Is Serve Robotics Creating the Most Robust Autonomy Advantage by 2026?

Serve Robotics: From Pilot Projects to Scalable Autonomy

Serve Robotics (SERV) is making the leap from experimental robotics deployments to a robust, scalable autonomy platform, with 2026 positioned as a potential turning point for the company.

Building a Competitive Edge Through Scale

The company’s first major advantage is its growing scale. By the third quarter of 2025, Serve Robotics had surpassed 1,000 active robots and is projected to double that number, expanding its presence in cities such as Los Angeles, Miami, Dallas, Atlanta, and Chicago. Leadership views this milestone as the moment when pilot programs evolve into sustainable, repeatable business models, with each new robot enhancing operational efficiency and data collection. Strategic partnerships with industry leaders like Uber and DoorDash have given Serve Robotics access to a significant portion of the U.S. food delivery market, further strengthening its network effects.

Technological Advancements Fueling Growth

The second pillar of Serve Robotics’ strategy is continuous technological improvement. The latest Gen3 robots offer substantial cost savings—reducing unit costs by 65% compared to earlier models—while delivering faster speeds and longer operational ranges. Recent acquisitions, including Vayu and Phantom Auto, are designed to bolster the company’s AI capabilities and remote operation technology, accelerating a cycle where increased usage leads to smarter models and less need for human oversight.

Expanding into Healthcare with Diligent Robotics

In January 2026, Serve Robotics broadened its reach by acquiring Diligent Robotics. This move introduced Moxi hospital robots, which have already completed over 1.25 million deliveries across more than 25 hospitals. By integrating indoor delivery capabilities, Serve Robotics is able to increase revenue per robot and tap into new markets, creating a unified autonomy platform that spans both outdoor and indoor environments.

Financial Outlook and Long-Term Vision

While the company continues to operate at a loss due to significant investments in research, development, and expansion, it maintains over $200 million in available funds. Serve Robotics is targeting a tenfold increase in revenue for 2026, prioritizing long-term market leadership over short-term profitability.

If Serve Robotics can successfully leverage its scale and cross-industry data, it may establish one of the most formidable competitive barriers in urban robotics as 2026 approaches.

Competitive Landscape: Amazon and Aurora Innovation

When evaluating Serve Robotics’ position, two notable competitors stand out: Amazon and Aurora Innovation. Amazon has steadily expanded its robotics initiatives, including autonomous delivery pilots and advanced warehouse automation. With vast order volumes, proprietary logistics data, and significant financial resources, Amazon’s integrated supply chain—from warehouses to customer doorsteps—gives it a strong foundation for scaling autonomous solutions. Should Amazon intensify its efforts in sidewalk or small-package delivery automation, its data and distribution network could present a serious challenge.

Meanwhile, Aurora Innovation is focused on developing self-driving technology for commercial trucking, specializing in highway autonomy. The company leverages extensive simulation, real-world testing, and freight partnerships to refine its AI systems. Aurora’s approach demonstrates how scale, capital, and technical validation can reinforce a competitive edge in autonomy.

To maintain and grow its advantage, Serve Robotics must continue to build urban data density and integrate across multiple platforms, especially as it faces competition from Amazon’s logistics dominance and Aurora’s highway expertise.

SERV Stock: Performance, Valuation, and Analyst Estimates

Over the past three months, Serve Robotics shares have risen by 2%, outperforming the broader industry, which saw a 19.6% decline.

Three-Month Stock Performance of SERV

Image Source: Zacks Investment Research

Currently, SERV stock trades at a premium, with a forward 12-month price-to-sales (P/S) ratio of 25.11—significantly higher than the industry average of 12.85.

Comparison of SERV’s Forward P/S Ratio to Industry Average

Image Source: Zacks Investment Research

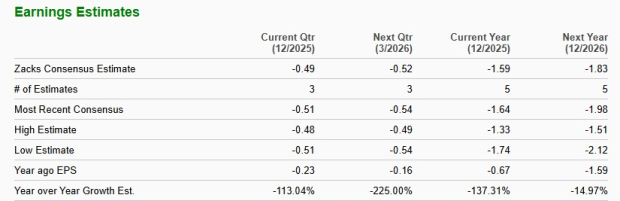

According to Zacks, the consensus estimate for Serve Robotics’ 2026 loss per share remains unchanged at $1.83 over the past two months. The company is expected to report a larger loss in 2026 compared to the previous year.

Trends in SERV’s Earnings Per Share (EPS)

Image Source: Zacks Investment Research

Serve Robotics currently holds a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CORRECTION -- WeShop Helps Pet Lovers Turn Everyday Pet Spending into Ownership

Bitwise Report Finds Long-Term Bitcoin Holders Consistently Reap Profits

Investor Education Webinar

Vitalik Buterin Targets Ethereum’s Core Bottlenecks with Bold Overhaul