3 Reasons to Consider Selling RUSHA and One Alternative Stock Worth Buying

Rush Enterprises: A Closer Look at Recent Performance

Since February 2021, the S&P 500 has returned 77.9%. In comparison, Rush Enterprises has outperformed significantly, climbing 149% over the past five years to reach $71.67 per share. The company’s upward trend has continued, with a 22.2% gain in the last six months, fueled by strong quarterly earnings that surpassed the S&P by 15%.

Should investors consider adding Rush Enterprises to their portfolios, or does it carry more risk than reward?

Why We’re Cautious About Rush Enterprises

While shareholders have benefited from the stock’s impressive rise, we remain skeptical about Rush Enterprises’ future prospects. Below are three reasons we’re steering clear of RUSHA, along with a suggestion for a more attractive alternative.

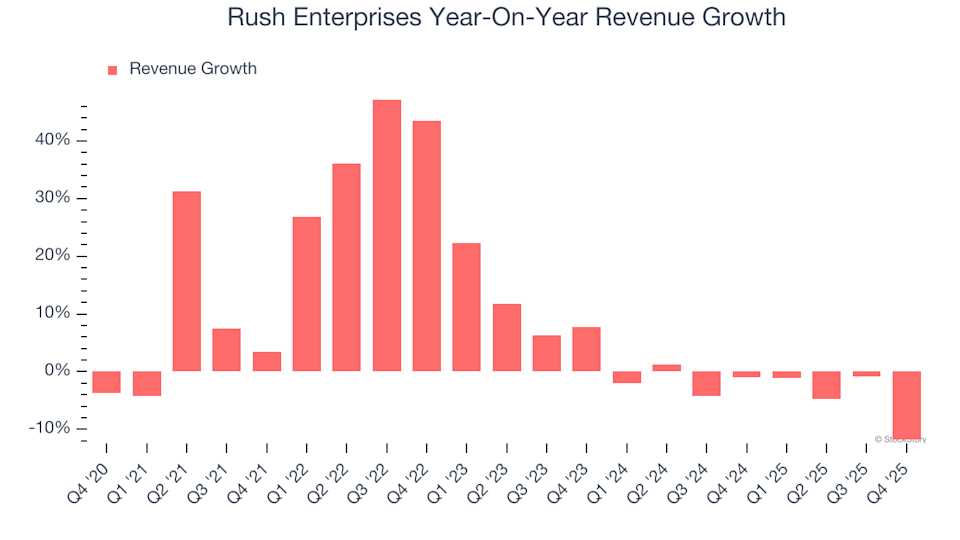

1. Declining Revenue Growth

Although long-term expansion is crucial, focusing solely on historical performance can overlook recent shifts in industry dynamics. Rush Enterprises has experienced a notable reversal in its growth trajectory, with revenue shrinking at an annual rate of 3.1% over the past two years.

Rush Enterprises Year-On-Year Revenue Growth

2. Weak Profit Margins Indicate Structural Challenges

For companies in the industrial sector, costs such as labor, materials, and supplies play a major role in profitability. These expenses can fluctuate due to inflation, supply chain issues, and the company’s scale. Rush Enterprises has struggled with low gross margins, averaging just 20.3% over the last five years. In practical terms, this means the company spent $79.66 for every $100 earned in revenue, highlighting tough competition and limited pricing power.

Rush Enterprises Trailing 12-Month Gross Margin

3. Earnings Per Share Have Fallen Sharply

While it’s important to monitor long-term earnings, short-term changes in EPS can reveal emerging challenges. Over the past two years, Rush Enterprises’ EPS dropped by 11.1%—a steeper decline than its revenue—suggesting the company has struggled to adapt to weaker demand.

Rush Enterprises Trailing 12-Month EPS (Non-GAAP)

Our Verdict

We appreciate companies that make life easier for their customers, but when it comes to Rush Enterprises, we prefer to watch from the sidelines. Despite its recent outperformance and a forward P/E ratio of 19.5 (or $71.67 per share), the company’s underlying weaknesses make it a risky bet. There are stronger investment opportunities available. For example, consider one of our top digital advertising recommendations.

Better Alternatives to Rush Enterprises

Relying on just a handful of stocks can leave your portfolio vulnerable. Now is the time to secure high-quality investments before the market shifts and these opportunities fade.

Don’t wait for the next market downturn. Explore our Top 6 Stocks for this week—a handpicked selection of high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

Our list features well-known names like Nvidia, which soared 1,326% between June 2020 and June 2025, as well as lesser-known success stories such as Kadant, which achieved a 351% five-year return. Discover your next winning investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

How Does Ecolab's Stock Performance Stack Up Against Other Companies in the Basic Materials Sector?

Northrop Grumman Shares: Is NOC Surpassing the Performance of the Industrial Sector?

Spot Bitcoin ETFs Record $787 Million Inflows, End 5-Weeks Of Consecutive Outlows

Analyst Says 99% of XRP Investors Will Lose Everything. Here’s why