FUTU vs. NU: Which Fintech Stock is a Better Buy Right Now?

Both Nu Holdings NU and Futu Holdings Limited FUTU are prominent fintech players stirring up the market. NU, with its banking, credit cards and other financial services, serves the Latin American market. FUTU is a digital brokerage platform operating in Hong Kong, China and other international markets.

Let us analyze these two companies and find out which can provide more upside to investors right now.

The Case for NU

NU continues to demonstrate why it remains one of the most compelling digital banking platforms globally. The company’s performance in Brazil stands out as a major strength, with a large customer base and extensive coverage of the adult population. Maintaining a high activity rate at this scale is no small achievement; it highlights deep customer engagement rather than superficial user growth. This combination of scale and engagement creates a powerful moat, allowing NU to expand product adoption continuously. The ability to grow while improving efficiency, as reflected in its declining efficiency ratio, reinforces the strength of its core business model.

Beyond Brazil, NU’s accelerating traction in Mexico and Colombia adds an important second growth engine. Both markets have already attracted millions of customers, showing that NU’s digital-first banking model travels well across geographies. These markets are still in relatively early stages, offering a long runway for customer acquisition and product cross-selling. The consistency in engagement metrics across regions suggests that NU is not simply exporting a product but is successfully replicating a scalable platform. This geographic diversification reduces overreliance on a single market and strengthens the company’s long-term growth profile.

Financially, NU’s rising revenues and expanding credit portfolio underline the quality of its growth. Rising ARPAC indicates that customers are not only joining the platform but also using it more actively across products. The credit portfolio’s expansion across cards, secured, and unsecured lending shows increasing maturity and diversification, which supports sustainable earnings growth. Importantly, this expansion has been accompanied by healthy asset quality metrics and disciplined risk management. Strong profitability, reflected in rising net income and a record return on equity, demonstrates NU’s ability to balance growth with financial discipline. Looking ahead, management’s vision of becoming an AI-first bank further strengthens the investment case, positioning NU to enhance efficiency, personalize customer experiences, and reinforce its competitive edge in digital banking.

The Case for FUTU

FUTU has emerged as one of the most compelling growth-oriented digital brokerage platforms, supported by strong monetization, expanding global reach and a favorable valuation relative to peers. Several key factors underline the company’s attractiveness and long-term potential.

One of FUTU’s most important strengths is its superior monetization efficiency. The company generates significantly higher revenue per funded account compared to many global brokerage platforms. This reflects the presence of highly engaged, affluent users who actively participate in trading across equities, derivatives and other financial instruments. This monetization advantage enables FUTU to maintain strong profitability while continuing to invest in innovation and expansion.

Another major growth driver is FUTU’s dominant position in Hong Kong’s brokerage ecosystem. The company has built a strong reputation among retail investors, particularly in IPO subscriptions, where its platform is widely used. This leadership position allows FUTU to benefit directly from improving capital market activity and increased investor participation. As IPO markets recover, FUTU stands to gain from higher trading volumes and new customer inflows.

International expansion also plays a crucial role in FUTU’s growth strategy. The company has been steadily expanding beyond its core markets into new regions, diversifying its customer base and reducing geographic concentration risk. This expansion supports sustained account growth and strengthens its global presence as digital brokerage adoption increases worldwide.

Additionally, FUTU’s exposure to emerging trading segments such as cryptocurrency enhances its long-term growth potential. Rising interest in digital assets has contributed to higher platform engagement and increased trading activity, positioning FUTU to benefit from evolving investor preferences.

Overall, FUTU’s strong monetization, market leadership, international expansion and exposure to emerging asset classes position it as a promising fintech platform with solid long-term growth prospects.

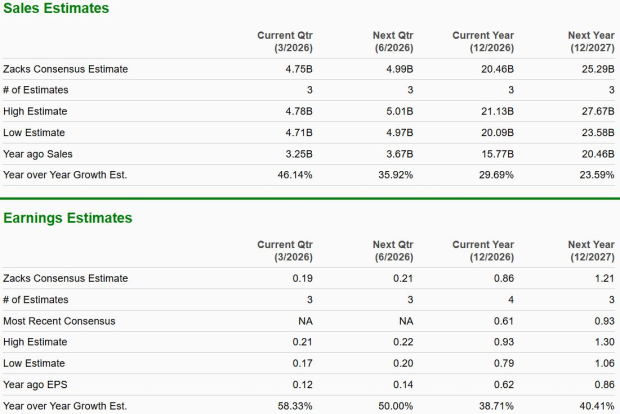

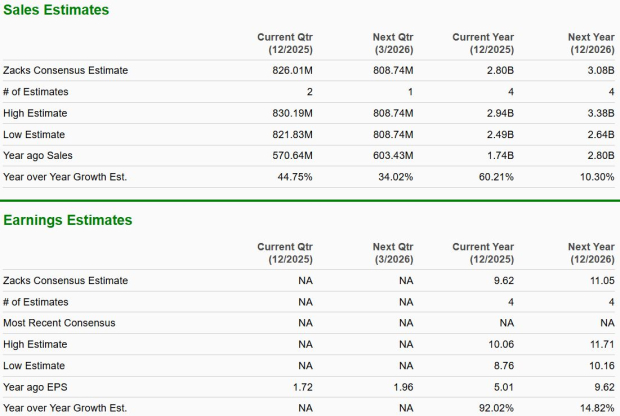

How Do Estimates Compare for FUTU & NU?

The Zacks Consensus Estimate for NU’s 2026 sales and EPS indicates year-over-year growth of 30% and 39%, respectively. Two estimates for 2026 have moved north in the past 60 days versus no southward revision.

The Zacks Consensus Estimate for FUTU’s 2026 sales and EPS hints at year-over-year growth of 10% and 15%, respectively. One estimate for 2026 has moved north in the past 60 days, versus no southward revision.

NU Trades Cheaper Than FUTU

Nu Holdings is trading at a forward price to earnings multiple of 16.41 times, lower than its 12-month median of 19.93 times. FUTU’s forward earnings multiple stands at 13.69 times, lower than its median of 16.5 times.

NU Emerges as the Stronger Choice

Both NU and FUTU present compelling fintech growth stories, supported by strong engagement, scalable platforms and expanding global opportunities. However, NU stands out as the better buy right now due to its broader financial ecosystem, deeper customer relationships and stronger long-term expansion potential across multiple high-growth markets. Its ability to drive consistent engagement while expanding lending and cross-selling opportunities strengthens its competitive moat and earnings visibility. Additionally, NU’s vision of becoming an AI-driven bank enhances its future efficiency and innovation potential. While FUTU remains a strong brokerage platform, NU’s diversified model, scalability, and structural growth drivers give it a clearer and more sustainable long-term advantage.

NU and FUTU carry a Zacks Rank #2 (Buy) each at present.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Femasys Announces Inducement Grants Under Nasdaq Listing Rule 5635(c)(4)

Oscar Health (OSCR) Reports $11.7B in 2025 Revenue Amid Strong Membership Growth

Root Inc. (ROOT) Delivers Record 2025 Results with 29% Revenue Growth and $40M Net Income

Why Flutter Entertainment (FLUT) Stock Is Plummeting Today