3 Compelling Motives to Sell PAG and One Alternative Stock Worth Buying

Penske Automotive Group: Recent Performance and Investor Concerns

In the past half-year, shares of Penske Automotive Group have dropped to $157.70, reflecting a 16.3% decline. This underperformance stands in sharp contrast to the S&P 500, which has risen by 7.2% during the same period. The downturn is partly attributed to weaker-than-expected quarterly results, prompting investors to reconsider their positions.

Is Penske Automotive Group a bargain at current levels, or does it pose a risk to your investments?

Why We Expect Penske Automotive Group to Lag Behind

Although the stock now trades at a lower price, our outlook on Penske Automotive Group remains cautious. Below, we outline three key reasons why we believe there are more attractive opportunities than PAG, along with a stock we prefer.

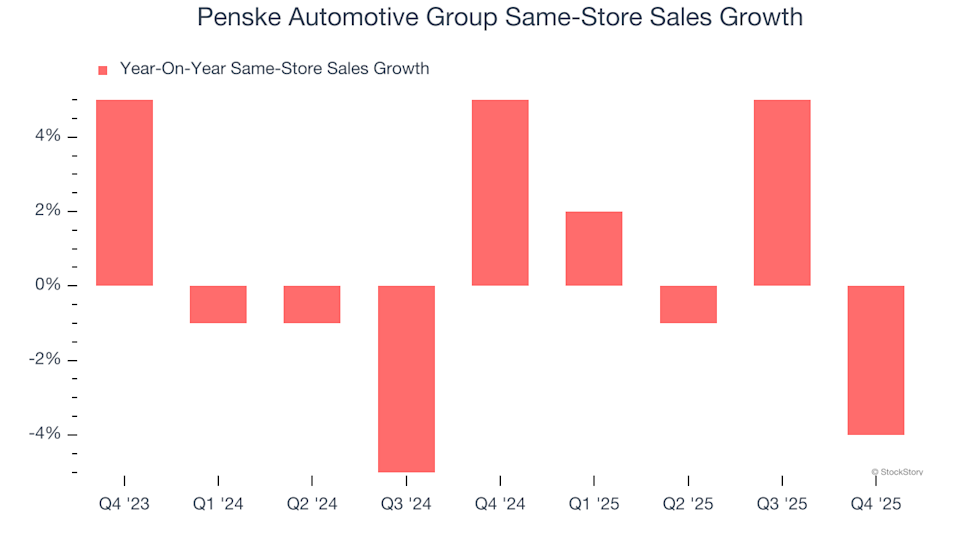

1. Stagnant Same-Store Sales Reflect Weak Customer Demand

Same-store sales are a crucial metric for retailers, measuring revenue growth at existing locations. This figure is influenced by both customer traffic and average transaction size.

For Penske Automotive Group, same-store sales have shown little to no growth over the past two years, indicating that demand at its current outlets has remained flat.

2. Slim Gross Margins Signal Structural Profitability Challenges

We favor companies with robust gross margins, as these typically point to pricing power or unique offerings, which can drive higher operating profits.

Penske Automotive Group, however, operates with thin margins—averaging just 16.5% over the past two years. This suggests the company faces intense competition and limited pricing flexibility, as its products are widely available. In practical terms, Penske pays suppliers $83.54 for every $100 in revenue, leaving little room for profit.

3. Declining Earnings Per Share (EPS)

Long-term trends in earnings per share reveal whether a company's additional sales are translating into profits. Sometimes, revenue growth is achieved through heavy spending on marketing, which can erode profitability.

Unfortunately, Penske Automotive Group's EPS has fallen by an average of 10.5% per year over the last three years, even as revenue increased by 3.4%. This pattern indicates that the company has become less profitable on a per-share basis as it has grown.

Our Verdict

Penske Automotive Group does not meet our standards for quality investments. Despite its current valuation of 11.8× forward P/E (or $157.70 per share), we remain unconvinced about the company's prospects. There are more compelling options available. For example, consider instead.

Better Alternatives to Penske Automotive Group

Relying on just a handful of stocks can make your portfolio vulnerable. Now is the time to secure high-quality investments before market conditions change and attractive prices disappear.

Discover Our Top Growth Stock Picks

Don't wait for the next market downturn. Review our Top 5 Growth Stocks for this month. This handpicked selection features high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list includes well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Exlservice, which achieved a 354% five-year return. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

ETH Price Replays Classic Master Pattern as Ethereum Moves to Solve Its Biggest Problem

Leading US Financial Firms Advise Allocating Bitcoin in Portfolios

“Could You Handle the Pressure” as XRP May Drop to This Multi-Year Support Before Run to $27