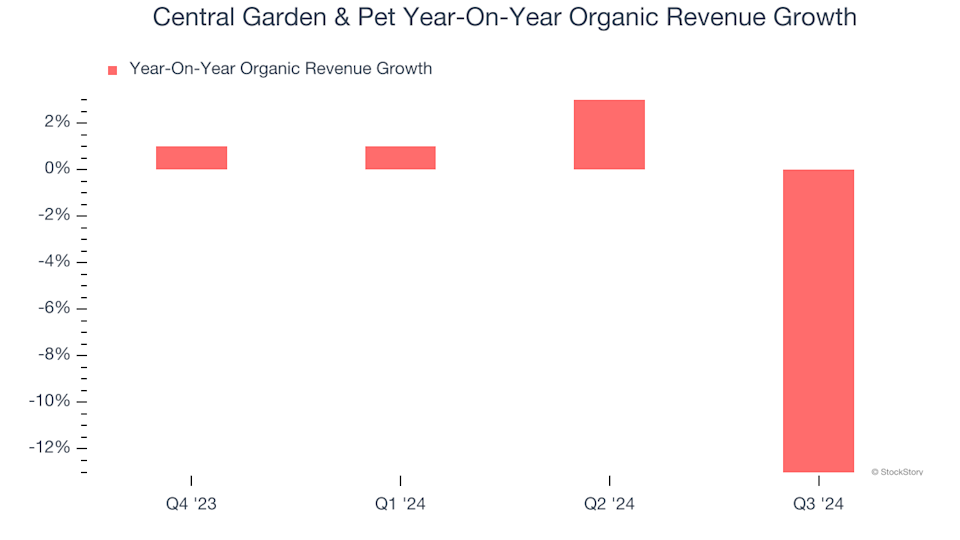

Organic revenue growth is a key indicator of a company’s true performance, as it excludes the effects of acquisitions, divestitures, and currency swings. Over the past eight quarters, Central Garden & Pet has seen declining demand, with average organic sales shrinking by 3% year over year.

Central Garden & Pet Year-On-Year Organic Revenue Growth

2. Modest Revenue Growth Forecasted

Wall Street’s revenue forecasts offer a glimpse into a company’s future prospects. While these estimates aren’t always precise, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect. Analysts expect Central Garden & Pet’s revenue to grow by just 1.1% over the next year. Although this suggests some improvement from new products, it still trails the industry average.

3. Past Growth Efforts Have Underwhelmed

Evaluating a company’s growth also means considering how efficiently it uses capital. Return on Invested Capital (ROIC) measures how much operating profit is generated for every dollar of capital employed. Central Garden & Pet’s five-year average ROIC stands at 8.3%, which is lackluster compared to leading consumer staples companies that regularly achieve 20% or more.

Central Garden & Pet Trailing 12-Month Return On Invested Capital

Our Verdict

Central Garden & Pet does not meet our standards for quality investments. While its current valuation of 14.1× forward P/E (or $39.25 per share) appears fair, the company’s weak fundamentals introduce significant downside risk. We believe there are more attractive opportunities available. For example, consider a resilient business like the owner of Taco Bell.

Stocks We Prefer Over Central Garden & Pet

Relying on just a handful of stocks can leave your portfolio vulnerable. Now is the time to secure high-quality investments before the market broadens and current prices are no longer available.

Discover Top Stock Picks

Don’t wait for the next market downturn. Explore our Top 6 Stocks for this week—a handpicked selection of high-quality companies that have outperformed the market with a 244% return over the past five years (as of June 30, 2025).

Our list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Exlservice, which delivered a 354% five-year return. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Walmart (WMT) Coverage Reinstated With Bullish Outlook from BofA

Chubb (CB) Price Target Raised Following Property and Casualty Sector Results

Chubb (CB) Price Target Raised Following Property and Casualty Sector Results

BofA Cuts Domino's (DPZ) Target to $545 While Keeping Bullish Rating